TL;DR:

- Many Australian investors are often surprised to learn that positive paper results do not always translate into weekly cash profits.

- Understanding the difference between net rental income and holding costs is essential to accurately assess real cash flow and make informed investment decisions.

Many Australian property investors are genuinely surprised to discover that a property showing a “positive” result on paper doesn’t always mean more money landing in their bank account each week. The gap between net rental income and holding costs is what defines your real cash flow position, and understanding this distinction is the foundation of every sound investment decision. This guide walks you through how to calculate, improve, and verify your property’s true cash flow, using expert-backed strategies and practical tax insights that apply directly to the Australian market.

Table of Contents

- Key concepts: What cash flow means for property investors

- Calculating your property’s real cash flow

- How tax and expense classification affect cash flow

- Top strategies to boost your property cash flow

- Verifying and monitoring cash flow: Maintaining peak performance

- What most cash flow guides miss: Beyond the numbers

- Take your property portfolio further with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your real cash flow | Calculating cash flow accurately means accounting for all costs, not just mortgage and rent. |

| Tax rules matter | Proper expense classification and understanding negative gearing directly affect your after-tax wealth. |

| Focus on net, not gross | Net yield provides a clearer view of true returns than gross rental figures. |

| Monitor and adjust | Ongoing verification helps you stay on track and spot cash-flow issues before they become problems. |

| Strategic improvements pay off | Small shifts—like better tenants, lower costs, or smarter tax claims—can boost your returns over time. |

Key concepts: What cash flow means for property investors

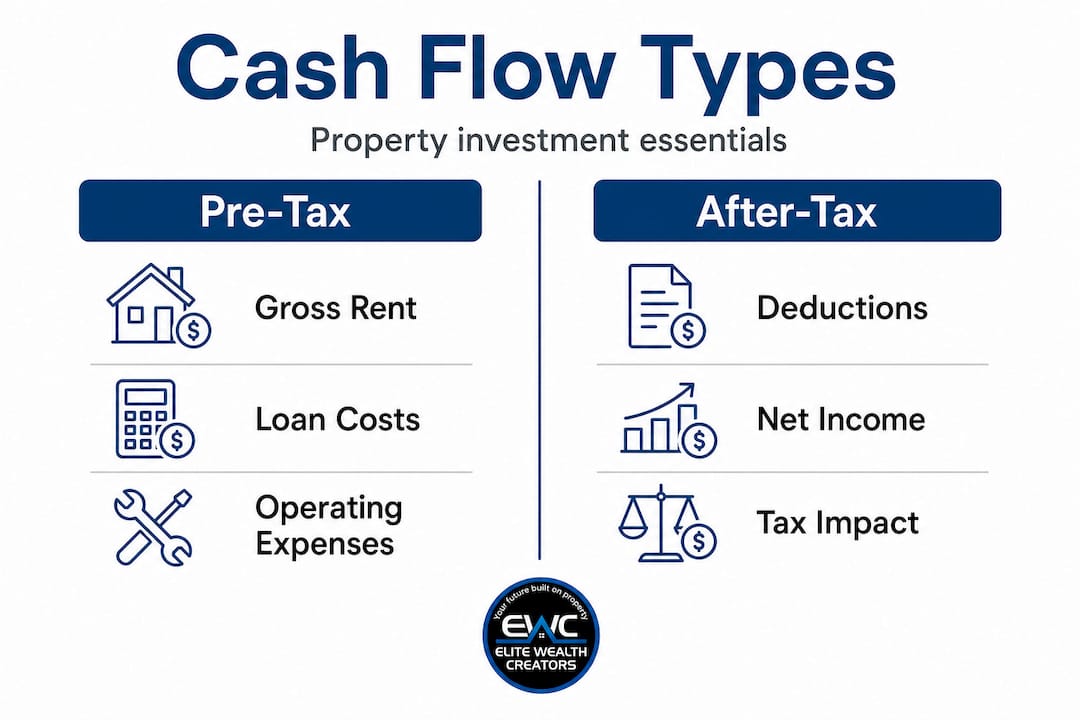

Cash flow in property investment is not simply rent minus mortgage repayments. It is the full picture: every dollar coming in from rent, minus every dollar going out in holding costs, financing, management fees, insurance, rates, and maintenance. When you look at it that way, the real number is often quite different from the figure investors first assume.

There are two layers you need to understand: pre-tax cash flow and after-tax cash flow. Pre-tax cash flow is the raw weekly or monthly surplus or shortfall before any tax adjustments. After-tax cash flow accounts for the tax refund or liability you receive at the end of the financial year, including the impact of deductions and depreciation.

Negative gearing sits at the centre of many Australian investors’ strategies. From the ATO’s perspective, negative gearing reduces taxable income when deductible expenses exceed rental income, which can produce a meaningful tax saving. However, that saving only arrives at tax time, not week to week.

Here is where investors often come unstuck. Depreciation deductions, such as Division 43 capital works and Division 40 decline-in-value allowances, are non-cash deductions. They reduce your taxable income on paper without requiring you to spend any money. As a result, your after-tax outcomes can differ significantly from your week-to-week cash movement, even though you still need to fund any genuine cash shortfall from your own pocket.

“The most important number is not what your accountant shows on a tax return. It is the amount you need to transfer from your savings account each month to keep the property running.”

Key cash flow components to track:

- Gross rental income (weekly rent multiplied by 52)

- Property management fees (typically 7 to 10 per cent of rent)

- Council rates and water charges

- Landlord insurance and building insurance

- Maintenance, repairs, and emergency costs

- Loan interest and principal repayments

- Body corporate fees (for units and apartments)

- Depreciation and capital works deductions (non-cash but tax-relevant)

| Cash flow type | What it includes | When it matters |

|---|---|---|

| Gross cash flow | Rent minus mortgage only | Quick initial estimate |

| Net pre-tax cash flow | Rent minus all cash costs | Day-to-day funding need |

| After-tax cash flow | Net pre-tax plus tax refund | Annual true return |

Now that you know why cash flow is key, let’s explore exactly what goes into its calculation.

Calculating your property’s real cash flow

With a clear idea of cash flow types, you can now accurately work out what your property is really earning you each year. The process is straightforward when you follow a structured approach, but it is easy to underestimate costs if you skip steps.

Step-by-step cash flow calculation:

- Start with gross rental income. Multiply your weekly rent by 52 to get your annual figure. If your property is vacant for two weeks per year, subtract that amount immediately.

- Subtract all operating expenses. Include management fees, insurance, rates, maintenance, body corporate fees, and any other recurring costs. Be thorough here. Annual fees that are paid in a lump sum are easy to overlook in monthly calculations.

- Subtract your loan interest. Use only the interest component of your repayment if you are on a principal-and-interest loan, or the full repayment if you want to see true cash outflow.

- Calculate pre-tax cash flow. This is your net position before tax. If it is negative, you will need to fund the shortfall from other income.

- Apply your marginal tax rate to the net rental loss. If you are negatively geared, multiply the loss by your marginal rate to estimate your annual tax saving.

- Add the tax refund to your pre-tax cash flow. The result is your estimated after-tax cash flow.

One of the most common mistakes investors make is relying on gross rental yield rather than net yield for planning purposes. Gross yield overstates actual earnings because it ignores operating expenses entirely. Net yield, calculated after all running costs, gives you a far more reliable basis for maximising rental cash flow and comparing properties accurately.

| Metric | Formula | Typical result |

|---|---|---|

| Gross rental yield | Annual rent / property value x 100 | 4 to 6 per cent |

| Net rental yield | (Annual rent minus expenses) / property value x 100 | 2 to 4 per cent |

| Pre-tax cash flow | Net rent minus loan costs | Often negative |

| After-tax cash flow | Pre-tax flow plus tax refund | Can be positive |

Pro Tip: When reviewing expert strategies for rental income, always model your cash flow using conservative vacancy assumptions of at least four weeks per year. This single adjustment prevents most cash flow surprises.

Good property management tips also play a direct role in your calculated yield. Lower vacancy rates and well-maintained properties consistently outperform the averages, which is why management quality belongs in your cash flow model from day one.

How tax and expense classification affect cash flow

Now that you can calculate cash flow, let’s see how tax rules and expense classifications influence real outcomes and your annual return. This is where many investors leave money on the table, or worse, create compliance problems by misclassifying costs.

The ATO draws a clear line between repairs and maintenance (immediately deductible) and capital improvements (claimed over time). Replacing a broken hot water system is a repair. Upgrading to a premium solar-powered system is an improvement. The distinction matters because misclassification can undermine your cash flow optimisation strategy and expose you to audit risk.

Immediately deductible expenses include:

- Routine repairs and maintenance

- Property management fees

- Council rates and water charges

- Insurance premiums

- Advertising for tenants

- Pest control and cleaning

Expenses claimed over time include:

- Capital improvements (claimed over the useful life of the asset)

- Borrowing costs, including loan establishment fees and mortgage insurance, spread over five years or the life of the loan, whichever is shorter

- Capital works (Division 43), claimed at 2.5 per cent per year over 40 years

Deduction eligibility depends on correct records and how costs are classified. Keeping detailed receipts, invoices, and a property expense log is not optional. It is the foundation of a defensible tax position and a genuine cash flow advantage.

Pro Tip: Commission a tax depreciation schedule from a qualified quantity surveyor as soon as you purchase an investment property. For properties built after 1985, this report can uncover thousands of dollars in annual non-cash deductions that directly improve your after-tax cash flow position. Explore maximising property deductions to understand how these schedules work in practice.

“Getting the classification right the first time costs far less than correcting it under ATO scrutiny.”

Understanding property investment classification tips from the outset also protects your ability to claim unlocking tax deductions in future years without amendment or penalty.

Top strategies to boost your property cash flow

Understanding the mechanics and pitfalls is only half the battle. Let’s move to proactive strategies you can use to boost your actual net cash position, starting with the most impactful actions first.

- Review your rent against the current market. Many investors set rent at the start of a tenancy and leave it unchanged for years. Conduct a market comparison every 12 months. Even a $30 per week increase on a single property adds $1,560 per year to your gross income.

- Reduce non-essential management costs. Compare property management fee structures annually. A difference of just two percentage points on a $500 per week rental saves $520 per year. Negotiate or switch providers if your current arrangement is not competitive.

- Improve tenant quality and retention. Vacancy is one of the most damaging cash flow events. A thorough tenant selection process and responsive maintenance reduce turnover. Retaining a good tenant for an extra 12 months can save thousands in re-letting fees and vacancy losses.

- Maximise eligible tax deductions. Ensure your depreciation schedule is current, all eligible expenses are claimed, and borrowing costs are being amortised correctly. Work with a property-specialist accountant rather than a generalist. The difference in outcomes is significant.

- Refinance strategically. Interest rates vary considerably between lenders. Refinancing to a lower rate on a $500,000 loan at a 0.5 per cent reduction saves $2,500 per year in interest, directly improving pre-tax cash flow.

- Invest in high-return improvements. Not all capital expenditure is equal. Adding air conditioning, off-street parking, or updated appliances in the right market can justify rent increases that outpace the cost of the improvement within two to three years.

Pro Tip: Before spending on any improvement, calculate the rent uplift required to recover the cost within 36 months. If the numbers don’t work in that timeframe, the improvement may not be the right priority for maximise rental cash flow at this stage of your portfolio.

Reviewing essential rental property tips regularly ensures your strategy adapts to changing market conditions rather than remaining static. Markets shift, and your rental property management tips framework should shift with them.

Remember that correct expense classification remains critical even when you are actively boosting cash flow. Overclaiming or misclassifying improvement costs as repairs is a common trigger for ATO scrutiny and can reverse the gains you have worked hard to achieve.

Verifying and monitoring cash flow: Maintaining peak performance

Once strategies are in place, you need checks and balances to keep your investments tracking in the right direction. Verification is not a one-time event. It is an ongoing discipline that separates high-performing portfolios from average ones.

Annual cash flow verification checklist:

- Reconcile actual rental income received against projected income

- Compare actual expenses to budget and identify variances over five per cent

- Confirm all deductions are correctly classified and supported by documentation

- Review your depreciation schedule for accuracy and completeness

- Check your loan structure and interest rate against current market offerings

- Assess vacancy periods and benchmark against local market averages

- Calculate actual pre-tax and after-tax cash flow and compare to your model

Note that borrowing expenses are spread over five years or the loan life, whichever is shorter, which means your deductible borrowing costs reduce each year. Factor this into your annual review to avoid overestimating deductions in later years.

| Review frequency | Key focus area | Action if off target |

|---|---|---|

| Monthly | Rent received vs expected | Chase arrears, review lease |

| Quarterly | Expense tracking vs budget | Renegotiate or reduce costs |

| Annually | Full pre and after-tax model | Adjust strategy or structure |

| Every 2 to 3 years | Depreciation schedule update | Commission updated report |

Pro Tip: Use a dedicated bank account for each investment property. This single habit makes reconciliation faster, reduces errors, and produces a clear audit trail that supports your tax position. Pair this with a rental appraisal review each year to ensure your rent is always aligned with the market.

Technology also plays a growing role here. Property management software and cash flow modelling tools allow you to track actuals against projections in real time, flagging issues before they become costly problems.

What most cash flow guides miss: Beyond the numbers

Armed with practical tools, let’s finish with a perspective most investors and guides overlook. The real risk in property cash flow planning is not a miscalculated spreadsheet. It is the gap between what your model shows and what your bank account actually experiences.

Most guides focus heavily on the calculation mechanics and the tax benefits of negative gearing. What they rarely address is the timing mismatch between cash outflows and tax refunds. You fund the shortfall every month. The refund arrives once a year, often months after the financial year ends. For investors with tight cash reserves, this lag creates genuine financial stress that no spreadsheet captures.

There is also a persistent confusion between “paper loss” and real cash loss. A property can show a significant tax loss on your return, thanks to depreciation and capital works deductions, while your actual out-of-pocket cost is far smaller. Conversely, a property that appears cash-flow neutral on paper can still drain your reserves if unexpected repairs or prolonged vacancy occur.

The most disciplined investors we work with model two separate layers: pre-tax cash flow, which is rent minus all cash costs and loan repayments, and after-tax cash flow, which includes the estimated tax refund. They never conflate the two. This discipline prevents the most common investor mistake: assuming a tax refund will solve a monthly cash problem.

The practical wisdom here is simple but powerful. Always check your actual bank flow, not just your projected spreadsheet. Review your transaction account monthly, not just at tax time. And maintain a cash buffer of at least three months of holding costs per property. This buffer is not a sign of poor planning. It is the foundation of a resilient portfolio.

Understanding the benefits of property investing in Australia goes well beyond yield calculations. It includes the confidence that comes from knowing your real cash position at every point in the year, not just when your accountant files your return.

Take your property portfolio further with expert support

If you’re ready to move from theory to action, Elite Wealth Creators is here to help you apply these principles and grow your property income with confidence. Our team specialises in translating complex cash flow modelling into clear, actionable strategies tailored to your portfolio and financial goals. Whether you’re building your first investment position or optimising an established portfolio, our property investing insights provide the strategic foundation you need. For investors focused on long-term wealth, explore our resources on unlocking financial freedom and discover how SMSF investment property benefits can further strengthen your position. Your vision, backed by our expertise.

Frequently asked questions

What is negative gearing and how does it impact my property cash flow?

Negative gearing means your rental expenses exceed income, creating a tax-deductible loss that may reduce your taxable income, but you still need to fund any cash shortfall throughout the year from your own resources.

What’s the difference between gross rental yield and net property cash flow?

Gross rental yield is your income as a percentage of property value before expenses, while net yield after expenses is a more accurate measure of what you actually retain and is the better metric for cash flow planning.

How can I improve the cash flow from my Australian investment property?

Focus on increasing rent to market rates, reducing management and operating costs, retaining quality tenants to minimise vacancy, and ensuring all eligible tax deductions including depreciation are correctly claimed each year.

Are all property expenses tax-deductible right away?

Some expenses like routine repairs are immediately deductible, while capital improvements and borrowing costs are spread over several years in line with ATO rules, so timing your claims correctly is essential.

Why does my cash position sometimes not match my tax results?

Depreciation and non-cash deductions can produce a paper loss for tax purposes even when your actual out-of-pocket costs are lower, which is why separating your pre-tax and after-tax cash flow models is so important for accurate planning.