TL;DR:

- A financial planner creates a comprehensive blueprint integrating property, tax, income, and retirement planning, not just managing investments. They provide holistic advice that improves long-term returns and offers psychological confidence, unlike advisors who focus solely on portfolio transactions. Engaging a qualified planner with full financial insight ensures coordinated decision-making and maximizes wealth-building potential.

Most people assume a financial planner is someone who picks stocks for you. That’s a costly misunderstanding. The true role of financial planner in investment is far broader: they build the blueprint around which every financial decision you make should fit. Your property holdings, superannuation, tax position, income streams, and retirement timeline are not separate puzzles. They are one picture. And without someone who sees all of it, your investment decisions will always be working with incomplete information. This article breaks down exactly what financial planners do, how they differ from advisors, and how to get the most out of working with one.

Table of Contents

- Key takeaways

- Financial planner vs financial advisor

- The holistic approach to investment strategy

- The real benefits of financial planning

- Understanding planner fee structures

- How to engage a financial planner

- My perspective on working with a planner

- Take the next step with Elitewealthcreators

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Planners vs advisors | Financial planners create a holistic financial roadmap; advisors focus on executing portfolio transactions. |

| Integration matters | Isolating investment decisions from tax, income, and retirement planning undermines long-term financial outcomes. |

| Measurable returns | Professional financial advice can add up to 4.87% more to annual portfolio returns over the long term. |

| Fee transparency | Ask upfront how your planner is compensated. AUM fees dominate, but flat and hourly models are growing. |

| Preparation pays | The more complete your financial picture when you engage a planner, the more precise and useful their advice will be. |

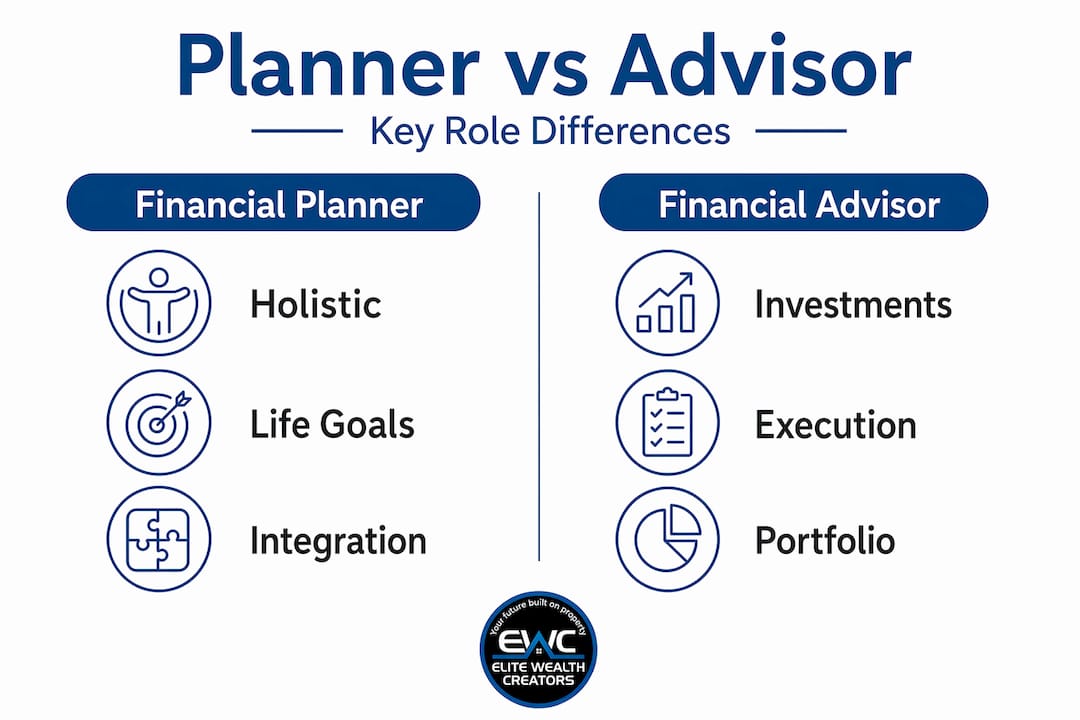

Financial planner vs financial advisor

People use these two terms interchangeably, and that confusion costs them. Understanding which professional you actually need is the first step toward getting real value from either.

Financial advisors focus primarily on investment execution. They manage portfolios, research asset classes, and make tactical decisions about where your money sits in the market. They are skilled at what they do, but their lens is narrow by design. Portfolio performance is their core metric.

Financial planners operate differently. They take a life-wide view, integrating your investments with your tax position, risk tolerance, insurance needs, estate planning, and retirement goals. Their product is a comprehensive financial roadmap that connects every financial decision you make to the outcomes you actually want. The investment portfolio is one component of that roadmap, not the whole picture.

Large institutions have started to separate these roles formally, with planners handling discovery and client relationships while advisors execute trades. It is a team-based model that reflects how distinct these functions genuinely are.

| Feature | Financial planner | Financial advisor |

|---|---|---|

| Primary focus | Holistic financial strategy | Investment portfolio management |

| Scope | Life-wide: tax, retirement, estate, risk | Asset selection and trade execution |

| Typical qualifications | CFP designation, fiduciary duty | Varies; may hold AFS licence |

| Best suited for | Long-term financial goal alignment | Tactical portfolio performance |

| Compensation | Flat fee, hourly, or AUM | Predominantly AUM-based |

Pro Tip: If a financial professional offers specific investment picks before asking about your income, debts, insurance, or retirement goals, treat that as a warning sign. Quality planners do not skip the discovery process.

The holistic approach to investment strategy

A financial planner’s value in investment is not about which assets they recommend. It is about the context they create before any investment decision is made.

Planners need a full financial snapshot before they can give responsible advice. Your income stability, debt structure, tax bracket, insurance coverage, and timeline to retirement all directly affect what investment strategy makes sense for you. Skip that context and you might build a high-growth portfolio that creates a significant tax liability you were not prepared for, or one that carries far more volatility risk than your income position can absorb.

The risks of separating investment management from planning are real. Without an integrated approach, there is no single professional with accountability for how your investments interact with your taxes, legacy goals, or income needs. You end up with advisors making decisions in silos, and the gaps between those silos are where wealth quietly erodes.

Here is what a coordinated planning approach actually covers:

- Tax-efficient asset placement: Determining which assets belong in super, which sit in a trust, and which are held personally to minimise tax drag.

- Cash flow modelling: Projecting how investment income interacts with living expenses, loan repayments, and future capital requirements.

- Risk management integration: Matching investment risk with income security and insurance coverage, not just with market benchmarks.

- Debt coordination: Structuring borrowings to support investment growth without undermining liquidity or serviceability.

- Legacy and estate alignment: Ensuring your investment structure supports ownership transfers and inheritance intentions.

- Retirement income sequencing: Planning the order and timing of drawing down assets to maximise longevity of funds.

For property investors specifically, this coordination is where significant value is found. Understanding how to structure property loans within a broader financial plan can be the difference between a portfolio that grows steadily and one that stalls due to poor cash flow management.

Pro Tip: Before engaging any financial planner, ask whether they will conduct a full financial review before making any recommendations. Those who skip straight to advice without this process are not doing comprehensive planning. They are doing something narrower and potentially less reliable.

The real benefits of financial planning

The data on this is not subtle. 74% of millionaires work with a financial advisor compared to just 34% of the general population. Those millionaires expect to retire two years earlier on average and report significantly higher levels of financial confidence.

Professional advice also shows up in portfolio performance. Industry estimates point to nearly 5% more returns annually with professional guidance over the long term. That is not a marginal gain. Compounded over a decade, it represents a fundamentally different retirement outcome.

But the benefits of financial planning go beyond numbers. One of the most underappreciated advantages is what researchers describe as “permission to spend.” Many disciplined savers reach retirement with substantial wealth and still feel they cannot spend it without anxiety. A financial planner provides the psychological clarity to make that transition. That is not a soft benefit. It directly affects quality of life during the years you have worked decades to reach.

“Having a financial planner is not about not knowing enough. It is about having someone who holds the full picture together so every decision you make is calibrated to your actual goals, not just the market conditions of the moment.”

| Study finding | Result |

|---|---|

| Millionaires using financial advisors | 74% versus 34% of general population |

| Expected earlier retirement with advisor | 2 years ahead of average |

| Annual portfolio return uplift | Up to 4.87% with professional advice |

| Psychological benefit identified | Permission to spend in retirement |

Understanding planner fee structures

Knowing what you will pay, and why, protects you from surprises and helps you choose the right professional.

AUM fees remain dominant, accounting for 72.4% of financial advisor revenue as of 2026. Under this model, you pay a percentage of the assets your planner manages, typically between 0.5% and 1.5% per year. The upside is alignment: the planner profits when your portfolio grows. The downside is that advice not tied to investable assets, such as insurance review or cash flow planning, may receive less attention.

Hourly and flat fee models are growing, with 21% of financial advisors now charging separate planning fees. These models suit people who want comprehensive planning without handing over portfolio management. You pay for the advice, not the assets.

Before you sign anything, ask these questions:

- How are you compensated, and does any part of your fee come from product recommendations?

- Do you charge separately for the initial discovery and financial review process?

- What services are included in your ongoing fee, and what sits outside it?

- How often will we review the financial plan and at what cost?

- Are you a fiduciary, meaning you are legally required to act in my best interest?

Fee clarity is not just about saving money. It tells you a great deal about how a planner operates and where their attention will naturally go.

How to engage a financial planner

Understanding the importance of a financial planner is one thing. Moving forward with one is another. Here is how to do it well.

-

Assess your situation honestly. Before approaching anyone, get clear on what you actually need. Are you at the accumulation stage, building a property or investment portfolio? Are you approaching retirement and need income sequencing advice? Your stage of wealth-building determines what kind of planner you need.

-

Gather your financial documents. Collect recent tax returns, super statements, loan documents, insurance policies, and any existing investment statements. The more complete your picture from day one, the more useful the first conversation will be.

-

Research credentials. In Australia, look for planners holding a Certified Financial Planner (CFP) designation or those registered with the Financial Adviser Standards and Ethics Authority (FASEA). Check the Australian Securities and Investments Commission (ASIC) financial advisers register before committing.

-

Conduct a discovery meeting. Most quality planners offer an initial meeting, sometimes at no cost, to assess fit. Use this to ask your fee questions, understand their process, and gauge whether they ask as many questions as they answer.

-

Review the Statement of Advice. Once engaged, your planner will provide a formal Statement of Advice (SOA) outlining their recommendations and rationale. Read it carefully and ask about anything that is not clear.

-

Schedule regular reviews. A financial plan is not a one-time document. Life changes, markets shift, and tax laws evolve. Annual or semi-annual reviews keep your investment strategy aligned with your current circumstances.

Pro Tip: When meeting a potential planner for the first time, pay close attention to whether they ask about your life goals before your asset balance. The best planners understand that money is a vehicle for the life you want, not the goal itself.

My perspective on working with a planner

I know a reasonable amount about financial markets, property investment, and tax structures. And I still have a financial planner. Not because I cannot read a balance sheet, but because I value having someone whose job it is to hold the whole picture and flag what I am too close to see clearly.

What I have found most useful is not the investment strategy guidance itself. It is the accountability. When you have someone who knows your full position, every financial decision you make gets considered in context rather than in isolation. I have caught myself about to make an investment move that looked clever in isolation but would have created a tax event I was not adequately prepared for. The planner saw it immediately.

The most common misconception I see is people treating planner fees as a cost rather than a structural advantage. The clients who get the most from the relationship are those who share everything, including the financial decisions they are embarrassed about or uncertain of. Holding back information from your planner is like hiding symptoms from a doctor and then wondering why the diagnosis is vague.

If you are a property investor, get a planner who understands property deeply. Not every planner does, and the difference in advice quality is significant.

— Nick

Take the next step with Elitewealthcreators

Understanding the role of a financial planner in investment is the first step. Acting on that understanding is where wealth actually gets built.

At Elitewealthcreators, we work with investors who are serious about integrating their property strategy with their broader financial goals. Whether you are looking to use equity for investment, assess SMSF property opportunities, or structure your portfolio for the next phase of growth, our team brings the strategic depth that standard agencies cannot offer.

If you are an SMSF trustee, the stakes are too high to leave property strategy to chance. Explore how SMSF property investment can work harder within your fund with the right guidance behind every decision.

We limit new client intake monthly, not for exclusivity, but because quality guidance demands proper attention. Spots are nearly gone. Stop watching opportunities close while you research. Contact Elitewealthcreators today.

FAQ

What is the main role of a financial planner in investment?

A financial planner integrates your investment strategy with your broader financial position, including taxes, income, risk, and retirement goals, to create a coordinated roadmap rather than managing a portfolio in isolation.

How is a financial planner different from a financial advisor?

Financial advisors focus on investment execution and portfolio management, while financial planners take a holistic view across your entire financial life, including estate planning, insurance, and long-term goal setting.

Can a financial planner improve my investment returns?

Yes. Professional financial advice can add up to 4.87% annually to portfolio returns over the long term, according to industry estimates, through better asset placement, tax efficiency, and disciplined strategy.

What questions should I ask a financial planner before engaging them?

Ask how they are compensated, whether they conduct a full financial review before advising, what services their fee includes, and whether they hold fiduciary responsibility to act in your best interest.

Do I need a financial planner if I already manage my own investments?

If you have property, superannuation, tax obligations, and personal income all running simultaneously, a financial planner adds value by coordinating those elements. Separating investment management from broader planning typically creates gaps in accountability and risk management.