TL;DR:

- Proper preparation, including pre-approval and detailed budgeting, prevents costly property mistakes.

- Using a subject-to-finance clause and avoiding cross-collateralisation safeguards your investment flexibility.

- Conducting independent inspections and leveraging cooling-off periods reduce legal and structural risks.

Picture this: a first-time buyer in Melbourne signs a contract, pays a deposit, and then discovers their finance application has been knocked back by the bank. No subject-to-finance clause in the contract means the deposit is gone. That single oversight cost them over $20,000 and set their property goals back by two years. Property mistakes like this happen every week across Australia, and they affect not just first-timers but also experienced investors who skip key steps under time pressure. This guide walks you through the exact preparation, process, and verification steps you need to protect your money and your long-term wealth strategy.

Table of Contents

- What you need before searching for property

- Step-by-step: avoiding finance and lending traps

- Conducting due diligence the right way

- Common mistakes that trip up Aussie buyers

- Why most buyers underestimate property risks (and what matters more)

- Take the next step with expert property guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Get finance pre-approval | Always secure written finance pre-approval before making offers on property. |

| Use independent inspections | Invest in independent building and pest inspections to avoid hidden surprises. |

| Avoid lender traps | Never cross-collateralise your properties and use subject-to-finance clauses for buyer protection. |

| Understand your contract | Read and review contracts thoroughly, seeking legal or expert advice where needed. |

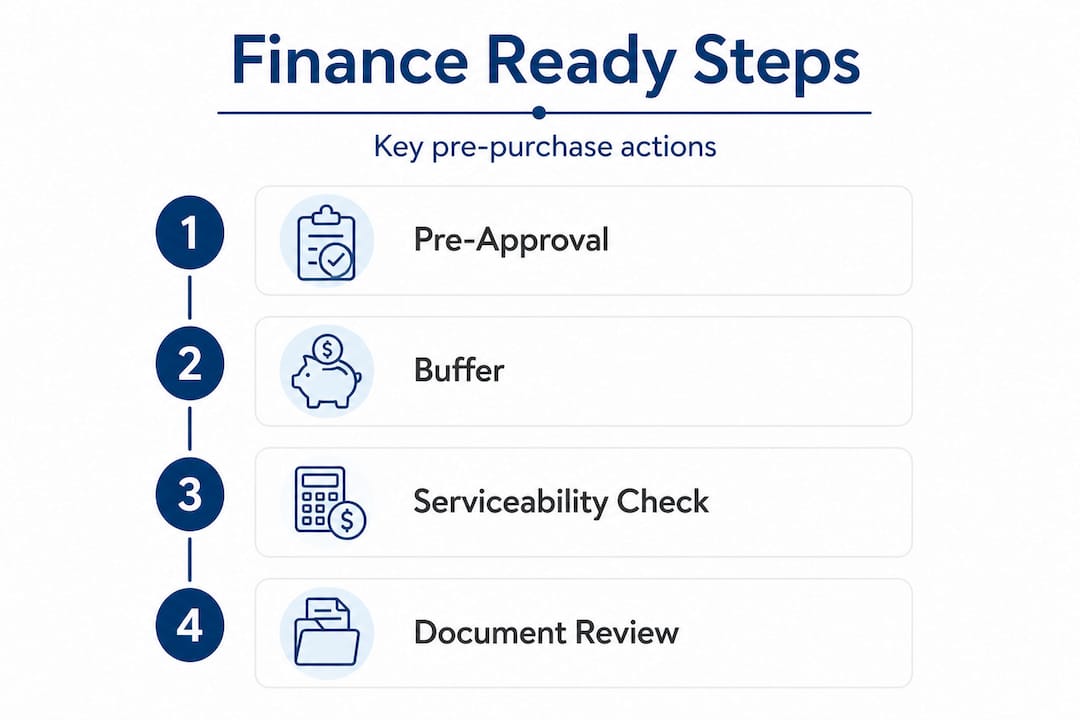

What you need before searching for property

Now that you know the stakes, let’s get prepared. Here’s where to start before you even view your first property.

The single most important step before you attend any open home is securing home loan pre-approval. Pre-approval is a written confirmation from a lender that they are willing to lend you a specific amount based on your current financial position. It is not a guarantee of finance, but it is far stronger than a verbal estimate or an online calculator result. Without it, you are essentially shopping blindfolded.

Critically, you must also test your serviceability by calculating whether you can still afford repayments if interest rates rise by 2 to 3 per cent above your current rate. Australian lenders are legally required to apply a buffer, but you should run that number yourself and make sure the repayments remain genuinely comfortable, not just technically possible. Many buyers focus on what the bank will lend them rather than what they can realistically manage month to month.

Setting a realistic budget means going beyond the purchase price. You need to account for stamp duty, legal fees, building and pest inspections, mortgage insurance (if your deposit is below 20 per cent), council rates, and ongoing maintenance. These costs regularly add 5 to 7 per cent on top of the property price. Missing them is one of the most common ways buyers overstretch their finances right from the start.

Before you begin searching, compile a clear list using the property buying essentials framework:

- Must-haves: Non-negotiable features such as minimum bedroom count, proximity to schools or transport, or specific zoning requirements for investors

- Nice-to-haves: Features you would prefer but could live without, such as a double garage or a north-facing backyard

- Dealbreakers: Factors that would cause you to walk away regardless of price, such as flood zone classification, a shared driveway, or a property under a flight path

| Preparation step | Why it matters | Risk if skipped |

|---|---|---|

| Written finance pre-approval | Confirms borrowing capacity | Loss of deposit if finance fails |

| Interest rate stress test (+2-3%) | Ensures long-term affordability | Mortgage stress or forced sale |

| Full budget including costs | Prevents cash shortfall at settlement | Delayed settlement or default |

| Property criteria list | Keeps decisions objective | Emotional overpaying |

Pro Tip: Do not use pre-approval as your absolute ceiling. Build a buffer of at least 5 per cent below your maximum approval amount so you have room for bidding competition, unexpected costs, or minor rate increases before settlement.

Step-by-step: avoiding finance and lending traps

With your preparation done, it’s time to start the process. But avoiding finance traps is key to a smooth transaction.

Finance mistakes are among the most financially damaging errors a property buyer can make. The good news is that they are almost entirely preventable with the right structure in place. Follow these steps carefully.

-

Get written pre-approval, not an estimate. A verbal nod from a broker or an online calculator result carries no legal weight. Only a written pre-approval from a lender counts, and even then, read the conditions attached carefully.

-

Always include a subject-to-finance clause in your offer. This clause gives you the right to withdraw from the contract without penalty if your finance application is not approved within the agreed timeframe. Without it, you may forfeit your deposit if the deal falls through.

-

Understand what a subject-to-finance clause covers. It typically specifies a lender, a loan amount, and a deadline. If the lender changes terms or reduces the approved amount significantly, you may still have grounds to exit, but this depends on how the clause is worded. Always have a conveyancer review it.

-

Avoid cross-collateralisation. Cross-collateralisation (also called cross-collateralizing) is when one lender uses two or more of your properties as combined security for a single loan. It sounds convenient, but it means the lender controls the relationship between all assets. If you want to sell one property, refinance, or access equity from another, you need the lender’s permission. This severely restricts your flexibility as a portfolio grows.

-

Use multiple lenders for portfolio growth. Experienced investors diversify their lenders to maintain control over individual properties. If all your properties are with one lender, that lender holds significant power over your entire portfolio. Using different lenders for different properties keeps each asset independent and preserves your ability to refinance, sell, or restructure at will.

-

Review your finance strategies regularly. Interest rates, your income, and your portfolio goals all change over time. An annual review of your loan structures ensures you are not paying a loyalty tax to your existing lender or sitting on a rate that has quietly become uncompetitive.

| Approach | Flexibility | Risk level | Recommended for |

|---|---|---|---|

| Single lender, cross-collateralised | Low | High | Not recommended |

| Single lender, separate loans | Medium | Medium | Early-stage investors |

| Multiple lenders, separate loans | High | Low | Portfolio builders |

Pro Tip: When negotiating a contract of sale, ask your conveyancer to specify the exact lender and loan amount in the subject-to-finance clause. A clause that is too vague may not protect you if a dispute arises.

Conducting due diligence the right way

So you have sorted your finance. Now let’s make sure the property really stacks up and you are not buying hidden problems.

Due diligence is the formal process of investigating a property before you commit to purchasing it. Many buyers rush this stage, especially in a competitive market where properties seem to sell within days. That urgency can lead to extremely costly shortcuts.

Follow these steps for thorough due diligence:

-

Commission an independent building inspection. A qualified building inspector will assess the structural integrity of the property, identify defects, and flag safety issues. Do not rely on a report that the vendor or agent has provided. Vendor-supplied independent reports may omit unflattering findings or lack the liability that comes with a report commissioned specifically for you.

-

Commission a separate pest inspection. Termite damage in Australia is a serious and surprisingly common issue. Pest inspections are often bundled with building inspections, but in older properties or high-risk areas, consider engaging a specialist pest inspector independently.

-

Review the contract of sale with a licensed conveyancer or solicitor. Contracts can contain special conditions, easements, encumbrances, or restrictions on use that significantly affect the property’s value or your plans for it. Never sign a contract without professional legal review.

-

Check for unapproved structures. Illegal extensions, pergolas, or granny flats that were built without council approval can become your liability the moment you settle. Always request council records and check what permits exist for any structures on the property.

-

Use your cooling-off period wisely. In most Australian states, buyers have a cooling-off period of 2 to 5 business days after signing a contract of sale. This gives you time to commission inspections, review legal documents, and confirm your finance position before you are fully committed.

“First home buyers often skip inspections or contract reviews, risking illegal builds or special levies. Always use cooling-off periods and independent reports rather than relying on vendor-provided ones.” This is not a minor procedural step. It is your primary legal protection between signing and settling.

Key items to check when reviewing a contract of sale:

- Zoning and planning restrictions

- Any registered easements or caveats on the title

- Special conditions added by the vendor

- Settlement timeframes and deposit terms

- Inclusions and exclusions (fixtures, appliances, chattels)

- Body corporate levies and meeting minutes for strata properties

Visit our property buyer tips resource for a more detailed checklist, and review the property ownership steps that experienced buyers use to reach settlement without surprises.

Common mistakes that trip up Aussie buyers

Even with checklists and processes, some mistakes remain all too common. Here are the major threat points to watch for.

Overstretching the budget with hidden costs is the number one financial trap. Buyers focus on the purchase price and forget stamp duty can add 4 to 5 per cent in states like New South Wales and Victoria. For a $750,000 property, that is an extra $27,000 to $37,000 before you have paid a single dollar of legal or inspection fees.

Skipping inspections or contract reviews to move faster in a competitive market is a false economy. A $600 building inspection that reveals $30,000 in structural issues is the best money you will ever spend. A legal review that identifies an encroachment or unapproved extension protects you from disputes that can drag on for years.

Failing to plan for interest rate rises is a pattern that recurs in every property cycle. Many buyers who entered the market in 2021 with rates at historic lows were suddenly managing repayments that jumped hundreds of dollars per month as rates rose sharply through 2022 and 2023. Always stress test at +2 to 3 per cent above your current rate before committing.

Cross-collateralising properties is a trap that catches many investors as their portfolios grow. It feels efficient to keep everything with one lender, but the risks of cross-collateralisation compound over time. When you want to sell one asset, refinance another, or access equity, you will need the lender’s approval for all connected properties simultaneously.

Here is how to protect yourself:

- Always maintain a cash buffer of at least 3 months of repayments

- Review your loan structures annually with a mortgage broker

- Keep individual properties on separate loan facilities wherever possible

- Get professional legal advice before signing any complex contract

Pro Tip: If you realise you have made a mistake post-settlement, do not panic. Contact a mortgage broker immediately to explore refinancing options. Many structural finance issues can be resolved, but the sooner you act, the more options remain available to you.

Learn more about avoiding costly investment mistakes and use the step-by-step buying guide to keep every stage of your purchase on track.

Why most buyers underestimate property risks (and what matters more)

Let’s challenge the bigger picture thinking that dominates property conversations in Australia.

Every week, someone quotes “location, location, location” as the guiding principle of property investment. And while location genuinely matters, that maxim has become a crutch that gives buyers permission to skip rigorous process. The idea is that if you buy in the right suburb, the market will forgive your mistakes. That belief has cost many investors dearly.

Long-term property success in Australia comes far more from rigorous process than from picking a hotspot. The investors we see build sustainable portfolios are not necessarily the ones who found the most exciting suburbs. They are the ones who built disciplined acquisition frameworks, reviewed their finance structures regularly, and had the courage to walk away from deals that did not fully stack up.

The sunk cost fallacy is a real and dangerous force in property. After months of searching, paying for inspections, and emotionally committing to a property, the pressure to proceed regardless of warning signs is intense. Walking away from a bad deal after spending $1,500 on inspections and legal advice is still the correct decision if the numbers or the property condition do not justify the purchase price. That $1,500 is already spent whether you proceed or not.

We also see buyers underestimate the value of portfolio diversification strategies in managing risk over time. Concentrating all your capital in a single asset class, one suburb, or one loan structure amplifies the impact of any single adverse event.

The most decisive investors we work with share one habit: they treat every deal as if they are the only buyer in the room, not as if they must compete for it at any cost. That mindset change alone can prevent most of the pitfalls outlined in this article.

Take the next step with expert property guidance

If you are ready to invest wisely while sidestepping the traps others fall into, Elite Wealth Creators provides the specialised strategic support to help you do exactly that. From finance structuring and independent due diligence guidance to off-market access and portfolio planning, our team works with first home buyers and experienced investors alike. Explore our property investing insights to understand how a disciplined strategy drives better outcomes, and review our property investing guide to see how our clients build wealth with greater confidence and less risk at every stage of the acquisition process.

Frequently asked questions

What is cross-collateralisation and why should I avoid it?

Cross-collateralisation links multiple properties to one loan, limiting your flexibility and increasing risk if you need to sell or refinance. Diversifying across lenders is the most effective way to maintain independent control over each asset in your portfolio.

How do subject-to-finance clauses protect buyers?

A subject-to-finance clause allows you to withdraw from a property contract without penalty if your finance application is not formally approved within the agreed timeframe. This protects your deposit if a lender declines or significantly changes the terms of your loan.

Is it safe to rely on a vendor-supplied building inspection?

No. Vendor-supplied reports may not carry the same liability protections as an inspection you commission yourself, and they may omit details unfavourable to the sale. Always engage your own independent building inspector before signing unconditionally.

What’s a cooling-off period and why is it important?

A cooling-off period is your legal right to withdraw from a property purchase within a short window after signing the contract, typically 2 to 5 business days depending on your state. It gives you protected time to complete final inspections and review legal documents without forfeiting your deposit.