TL;DR:

- Rentvesting allows Australians to invest in property markets while living in their preferred areas without delay.

- It involves renting in desirable locations while purchasing investment properties in more affordable markets to build wealth.

You don’t have to choose between living where you love and getting a foothold in the property market. That’s the assumption many Australians accept as fact, yet it keeps thousands on the sidelines, watching values climb while they wait for the “perfect” moment to buy in their preferred suburb. Rentvesting challenges that assumption directly. As reported by property experts, rentvesting can provide earlier exposure to the property market without sacrificing your desired location. This guide walks you through exactly how it works and how to do it strategically.

Table of Contents

- Understanding rentvesting: The basics

- Pros and cons of rentvesting

- How to choose the right investment property market

- Real-world rentvesting: Success stories and key pitfalls

- Our take: What most guides miss about rentvesting

- Ready to make rentvesting work for you?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Rentvesting explained | Rentvesting means renting where you want to live while owning an investment property elsewhere. |

| Benefits and risks | It can get you into the property market sooner but requires financial discipline and market research. |

| Market selection matters | Choosing the right area with strong rental demand is essential for success. |

| Not a one-size-fits-all | Rentvesting works best for those with the right financial profile and mindset. |

Understanding rentvesting: The basics

Rentvesting is a property strategy where you rent the home you actually want to live in, while simultaneously purchasing an investment property in a more affordable market. You maintain your lifestyle in a suburb or city that suits you, while your investment asset grows equity and generates rental income elsewhere. It’s a practical workaround to the affordability gap that defines so many Australian capital cities in 2026.

The strategy has gained significant traction because it separates two decisions that people often incorrectly bundle together: where you live and where you invest. These don’t need to be the same location. A professional renting in inner Melbourne, for instance, might invest in a well-selected property in regional Queensland or metropolitan Adelaide, where entry prices are lower and rental yields are stronger.

Here is what the core mechanics look like in practice:

- You rent a home in your preferred location, maintaining your lifestyle, commute, and social connections

- You buy an investment property in a location with strong rental demand and growth potential

- Your tenants effectively help service your mortgage through their rent payments

- You build equity in a real asset while retaining the flexibility renters enjoy

- You access tax advantages such as depreciation deductions and potential negative gearing benefits

As property experts note, getting into the property market sooner and keeping lifestyle choices while building equity via the investment property are two of the most commonly cited upsides of this approach.

“Rentvesting is not about settling for less. It’s about being strategic. You’re choosing where your capital works hardest, not just where it feels comfortable.” — Elite Wealth Creators Advisory Team

To understand the full picture of rentvesting explained, including how ownership structures affect your long-term tax position, it pays to look at the complete framework before committing.

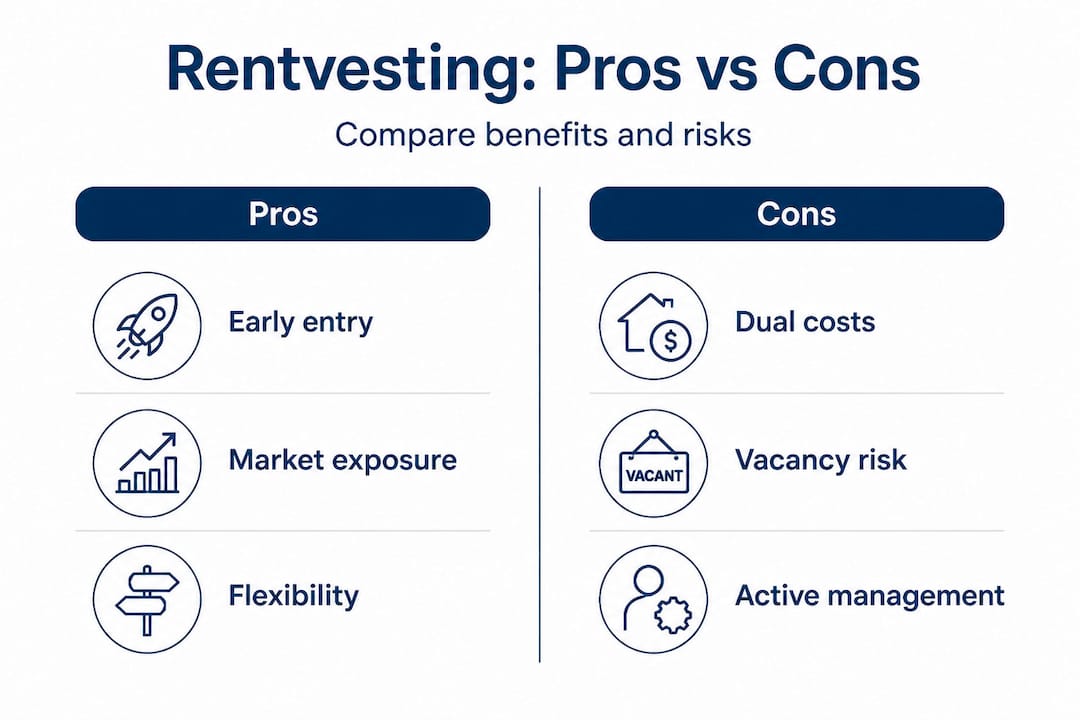

Pros and cons of rentvesting

With the basics covered, it’s important to weigh up what rentvesting delivers and where it might fall short. Like any investment strategy, rentvesting works well for some financial profiles and poorly for others. Understanding both sides protects your position.

Advantages of rentvesting

| Advantage | Detail |

|---|---|

| Earlier market entry | You invest now rather than waiting to save a deposit for your dream suburb |

| Lifestyle preservation | You continue renting in a location that suits your work and personal life |

| Equity building | Your investment property grows in value while tenants help cover the mortgage |

| Tax benefits | Potential deductions on interest, depreciation, and property expenses |

| Portfolio flexibility | You can scale your investment portfolio over time without being anchored to one property |

Challenges to consider

| Challenge | Detail |

|---|---|

| Dual housing costs | You pay rent while also servicing a mortgage, requiring strong cash flow management |

| Negative gearing risk | If rental income falls short of mortgage costs, you absorb the shortfall |

| Vacancy periods | Gaps between tenants reduce your income stream |

| No capital gains tax exemption | Unlike a principal place of residence, your investment is subject to CGT on sale |

| Emotional disconnect | Some investors find it harder to stay motivated about a property they don’t live in |

The strategy provides earlier exposure to the market rather than waiting on a “perfect” location, and that time advantage can be worth tens of thousands in capital growth alone. However, rentvesting works only for the right profile: it depends on cash flow buffers, the ability to absorb negative gearing shortfalls, and disciplined selection of investment property markets based on rental demand and vacancy risk.

The investors who thrive are those who approach it as a long-term wealth-building strategy rather than a quick fix. They maintain six to twelve months of expenses in reserve, understand their numbers inside out, and select investment properties with analytical rigour, not emotion.

Pro Tip: Before committing to rentvesting, run a detailed cash flow model covering your rent payments, mortgage repayments, property management fees, maintenance estimates, and vacancy allowances. If the numbers are tight, build your cash buffer before purchasing.

Explore high-return investing strategies to understand how rentvesting fits alongside other approaches in a diversified wealth-building portfolio.

How to choose the right investment property market

Once you know the pros and cons, selecting the right investment market becomes your next priority. This is where many rentvestors make their most significant error. They buy in a market they’re familiar with socially rather than one that suits their investment objectives financially.

Disciplined selection of the investment property market, with specific attention to rental demand and vacancy risk, is the critical variable that separates rentvestors who build wealth from those who stall.

Key market assessment criteria

| Factor | What to look for | Red flags |

|---|---|---|

| Rental yield | 4.5% and above for positive or neutral cash flow | Below 3.5% in expensive markets |

| Vacancy rate | Below 2% indicates strong demand | Above 3% suggests oversupply |

| Population growth | Infrastructure investment and population inflows | Declining or stagnant population |

| Employment diversity | Multiple industries driving local employment | Single-industry towns with cyclical risk |

| Supply pipeline | Limited new supply relative to demand | Oversupplied apartment markets |

Use this numbered framework to assess any prospective investment market:

- Research rental yield data from reputable sources to confirm the market’s income potential relative to purchase price

- Check vacancy rates for the suburb and surrounding area across at least the past 24 months to identify trends, not just snapshots

- Assess infrastructure investment by reviewing local council plans, government announcements, and major employer activity

- Examine the supply pipeline by identifying how many new dwellings are under construction or approved in the area

- Model your cash flow under both optimistic and conservative scenarios, including a 4-week vacancy buffer per year

- Stress-test your holding costs against a 1% to 2% interest rate increase to confirm you can still service the loan

Understanding which high-yield property types suit your target market is equally important. Houses in regional growth corridors often deliver stronger yields than inner-city apartments, which can suffer from body corporate fees, high strata levies, and competitive oversupply.

Pro Tip: Prioritise suburbs within 30 minutes of a regional city’s CBD or employment hub. These locations tend to attract stable, long-term tenants such as healthcare workers, government employees, and tradespeople, which reduces vacancy risk considerably.

Underpinning all of this is property market stability. You want a market that won’t swing dramatically, one where steady demand supports consistent rental income and moderate capital growth over a 7 to 10-year horizon.

Real-world rentvesting: Success stories and key pitfalls

Now that you know how to evaluate markets, it helps to see what actually works and what doesn’t in practice. The difference between a successful rentvestor and an unsuccessful one often comes down to preparation, patience, and process.

A typical success pattern looks like this:

- A buyer in their late twenties rents a two-bedroom apartment in Sydney’s inner west, paying $550 per week

- They purchase a four-bedroom house in a Queensland growth corridor for $480,000 with a 10% deposit

- The property rents for $480 per week, nearly covering the mortgage at current interest rates

- Over seven years, the property grows in value, their tenant base remains stable, and they refinance to access equity for a second purchase

- By their mid-thirties, they hold two investment properties and have not compromised their lifestyle once

This pattern is not hypothetical. It reflects the experience of disciplined investors who chose markets carefully, maintained cash flow buffers, and resisted the urge to over-extend.

“Keeping discipline and cash flow buffers is crucial for ongoing rentvesting success. The investors who struggle are those who cut corners on research or underestimate holding costs.”

Common pitfalls to avoid:

- Buying on emotion. Choosing a property because you find it appealing rather than because the numbers support it is a guaranteed path to cash flow problems.

- Ignoring vacancy risk. Some investors focus entirely on yield and overlook the possibility of extended vacancy periods, which can destroy annual returns quickly.

- Underestimating ongoing costs. Maintenance, property management fees, insurance, council rates, and water charges add up. Budget for 1% to 1.5% of the property’s value per year in holding costs beyond the mortgage.

- Failing to review the strategy annually. Market conditions change. A suburb that offered strong yields two years ago may have softened. Annual reviews keep your strategy current.

Accessing expert rental tips for investors helps you avoid the most costly mistakes before they occur. And once you’re a landlord, understanding managing rental properties effectively becomes your next critical skill set, whether you self-manage or engage a property manager.

Pro Tip: Always engage a qualified property manager in your investment market, even if their fees seem like an unnecessary cost. A skilled property manager reduces vacancy periods, attracts quality tenants, and handles maintenance issues promptly, often saving you more than their fees cost annually.

Our take: What most guides miss about rentvesting

Most articles about rentvesting focus almost entirely on the financial mechanics. They walk you through yield calculations, negative gearing tables, and deposit strategies, and stop there. What they rarely address is the psychological and strategic discipline the approach genuinely demands.

Rentvesting is not a passive strategy. It requires active management, consistent review, and a willingness to make decisions based on data rather than comfort. The investors who underperform are rarely those who chose the wrong market; they’re the ones who chose the right market initially and then stopped paying attention.

We also notice that most guides treat rentvesting as a beginner’s strategy, a stepping stone until you can afford your “real” home. We disagree with that framing entirely. Rentvesting is a legitimate long-term wealth vehicle that can be scaled across multiple properties over a decade or more. Some of Australia’s most sophisticated property investors continue to rent their primary residence indefinitely, because the capital they would lock into an owner-occupied property works far harder across a portfolio of income-generating assets.

The coming years in the Australian property market are likely to reward patient, research-driven investors who act decisively in well-selected markets. Population growth, constrained housing supply in key corridors, and sustained rental demand in regional centres all point to continued opportunities for rentvestors who approach the strategy seriously.

Exploring diversified property strategies beyond conventional residential investment is worth considering as your portfolio matures. Dual-income properties, NDIS housing, and co-living arrangements can dramatically enhance your returns when you have the right foundation in place.

The most important mindset shift rentvesting demands is this: stop thinking about property as a home first and an investment second. Think of your investment property as a business asset. When you do that, decisions become clearer, research becomes more disciplined, and results follow.

Ready to make rentvesting work for you?

Rentvesting is a strategy with genuine, proven potential, but it rewards those who plan carefully and act with clarity. If you’re considering this approach, start by building a solid understanding of your own financial position, then focus on market selection with the same precision you’d apply to any significant business decision. At Elite Wealth Creators, we specialise in helping Australian investors design and execute strategies like this from the ground up. Explore our property investing insights for data-driven guidance on where and how to invest in 2026. When you’re ready to take the next step toward unlocking financial freedom, our team is here to provide personalised support, off-market opportunities, and the strategic edge that separates confident investors from hesitant ones.

Frequently asked questions

Is rentvesting only for first-time property buyers?

No, rentvesting suits anyone wanting market exposure and lifestyle flexibility, not just first-time buyers. Experienced investors use rentvesting as a deliberate long-term portfolio strategy.

What are the main financial risks of rentvesting?

Key risks include negative gearing shortfalls, vacancy periods, and market downturns, because absorbing ongoing shortfalls and vacancy risk requires strong cash reserves and disciplined planning.

Can I rentvest if I’m self-employed or on a variable income?

Yes, but you’ll need strong cash flow buffers, because rentvesting works only for the right profile and variable income increases your exposure to shortfall periods if your investment property experiences vacancy.

How does rentvesting compare to buying your own home first?

Rentvesting lets you start building wealth sooner by entering the market earlier rather than waiting on a perfect location, while buying your home first prioritises stability and emotional connection to your chosen suburb.

Recommended

- From Rent-Vesting to Homeownership: Your Path to Property Investment | Elite Wealth Creators

- Maximise rental income: Expert strategies for Australian investors | Elite Wealth Creators

- Property Investment Success | Elite Wealth Creators

- 6 Must-Know Rental Tips for Aussie Investors | Elite Wealth Creators