TL;DR:

- Most Australian property investors overlook the benefits of property depreciation, a non-cash deduction that reduces taxable rental income by accounting for wear and tear. Properly claiming depreciation on structural and asset costs enhances cash flow without additional spending, provided documentation and schedules are accurate and compliant. Mastering depreciation strategies offers investors a significant, often overlooked, advantage in optimizing long-term investment returns.

Most Australian property investors are missing out on thousands of dollars each year, not because of poor property selection, but because they misunderstand one of the most powerful tools in their financial arsenal. What is property depreciation? It’s not money you spend. It’s not a bill. It is a legitimate, non-cash tax deduction that reduces your taxable rental income by reflecting the wear and tear on your investment property over time. Get it right, and you improve your cash flow without spending an extra dollar. This guide explains exactly how depreciation works under Australian tax law, what you can claim, and how to apply it to your portfolio with confidence.

Table of Contents

- What is property depreciation and why does it matter?

- How does depreciation work under Australian tax law?

- What assets and expenses can you claim depreciation on?

- How to calculate and claim depreciation to optimise your investment returns

- Comparing depreciation with other property investment tax benefits

- Why mastering property depreciation is your unfair advantage in investing

- How Elite Wealth Creators helps you unlock depreciation benefits

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Depreciation is a non-cash deduction | It reduces taxable rental income without requiring actual cash outlay each year. |

| ATO rules split depreciation | Capital works (building structure) and depreciating assets (fixtures) are claimed under different tax divisions. |

| Detailed depreciation schedules are essential | They identify all eligible assets ensuring you don’t miss valuable deductions. |

| Depreciation must be claimed correctly | Accurate claims reduce tax and avoid ATO audits, enhancing cash flow. |

| Combine depreciation with other deductions | Using depreciation alongside other tax benefits improves your investment returns. |

What is property depreciation and why does it matter?

Property depreciation explained simply: it is a tax deduction the Australian Taxation Office (ATO) allows you to claim for the natural decline in value of your investment property’s structure and its assets over time. You do not need to spend money in the current year to claim it. That is what makes it exceptional as a financial planning tool.

The ATO treats rental property depreciation as an income tax deduction for the decline in value of depreciating assets and, for buildings, capital works. These are non-cash deductions, meaning they reduce the income you are taxed on without requiring a corresponding cash outlay this financial year.

There are two distinct categories the ATO recognises:

- Capital works (Division 43): The structural elements of the building itself, such as walls, floors, roofing, and fixed construction.

- Depreciating assets (Division 40): Removable or mechanical items within the property, such as carpet, hot water systems, air conditioning units, and kitchen appliances.

“Depreciation is not a cost you incur today. It is recognition that the property and its contents are wearing down over time, and the tax system allows you to account for that decline as a legitimate deduction against your rental income.”

Understanding this distinction matters enormously. Many investors assume depreciation only applies to the building shell, when in reality the fittings and fixtures inside can represent a significant and separate stream of deductible value. You can read more about property tax deductions explained to see how depreciation sits within the broader picture of property depreciation basics and investment planning.

How does depreciation work under Australian tax law?

The ATO’s framework divides depreciation claims into two legislative divisions, each with its own rules, rates, and qualifying criteria. Knowing which division applies to which part of your property is how you avoid leaving deductions unclaimed.

Division 43 (capital works) covers the physical structure of the building. You can generally claim 2.5% per year of the original construction cost over 40 years, provided the building was constructed after 16 September 1987. Older properties may still qualify for partial deductions if significant renovations have been completed.

Division 40 (plant and equipment) covers assets that are not permanently fixed to the building structure. The ATO’s depreciation guidance makes clear that you claim deductions when the decline in value occurs and the property is used to produce assessable rental income.

Key rules to keep in mind:

- You can only claim depreciation on assets used to generate rental income. If the property is used privately for part of the year, your deductions are proportionally reduced.

- Depreciation claimed reduces your taxable income in the year of the claim, improving your after-tax cash position.

- Records and supporting documentation are not optional. The ATO expects you to substantiate every deduction with evidence, which is where a depreciation schedule becomes indispensable.

- Significant changes to how plant and equipment can be claimed for second-hand properties were introduced in 2017, so if you purchased an established property after 9 May 2017, different rules apply to existing fixtures.

Pro Tip: Commission a depreciation schedule before you lodge your first tax return on a new investment property. Backdating or reconstructing records later is far more costly and complicated than getting it right from the start. Your accountant will thank you. More detail on maximising rental deductions is worth reviewing before your next lodgement.

What assets and expenses can you claim depreciation on?

This is where investors frequently leave money on the table. The instinct is to focus on the obvious: the building itself. But identifying all eligible assets in renovations and removable fittings requires a level of categorisation most investors do not attempt without professional help.

Capital works (Division 43) includes:

- Structural walls, floors, and roofing

- Fixed windows and doors

- Driveways and fencing

- In-ground swimming pools

- Initial fit-out costs (for new buildings)

Plant and equipment (Division 40) includes:

- Carpet and floating floorboards

- Hot water systems

- Ovens, dishwashers, and rangehoods

- Air conditioning units

- Blinds and curtains

- Light fittings and exhaust fans

What you cannot depreciate:

- Land. Property value decline reasons are numerous, but land itself has no depreciable value under Australian tax law.

- Assets not connected to producing rental income.

- Second-hand plant and equipment purchased in an established property after 9 May 2017, unless you are the original owner or the asset is new.

A step-by-step approach to ensure you capture everything:

- Engage a qualified quantity surveyor to inspect the property in person.

- Have them identify and categorise every claimable asset under Division 40 and Division 43.

- Obtain written evidence of original construction costs or purchase prices where available.

- Include all renovation costs completed after acquisition, as these can generate fresh depreciation entitlements.

- Update the schedule whenever you make improvements or significant repairs.

Pro Tip: Renovations you complete after purchasing a property can open entirely new depreciation streams. Even repainting walls or replacing carpet creates fresh deductible amounts under the correct categories. Learn more about claimable depreciation assets and how to capture them properly.

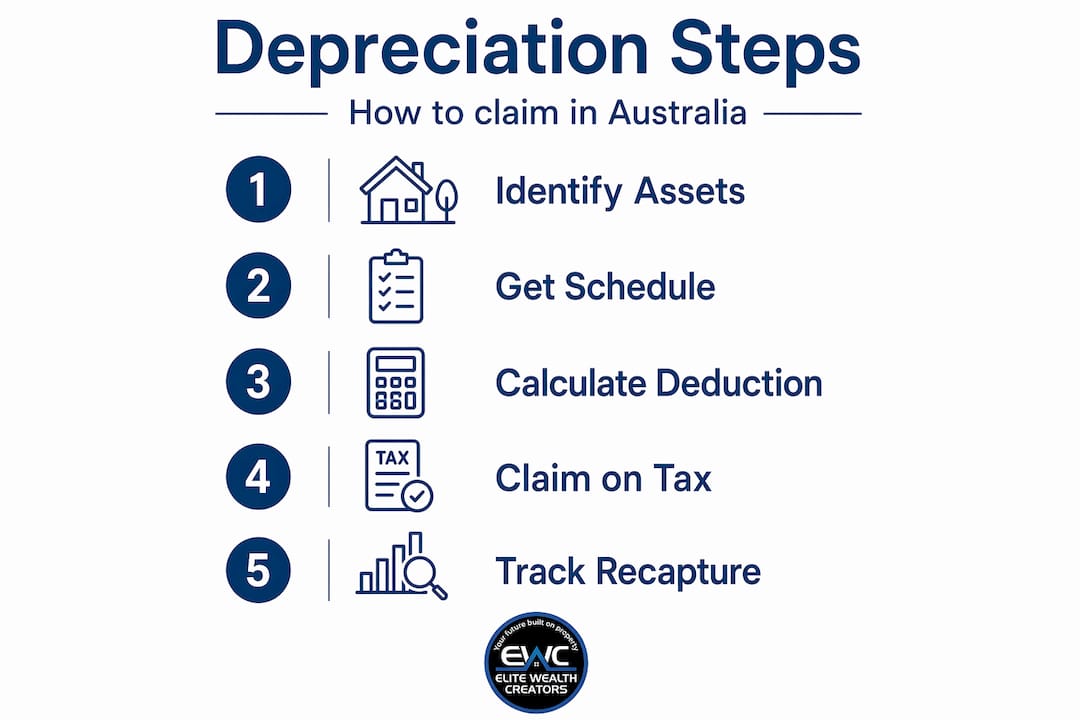

How to calculate and claim depreciation to optimise your investment returns

Calculating property depreciation for tax purposes is not something you do on instinct. It requires accurate data, correct categorisation, and a method approved by the ATO. Here is how the process works in practice.

Step-by-step claim process:

- Engage a quantity surveyor. This is the recognised professional for preparing depreciation schedules on investment properties. They assess the property’s construction costs, installed assets, and renovation history to produce an evidence-based depreciation schedule.

- Divide claims by division. Your schedule will separate Division 43 capital works deductions from Division 40 plant and equipment deductions, each with its own annual rate and effective life calculation.

- Choose a depreciation method for assets. The two ATO-approved methods for plant and equipment are the prime cost method (equal deductions each year) and the diminishing value method (higher deductions in earlier years, reducing over time). Most investors favour diminishing value for early cash flow benefits.

- Include the schedule in your annual tax return. Your accountant uses the schedule figures to complete the rental income schedule and apply the correct deductions.

- Maintain thorough records. Purchase contracts, construction invoices, renovation receipts, and the schedule itself must be kept for five years after the relevant tax year.

| Depreciation method | Year 1 deduction | Year 5 deduction | Best suited to |

|---|---|---|---|

| Prime cost | Lower, equal each year | Same as Year 1 | Long-term holds |

| Diminishing value | Higher in early years | Lower than Year 1 | Early cash flow improvement |

| Capital works (Div 43) | 2.5% of construction cost | 2.5% of construction cost | Building structure only |

Understanding depreciation recapture is also important. When you eventually sell the property, the ATO may require that previously claimed depreciation deductions be accounted for in your capital gains tax calculation. This is not a reason to avoid claiming, but it is a reason to plan your exit strategy with a qualified tax adviser. Read more about the depreciation claiming process before you make your next move.

Comparing depreciation with other property investment tax benefits

Property depreciation does not operate in isolation. Understanding how it sits alongside other available deductions gives you a clearer picture of your total tax position and helps you plan more effectively.

| Tax benefit | Cash or non-cash | Claimed against | Frequency |

|---|---|---|---|

| Depreciation (Div 40 and 43) | Non-cash | Rental income | Annual |

| Loan interest | Cash | Rental income | Annual |

| Property management fees | Cash | Rental income | Annual |

| Repairs and maintenance | Cash | Rental income | As incurred |

| Insurance premiums | Cash | Rental income | Annual |

The significance of depreciation is precisely that it is non-cash by nature, reducing your taxable income without any actual money leaving your account in that financial year. Every other deduction on the list above requires you to first spend money, then claim it back. Depreciation is unique in that the “expense” is the passage of time and use.

Key points of distinction:

- Repairs restore an asset to its original condition and are immediately deductible. Improvements, however, must be depreciated over time, not claimed all at once.

- Loan interest is your largest cash deduction in most cases, but it fluctuates with interest rate movements. Depreciation is predictable and consistent.

- Combining all available deductions, including depreciation, produces the most accurate picture of your actual taxable rental income. Investors who treat these in isolation consistently pay more tax than necessary.

For context on how depreciation fits your long-term wealth building roadmap, understanding capital growth vs depreciation as complementary forces in your investment strategy is well worth your time.

Why mastering property depreciation is your unfair advantage in investing

Here is what most depreciation articles will not tell you: the investors who benefit most from depreciation are not necessarily those with the most expensive properties. They are the ones who understand it well enough to demand a thorough schedule rather than a generic one.

We have seen investors receive schedules from quantity surveyors that miss entire renovation components, or that default to minimum values for plant and equipment rather than establishing accurate replacement costs. The difference between getting depreciation right and getting it approximately right can be thousands of dollars annually across a portfolio of two or three properties.

There is also a common misconception that depreciation only matters if you are in a high tax bracket. This is incorrect. Any taxable income you reduce means less tax paid, regardless of your marginal rate. For investors building towards financial independence, preserving cash flow in the early years of a portfolio is exactly where depreciation pays its most significant dividends.

The other risk worth naming directly: non-compliance. Claiming depreciation on ineligible assets, or claiming at the wrong rate, is not a minor error. The ATO’s data matching capabilities have improved considerably, and an audit triggered by depreciation inconsistencies can result in penalties and interest that far exceed the original deduction. Accuracy, not aggression, is the right approach.

Depreciation is not paperwork. It is a financial lever. Pulled correctly, with the right professional support and current knowledge of ATO rules, it is one of the few tools available to you that consistently improves your after-tax returns without requiring you to take on additional risk. Explore our expert property tax tips for practical guidance across your investment journey.

How Elite Wealth Creators helps you unlock depreciation benefits

At Elite Wealth Creators, we understand that knowing the theory is only half the equation. Applying it to your specific portfolio, ownership structure, and financial goals is where the real work begins. Our team connects you with trusted quantity surveyors who produce thorough, ATO-compliant depreciation schedules that leave nothing on the table. We also provide guidance for SMSF property investment where depreciation compliance carries additional complexity. Whether you are building your first rental portfolio or expanding an established one, our invest smart property insights give you the clarity to act decisively and grow confidently. Ready to see what your properties could really be returning? Start by unlocking financial freedom with a team that treats your goals as their own.

Frequently asked questions

Can I claim depreciation on my primary residence?

No, depreciation applies only to investment properties generating rental income. Your own home is not eligible, regardless of its age or construction type.

How do I get a depreciation schedule for my rental property?

You engage a qualified quantity surveyor who inspects your property and prepares a detailed schedule with item-by-item values for all eligible capital works and plant and equipment.

Can I claim depreciation on renovations I make after purchase?

Yes, provided the renovations meet ATO criteria for depreciating assets or capital works and the property is used to produce assessable rental income, renovation costs generate fresh and claimable depreciation.

Does claiming depreciation reduce my property’s resale value?

No. Depreciation is a tax deduction that reflects loss in value over time on paper; it has no direct effect on what a buyer will pay for your property in the market.

What happens if I don’t claim depreciation on my rental property?

The ATO assumes you have claimed depreciation when calculating capital gains tax on sale, which means failing to claim during ownership gives you a tax liability at the end without the benefit along the way.