TL;DR:

- Property syndication allows Australians to pool funds for high-value assets with passive management.

- Investments typically lock in for 4 to 7 years with target yields of 7 to 8.25%.

- Success depends on a competent syndicator, thorough due diligence, and understanding illiquidity risks.

Property syndication isn’t just a strategy for wealthy investors with deep pockets. It’s a proven vehicle that lets everyday Australians pool their capital to access high-value commercial and residential assets that would otherwise be out of reach. Think of it as co-ownership, structured and managed professionally, with each investor holding a proportional stake. Whether you’re building a portfolio alongside your SMSF or looking for income-producing assets beyond the typical house or unit, understanding how syndication works could reshape your investment outlook. This guide covers how syndicates are structured, the risks involved, the potential returns, and how to assess whether this approach suits your financial goals.

Table of Contents

- Understanding property syndication in Australia

- How property syndicates work: Process from start to finish

- Comparing syndicate types: Single-asset vs multi-asset

- Key risks and rewards of property syndication

- Why property syndication opportunity is bigger — and riskier — than most realise

- Next steps: Start building wealth with expert guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Access bigger assets | Property syndication lets everyday investors own a share of large-scale properties with a lower capital outlay. |

| Understand the risks | Syndicates lock funds for years and require thorough research on the manager and asset. |

| Diversification benefits | Multi-asset property syndicates help spread risk and can offer more stable returns. |

| SMSF caution | SMSFs can benefit but also face strict rules and scam risks in syndication deals. |

Understanding property syndication in Australia

At its core, property syndication is a formal arrangement where multiple investors pool their funds to collectively purchase and manage a property asset. Instead of buying a property outright, you buy a share of a larger asset, typically via a unit trust or similar legal structure. Each investor holds units proportional to their capital contribution, and returns are distributed accordingly.

The key players in any syndicate are:

- The syndicator (or syndicate manager): The experienced operator who identifies the asset, structures the deal, manages the property, and communicates with investors.

- The investors: Individuals or entities (including SMSFs) who contribute capital in exchange for income distributions and potential capital growth.

- The trustee: Often a corporate entity responsible for holding the asset on behalf of investors and ensuring compliance with legal obligations.

Before investing, you’ll typically receive an information memorandum, which is a formal document that outlines the property details, investment terms, projected returns, risks, and the syndicator’s track record. Read it carefully. It is one of the most important documents you’ll encounter in this process.

Minimum investment amounts generally start around $25,000 to $50,000, making entry more achievable than purchasing a standalone commercial property. Syndicates target yields of 7 to 8.25% plus capital growth, with historical averages exceeding 13% over time and typical terms running 4 to 7 years. Once committed, your capital is largely illiquid until the asset is sold or refinanced.

Syndication differs from direct property ownership in several important ways. You don’t manage tenants, organise maintenance, or deal with council approvals. That responsibility sits with the syndicator. What you do manage is your due diligence upfront and your portfolio strategy over time. For investors interested in SMSF property syndicates, there are additional compliance requirements to understand before committing funds.

Pro Tip: Don’t confuse a property syndicate with a listed property trust. Syndicates are typically unlisted, which means pricing is not transparent in real time and liquidity is limited. Understanding this distinction matters before you commit capital.

How property syndicates work: Process from start to finish

Investing in a property syndicate follows a defined lifecycle. Understanding each stage helps you set realistic expectations and make more informed decisions.

- Syndicate launch and capital raising: The syndicator identifies a target asset, conducts feasibility analysis, and prepares the information memorandum. Investors are invited to participate and commit their capital within a specified window.

- Settlement and asset acquisition: Once sufficient capital is raised, the property is purchased and ownership is established through the chosen legal structure, typically a unit trust.

- Active asset management: The syndicator manages the property, handles leasing arrangements, maintains the asset, and distributes income to investors on a regular basis, usually quarterly.

- Reporting and communication: Investors receive regular financial statements, tax information, and updates on property performance and market conditions.

- Exit via sale or refinance: At the end of the syndicate term, the asset is sold or refinanced. Proceeds are distributed to investors after costs, and the syndicate is wound up.

Property syndicate terms run 4 to 7 years, with capital generally locked in until the asset is sold or refinanced. Plan your liquidity needs accordingly.

The investor’s role throughout this process is relatively passive. You contribute capital, receive income distributions, and monitor reporting. You don’t make day-to-day decisions about the property. This makes syndication attractive for busy professionals and retirees who want income-producing exposure to real estate without the operational burden.

Your exit from the investment is tied to the syndicate’s timeline, not your personal cash flow needs. This is why understanding the property syndicate process in detail before committing is so critical. If your circumstances change mid-term, you may have very limited options to access your funds early.

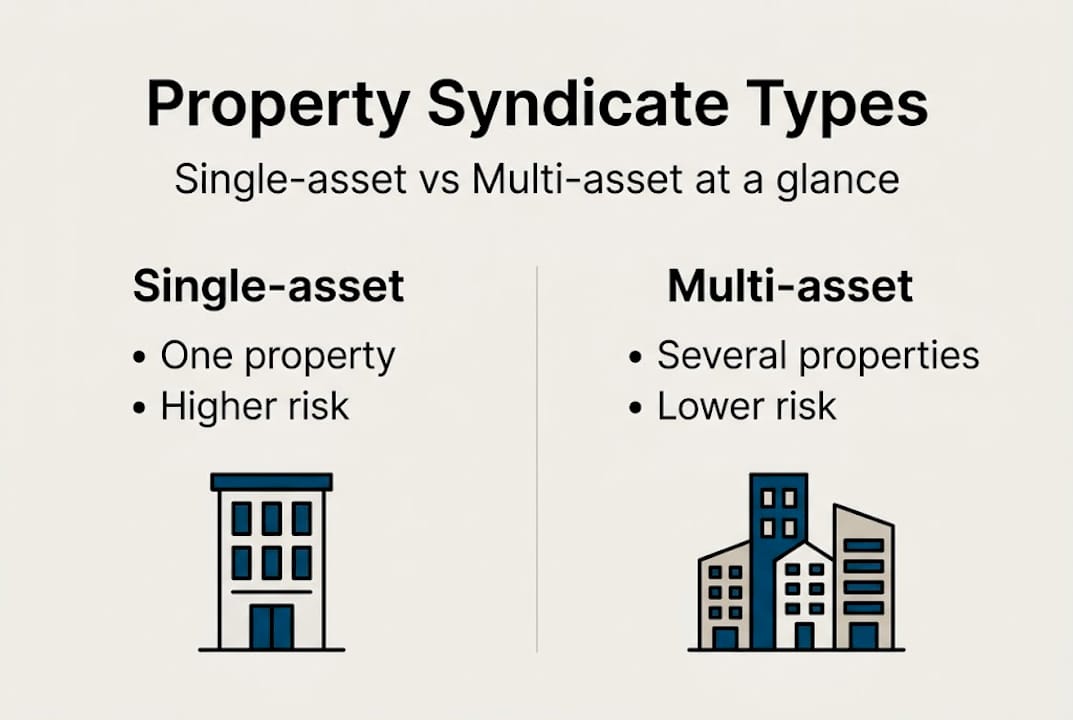

Comparing syndicate types: Single-asset vs multi-asset

Not all property syndicates are built the same way. Two primary models exist, and your choice between them should reflect your risk tolerance and investment goals.

Single-asset syndicates focus on one specific property, such as a commercial office building, industrial warehouse, or retail centre. They offer targeted exposure to a particular sector or location and can generate strong returns if the asset performs well.

Multi-asset syndicates pool capital across several properties, spreading risk across different locations, tenants, and property types. This diversification can smooth out income volatility if one asset underperforms.

| Feature | Single-asset syndicate | Multi-asset syndicate |

|---|---|---|

| Risk profile | Higher concentration risk | Lower concentration risk |

| Return potential | High if asset performs | Moderate, more consistent |

| Liquidity | Low | Slightly better |

| Transparency | Clear focus on one asset | More complex to assess |

| Best suited for | Experienced investors | Newer or risk-averse investors |

Single-asset syndicates offer targeted exposure but carry higher concentration risk, while multi-asset structures provide broader diversification and potentially better liquidity.

Key considerations when choosing between models:

- Tenant risk: A single-asset syndicate relying on one major tenant is highly exposed if that tenant vacates.

- Sector exposure: Multi-asset syndicates let you spread across industrial, retail, and commercial, reducing sector-specific downturns.

- Management complexity: More assets mean more variables for the syndicator to manage, which requires a more experienced team.

For investors building diversified property portfolios, a multi-asset approach often makes sense as a starting point, before concentrating in specific assets as experience grows.

Pro Tip: New investors consistently underestimate concentration risk in single-asset syndicates. If the tenant leaves, the valuation drops, or the sector softens, you have no buffer. Always ask what happens to your distributions if the anchor tenant vacates.

Key risks and rewards of property syndication

Every investment carries risk. Property syndication is no exception, and a clear-eyed assessment of both sides of the ledger is essential before committing.

| Risk | Potential reward |

|---|---|

| Illiquidity (locked 4 to 7 years) | Target yields of 7 to 8.25% p.a. |

| Syndicator underperformance | Historical averages exceeding 13% |

| Concentration in one asset | Access to institutional-grade assets |

| Market and gearing risks | Capital growth on exit |

| SMSF-related party scam exposure | Portfolio diversification |

Illiquidity is the risk most investors underestimate. Once you commit, your funds are largely locked until the syndicate exits. There is generally no secondary market to sell your units quickly. Plan your overall cash flow to ensure you can absorb this.

Syndicator quality is arguably the single most important variable in your outcome. A poorly managed syndicate can erode returns through bad tenancy decisions, over-gearing, or inadequate maintenance reserves. Always review the syndicator’s track record and ask for references from previous investors.

For SMSF investors, the ATO has flagged specific risks around related-party property development scams, where SMSF funds are funnelled into arrangements that benefit connected parties rather than the fund itself. Regulatory compliance is non-negotiable.

Before investing, ask yourself:

- What is the syndicator’s track record over the past 10 years?

- How is the property valued, and by whom?

- What are the exit options if my circumstances change?

- How is the syndicator remunerated, and are their interests aligned with mine?

- What gearing (borrowing) is applied, and how does that affect risk?

For investors comparing historical returns across asset classes, well-structured syndicates have demonstrated competitive performance. But past performance doesn’t guarantee future results, and the fundamentals of each deal must be assessed individually. Reviewing SMSF investment risk tips is strongly recommended before proceeding.

Why property syndication opportunity is bigger — and riskier — than most realise

Property syndication genuinely opens doors that were previously closed to everyday Australian investors. Access to commercial-grade assets, professional management, and income distributions that rival or exceed residential yields are real advantages. We’ve seen investors build meaningful wealth through well-chosen syndicates, and the opportunity is not overstated.

But here’s what the promotional brochures rarely say: passive income through syndication is conditional on a syndicator who is competent, honest, and well-incentivised. Many investors treat the passive nature of syndication as meaning low effort across the board, including during due diligence. That’s where things go wrong.

Illiquidity also deserves more attention than it typically receives. Seven years is a long time. Markets shift, personal circumstances change, and a syndicate that looked ideal in year one may feel restrictive by year four. Diversification within syndication itself, across multiple syndicates, sectors, and managers, is a strategy far too few new investors consider.

Trust the fundamentals. An expert view on SMSF property consistently reinforces that opportunities promising unusually high returns with minimal explanation deserve extra scrutiny, not excitement. Sound assets, experienced operators, and clear alignment of interests remain the foundation of any successful syndicate investment.

Next steps: Start building wealth with expert guidance

Property syndication can be a powerful addition to your investment portfolio, offering access to assets and income streams that most individual investors can’t reach alone. The key is matching the right syndicate structure to your financial goals, risk profile, and timeline. At Elite Wealth Creators, we specialise in helping Australian property investors navigate exactly this kind of decision with clarity and confidence. Explore our resources on smarter investing strategies and discover how SMSF property opportunities could work for your situation. Take the first step toward unlocking financial freedom with guidance built around your vision.

Frequently asked questions

How much money do I need to join a property syndicate in Australia?

Minimum investments typically start from $25,000 to $50,000, though this varies depending on the syndicate structure and the asset being acquired.

Are property syndicates safe for my SMSF?

SMSF property syndicates can be effective, but the ATO warns of related-party scams and illiquidity risks, making compliance checks and thorough due diligence essential before committing your super.

What is the typical holding period for a property syndicate?

Most property syndicates have a holding period of 4 to 7 years, and your capital is generally locked until the asset is sold or refinanced at the end of the term.

What’s the difference between a syndicate and a property trust?

A property trust is typically an ongoing, often listed investment vehicle, while a property syndicate is structured around a specific asset or group of assets with a defined investment term and a planned exit.