Choosing a home loan based purely on the lowest advertised rate is one of the most common and costly mistakes Australian borrowers make. Many Australians select loans based solely on headline rates, often ignoring longer-term cost risks that can erode financial security over time. Whether you are a first-home buyer trying to manage a tight budget or a seasoned property investor protecting rental cash flow, understanding the real value of a fixed rate loan could reshape your entire financial strategy. This guide walks you through what fixed rate loans are, their core benefits, how they compare to variable alternatives, and exactly when choosing one makes strategic sense.

Table of Contents

- What is a fixed rate loan and how does it work?

- Major benefits of fixed rate loans for Australians

- Fixed rate vs variable rate loans: key differences

- When choosing a fixed rate loan makes the most sense

- Why most Australians misunderstand fixed loans and what experts know

- Take your next step with expert loan guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Repayment stability | Fixed rate loans let you budget with certainty by locking in your interest rate for several years. |

| Best for rising rates | Fixed loans can shield you from increases if the Reserve Bank of Australia lifts rates. |

| Know the trade-offs | Breaking a fixed loan early can be costly, and flexibility is often limited. |

| Property investor advantage | Knowing exactly what you’ll pay helps investors manage cash flow and plan ahead. |

| Check your fit | Evaluate your own priorities and life plans before choosing fixed or variable rates. |

What is a fixed rate loan and how does it work?

A fixed rate loan is exactly what it sounds like: your interest rate stays the same for an agreed period, regardless of what the broader market does. A fixed rate loan locks in your interest rate for a set period, usually one to five years in Australia. After that fixed term expires, your loan typically reverts to the lender’s standard variable rate, unless you negotiate a new fixed arrangement.

The mechanics are straightforward. You and your lender agree on a rate at settlement, and your repayments remain identical every month for the entire fixed period. There are no surprises when the Reserve Bank of Australia (RBA) adjusts the cash rate. Your repayment stays locked, giving you a clear picture of your outgoings at all times.

When exploring home loan options, it helps to understand the core features of fixed rate products before committing. Here is what defines them:

- Rate locked in: Your interest rate does not move during the fixed term, regardless of RBA decisions.

- Payment predictability: Every repayment is identical, making monthly budgeting simple and reliable.

- Limited flexibility: Most fixed loans restrict extra repayments and do not offer full offset account functionality.

- Break costs apply: Exiting the loan early usually triggers a break fee, which can be substantial.

- Rollover at term end: At expiry, the loan moves to a variable rate or you can refix at current market rates.

Understanding property buying essentials means recognising that loan structure is just as important as purchase price. The fixed rate home loans category suits borrowers who value certainty over flexibility.

Pro Tip: The best time to fix your rate is when interest rates are rising or expected to rise. Locking in before further RBA increases can save you thousands over the fixed term.

Major benefits of fixed rate loans for Australians

Now that you understand how fixed rate loans work, it is worth examining why so many Australian homeowners and investors actively choose them. The advantages go well beyond simple peace of mind.

Fixed repayments provide budgeting confidence, protecting against RBA rate rises that can push variable repayments higher without warning. For families managing household expenses, investors balancing rental income against loan outgoings, and first-home buyers stretching their budgets, this predictability is genuinely powerful.

“Knowing your exact repayment for the next three years is not just comforting, it is a strategic advantage. It allows you to plan asset acquisition, manage cash reserves, and model future investment moves with real confidence.”

When you secure a home loan on a fixed rate, you are essentially buying certainty. That certainty has real dollar value, particularly in volatile rate environments. The pros and cons of fixed rate loans are well documented, but the stability benefit consistently stands out for those with structured financial goals.

For property investors, the advantage is even more pronounced. Rental income is often relatively stable month to month, so matching it against a fixed loan repayment creates a clean, predictable cash flow model. You know your net position without running complex calculations every time the RBA meets.

Here is a quick summary of who benefits most from a fixed rate loan:

- Families on a set income who need reliable monthly budgeting without rate shock.

- Property investors managing rental yield against loan repayments across a portfolio.

- First-home buyers who are stretching their borrowing capacity and cannot absorb rate increases.

- Risk-averse borrowers who prioritise financial security over chasing potential savings.

- Borrowers in rising rate environments who want to lock in before further increases take hold.

The key insight here is that choosing a fixed rate is not a passive or fearful decision. It is a deliberate, strategic move to protect your financial position while you pursue growth.

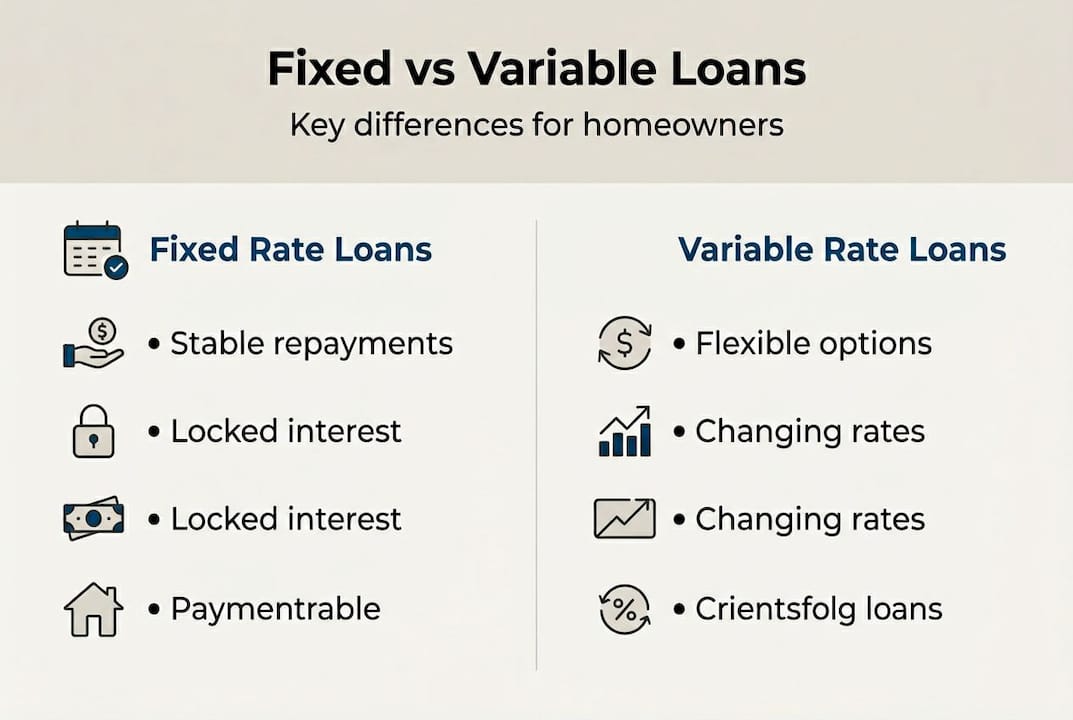

Fixed rate vs variable rate loans: key differences

To make an informed decision, you need a clear view of how fixed and variable loans differ. Variable rates can move both up and down, while fixed rates remain steady for a set period. That single distinction creates a cascade of differences in how each loan type affects your finances.

Variable loans offer flexibility. You can usually make unlimited extra repayments, access offset accounts, and refinance without paying break costs. But your repayments shift every time the RBA adjusts the cash rate, which introduces genuine financial uncertainty.

The Finder fixed vs variable loan guide outlines these trade-offs in detail. Here is a direct comparison:

| Feature | Fixed rate loan | Variable rate loan |

|---|---|---|

| Interest rate certainty | Locked for fixed term | Moves with market |

| Repayment predictability | Identical each month | Changes with rate moves |

| Extra repayments | Usually limited or capped | Typically unlimited |

| Offset account | Rarely available | Commonly available |

| Break costs | Yes, can be significant | Generally none |

| Refinancing flexibility | Restricted during fixed term | High flexibility |

| Potential for savings | If rates rise, you win | If rates fall, you win |

There are also some common misconceptions worth addressing when comparing fixed vs variable loans:

- Myth: Fixed always costs more. Not true. If rates rise during your fixed term, you save compared to variable borrowers.

- Myth: Variable is always riskier. In a falling rate environment, variable loans can reduce your repayments significantly.

- Myth: You cannot switch. You can exit a fixed loan, but break costs make it expensive, so timing matters.

- Myth: Fixed loans have no features. Some lenders offer limited offset accounts and redraw on fixed products.

The right choice comes down to your priorities. If security and cash flow certainty matter most, fixed wins. If flexibility and potential savings appeal more, variable deserves consideration.

When choosing a fixed rate loan makes the most sense

With a clear view of both loan types, the next question is straightforward: when does fixing your rate actually make strategic sense for your situation?

Fixed rates are attractive when the RBA is expected to lift official rates further. But rate expectations are just one factor. Here are the top scenarios where fixing your rate is a smart move:

- You expect interest rates to rise. Locking in before further RBA increases protects you from higher repayments.

- Your cash flow is tight. A fixed repayment removes the risk of unexpected increases straining your budget.

- You need budgeting certainty. Families and investors with structured financial plans benefit from knowing exact outgoings.

- You are building a property investment portfolio. Fixed loans make cash flow modelling across multiple properties far more precise.

- You are a first-home buyer. Certainty during your early ownership years reduces financial stress while you build equity.

- You are planning major life changes. Starting a family, changing careers, or undertaking renovations all benefit from predictable loan costs.

Before you fix, run through this quick decision checklist. Ask yourself: Do I need flexibility to make extra repayments? Am I likely to sell or refinance within the fixed term? Do I have an emergency buffer to absorb rate changes if I stay variable? Is my income stable enough to manage potential variable rate increases?

If your answers point toward stability over flexibility, fixing is likely the right move. For those who want a middle ground, consider reviewing buying property tips alongside your loan strategy.

Pro Tip: A split loan divides your borrowing between fixed and variable portions. This gives you repayment certainty on part of your debt while retaining flexibility, such as offset accounts and extra repayments, on the variable portion.

Refinancing considerations matter too. If you fix your rate and then want to refinance within the term, break costs can be significant. Always model the break cost scenario before committing to a fixed period.

Why most Australians misunderstand fixed loans and what experts know

Here is an uncomfortable truth: most borrowers approach fixed loans defensively, as though fixing is something you do when you are scared of rate rises. Experts see it very differently.

Many Australians focus solely on initial savings, but experts balance security, flexibility, and long-term gains when structuring loan arrangements. The smartest property investors we work with do not ask “which rate is lower right now?” They ask “which loan structure best protects my ability to keep acquiring assets?”

Fixing your rate is often about protecting opportunities, not just capping risk. When your repayments are locked, your cash flow is predictable. Predictable cash flow means you can plan your next acquisition with confidence, rather than waiting to see what the RBA does next month.

Many borrowers also switch out of fixed loans too late, missing the window where break costs are lowest and market conditions are most favourable. Timing a fixed rate entry or exit is a skill, and it requires understanding market cycles, not just current rates. The right loan structure is a vehicle for wealth creation, not just a cost to minimise.

Take your next step with expert loan guidance

At Elite Wealth Creators, we understand that choosing between fixed and variable loans is rarely a simple decision. It involves your income, your investment goals, your risk tolerance, and your long-term wealth strategy. Our team specialises in helping Australian homeowners and property investors structure their financing for maximum stability and growth.

Explore our property investing insights to see how smart loan structuring fits into a broader wealth creation strategy. Our mortgage types guide gives you the full picture across all loan options available in the Australian market. When you are ready to move from knowledge to action, our advisers are here to help you build the right blueprint.

Frequently asked questions

Can I break a fixed rate loan early in Australia?

Yes, but break costs may apply if you pay out or refinance your loan during the fixed period, and these fees can be substantial depending on how much rates have moved.

What happens when my fixed rate period ends?

At the end of the fixed term, the loan usually switches to the standard variable rate, so it pays to review your options and renegotiate well before expiry.

Are fixed rate loans suitable for property investors?

Fixed loans are popular with investors looking for certainty during volatile markets, as they allow precise cash flow modelling across a property portfolio.

Do fixed rate loans offer offset accounts or extra repayments?

Not all fixed loans offer the same features as variable loans, such as offset accounts, and extra repayments are often capped or restricted depending on the lender.

Recommended

- Top Australian Mortgage Options in 2023 for Smart Borrowing | Elite Wealth Creators

- Why refinance your home: a guide for Australians 2026 | Elite Wealth Creators

- 5 innovative ways to finance property in Australia 2026 | Elite Wealth Creators

- What is property refinancing: a smart guide for Australian homeowners 2026 | Elite Wealth Creators