Off-plan property investing promises something rare in the Australian market: the ability to lock in today’s price and watch your asset grow before you even receive the keys. But that promise comes with real complexity. Off-plan property can yield strong capital gains while also exposing buyers to project delays, developer insolvency, and contract traps that catch unprepared investors off guard. This guide gives you a proven, evidence-based roadmap covering every stage of the process, from initial research through to settlement, so you can move forward with clarity and confidence.

Table of Contents

- What is buying off-plan?

- Key benefits for investors

- Common risks and how to protect yourself

- Step-by-step buying process

- Investor’s checklist: legal and financial essentials

- Stamp duty concessions: how much can you save?

- Unlock expert support for your next off-plan investment

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Price lock-in advantage | Buying off-plan enables you to secure a property at today’s prices, with potential for capital growth by settlement. |

| Mitigate key risks | Always safeguard your purchase with a thorough contract review, trusted developers, and legal protections. |

| Stamp duty savings | Off-plan buyers can qualify for substantial stamp duty concessions, but rules differ by state. |

| Follow a structured process | A disciplined, step-by-step approach avoids pitfalls and ensures your investment delivers the desired returns. |

What is buying off-plan?

Buying off-plan means committing to purchase a property before construction is complete, sometimes before a single brick has been laid. As comparethemarket.com.au explains, you are purchasing based on developer plans, renders, and a contract of sale rather than a finished product you can inspect. This is fundamentally different from buying an established home, where what you see is what you get.

Developers sell this way for practical reasons. Pre-sales give them the financial evidence lenders need to fund construction, which means your commitment helps the project get off the ground. In return, you gain access to property buying basics at an earlier stage, often at a price that reflects today’s market rather than tomorrow’s.

Key characteristics of off-plan purchases include:

- You sign a contract and pay a deposit, typically 10%, well before completion

- Settlement occurs once the property receives an occupancy certificate

- The finished product may differ slightly from the original plans

- Your borrowing capacity is assessed at the time of settlement, not signing

For investors, the core appeal is price lock-in. If the market rises during the construction period, which can span 18 to 36 months, you benefit from capital growth without having paid the full purchase price upfront.

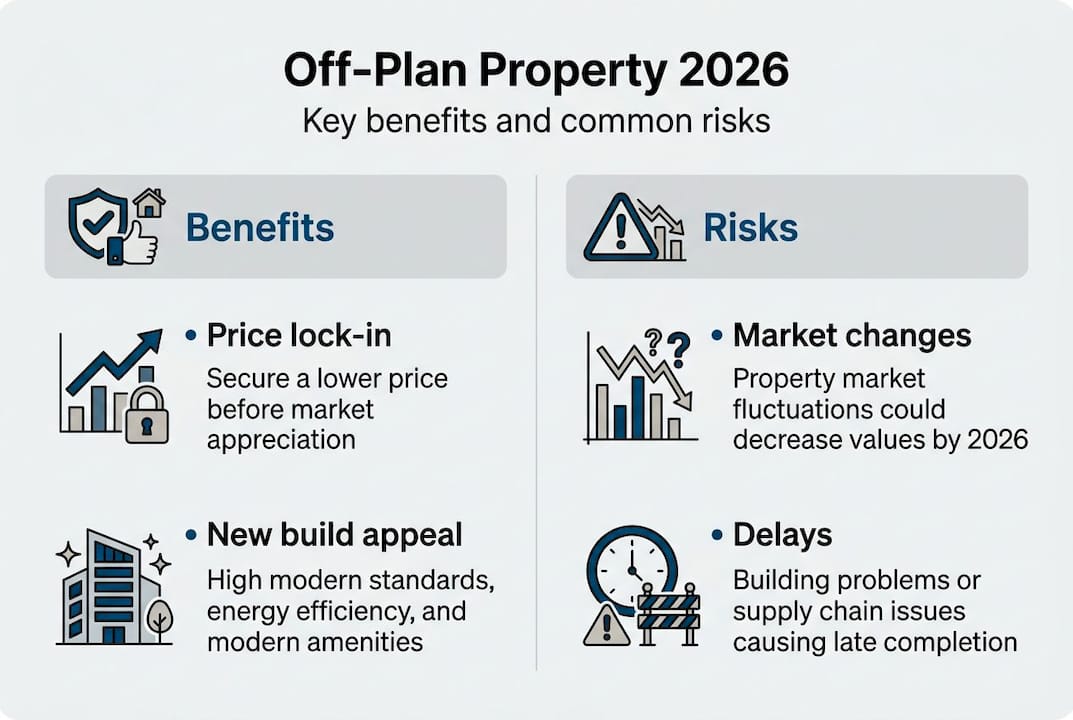

Key benefits for investors

Understanding the basics, investors should next assess the concrete advantages on offer. The financial case for off-plan investing is compelling when the conditions are right.

According to savingsmate.com.au, investors can lock in today’s price, capture capital gains, reduce stamp duty, and maximise tax depreciation on new builds. These four levers, working together, can significantly improve your overall return compared to buying established property.

Key benefits at a glance:

- Capital growth: In strong markets, investors have recorded gains of $60,000 to $100,000 between contract signing and settlement

- Stamp duty concessions: Many states apply duty only to the land value or offer discounts for off-plan purchases, reducing upfront costs substantially

- Tax depreciation: New builds attract maximum depreciation claims, improving your annual cash flow position

- Modern appeal: New properties attract quality tenants and typically carry lower maintenance costs in the early years

- Price certainty: You know your purchase price from day one, which aids long-term cash flow modelling

| Benefit | Established property | Off-plan property |

|---|---|---|

| Stamp duty | Full market value | Often reduced or land value only |

| Depreciation | Limited (older assets) | Maximum (brand new) |

| Capital growth timing | Immediate | Locked in at signing |

| Maintenance costs | Higher (older fixtures) | Lower (new build warranty) |

Explore apartment investment benefits to see how new builds compare across different asset classes in the current market.

Pro Tip: Request a quantity surveyor’s depreciation schedule before settlement. On a new apartment, this can generate $8,000 to $15,000 in annual tax deductions, meaningfully improving your after-tax yield from day one.

Common risks and how to protect yourself

While the rewards are enticing, no investor should act without first weighing the hazards and knowing how to reduce them. The risk landscape for off-plan buyers has shifted considerably in recent years.

Developer insolvency and buyer protection data confirms that construction delays, valuation shortfalls, and developer insolvency have all risen since 2024, with 2,832 construction companies recorded as insolvent in the 2024 to 2025 financial year. That is not a reason to avoid off-plan investing. It is a reason to invest with rigour.

The main risks to understand:

- Construction delays: Projects routinely run 6 to 12 months beyond the original timeline, affecting your finance pre-approval and rental income projections

- Developer insolvency: If your developer collapses mid-build, your deposit should be protected in trust, but the project may stall or be sold to another party

- Valuation shortfalls: At settlement, your bank may value the completed property below your contract price, creating a finance gap you must cover with cash

- Sunset clauses: Some contracts allow developers to rescind the agreement if construction is not completed by a set date, potentially leaving you without the property in a rising market

- Defects and variations: The finished property may include material changes from the original plans, or present defects that require rectification

Always ensure your deposit is held in a statutory trust account, not released to the developer until settlement. This is your primary financial safeguard.

For off-plan buyer protections in New South Wales, the government mandates specific trust account requirements and disclosure obligations. Other states have comparable frameworks, though the details vary.

Understanding investing risks and security at a portfolio level will help you position off-plan assets appropriately within your broader strategy. You should also review property finance issues before committing, particularly around how lenders assess borrowing capacity at settlement versus signing.

Pro Tip: Negotiate a longer sunset clause, ideally 36 months or more, and include a clause that prevents the developer from invoking it opportunistically in a rising market. Your solicitor can advise on the specific wording.

Step-by-step buying process

With risks addressed, it is time for the critical step-by-step method that paves the way for investment success. The major steps include setting your budget, securing pre-approval, researching developers, paying your deposit, reviewing the contract, monitoring the build, and completing settlement.

- Assess your budget and borrowing power. Calculate your usable equity, savings, and maximum loan serviceability before you look at any project. Know your numbers before you fall in love with a floor plan.

- Research developers and suburbs. Investigate the developer’s track record, completed projects, and financial standing. Focus on suburbs with strong population growth, infrastructure investment, and rental demand.

- Secure finance pre-approval. Obtain conditional pre-approval from a lender before signing anything. Note that lenders will reassess your position at settlement, so maintain your financial position throughout the build.

- Select your unit and pay the deposit. Choose your preferred lot and pay the initial deposit, typically 10% of the purchase price, into a statutory trust account. Confirm this in writing.

- Engage your solicitor for contract review. This is non-negotiable. Your solicitor should scrutinise the sunset clause, deposit handling terms, variation rights, defect liability periods, and any special conditions. Review the off-plan buying process in detail before signing.

- Sign the contract and monitor construction. Once satisfied, execute the contract. Request regular construction updates and attend any site inspection opportunities offered by the developer.

- Conduct a pre-settlement inspection. Before you finalise finance and attend settlement, inspect the property thoroughly. Document any defects or variations in writing and ensure they are addressed or acknowledged before you settle.

The stepwise buying process and property essentials resources can help you prepare for each stage with greater confidence.

Pro Tip: Keep a dedicated folder, physical or digital, for every document related to your off-plan purchase. Contracts, correspondence, inspection reports, and finance approvals should all be stored and dated. This protects you if disputes arise at settlement.

Investor’s checklist: legal and financial essentials

To supplement the buying steps, keep this investor’s checklist close at hand for every transaction. Missing even one item can expose you to significant financial or legal risk.

Before signing:

- Confirm the deposit will be held in a statutory trust account, not released to the developer

- Have your solicitor review the full contract of sale, including all schedules and special conditions

- Verify the sunset clause duration and the conditions under which it can be triggered

- Confirm the developer’s rights to make variations and the threshold at which you can withdraw

- Check the developer’s history: completed projects, litigation history, and financial standing

For foreign investors:

- Assess your Foreign Investment Review Board (FIRB) obligations before signing

- Confirm GST obligations, as new residential property attracts a 10% GST component at settlement

- Review duty and grant eligibility to ensure you are not missing available concessions

Ongoing:

- Maintain your financial position to support reassessment at settlement

- Keep your pre-approval current and communicate with your lender throughout the build

- Arrange building insurance from the date of settlement, not before

As comparethemarket.com.au advises, always use a solicitor for the contract, check the developer’s track record and deposit handling, and watch carefully for GST and FIRB requirements. Review the full off-plan checklist to ensure nothing is overlooked.

Pro Tip: Ask the developer for a copy of their project registration and development approval before you commit. A legitimate developer will provide these without hesitation.

Stamp duty concessions: how much can you save?

With legal and financial safeguards outlined, you should also factor in state-specific stamp duty concessions, often the biggest upfront saving available to off-plan buyers. Stamp duty savings and eligibility depend on state policy and property status, so always verify the current rules before you rely on a figure.

| State | Concession type | Potential saving |

|---|---|---|

| New South Wales | Duty on land value only (pre-construction) | Up to $20,000 |

| Victoria | Stamp duty discount extended to October 2026 | Up to $28,000 on a $620,000 apartment |

| Queensland | Investor relief available in select circumstances | Varies by property and buyer type |

| South Australia | Stamp duty abolished for eligible new builds | Significant savings for qualifying buyers |

In Victoria, the off-plan stamp duty concessions framework means a buyer purchasing a $620,000 apartment off-plan in 2026 could save approximately $28,000 compared to buying the same property after completion. That is a material difference in your upfront capital requirement.

Key points to check in your state:

- Whether the concession applies to investors or only owner-occupiers

- The property value cap above which the concession phases out

- Whether the concession applies at contract date or settlement date

- SMSF-specific rules, which can differ from individual buyer entitlements

For South Australian investors, explore stamp duty changes in Adelaide and review SMSF stamp duty advice if you are purchasing through a self-managed super fund.

Unlock expert support for your next off-plan investment

Off-plan investing rewards those who combine market knowledge with disciplined process. Every step in this guide, from developer research through to pre-settlement inspection, is designed to protect your capital and position you for genuine long-term growth. But knowing the steps and executing them with precision are two different things, and that is where expert guidance makes a measurable difference.

At Elite Wealth Creators, we work alongside investors at every stage of the off-plan journey, from identifying high-potential projects to navigating contract negotiations and finance structures. Whether you are building your first investment portfolio or adding a strategic asset to an existing one, our team provides the insight and access you need. Explore how to invest smart for property wealth growth and discover the pathways available for unlocking financial freedom through well-structured property investment.

Frequently asked questions

How much deposit do I need to buy off-plan in Australia?

Most off-plan purchases require a 10% deposit into trust, held securely until the property reaches completion and settlement occurs.

What happens if the developer goes bust before completion?

Your deposit held in trust is generally protected, but insolvencies have increased dramatically since 2024, meaning you may face settlement delays, contract rescission, or the need to find an alternative property.

Are there stamp duty savings for off-plan investments in all states?

Substantial concessions exist in most states, but savings and eligibility depend on state policy, property value, and buyer type, so always verify the current rules before you budget.

Can I negotiate contract terms when buying off-plan?

Yes, and you should. Experts recommend negotiating buyer-friendly terms including longer sunset clauses and clear deposit protections, always with your solicitor’s guidance.

What if the bank values my property at less than I paid?

Valuation shortfalls are a top risk at settlement, so maintain a financial buffer and discuss lender’s mortgage insurance options with your broker well before the settlement date arrives.

Recommended

- Step by step property buying guide for Australian first-timers 2026 | Elite Wealth Creators

- Step by step land purchase guide for Australian buyers 2026 | Elite Wealth Creators

- Budget planning for home buyers: a practical guide 2026 | Elite Wealth Creators

- Step-by-Step Mortgage Approval: Boost Borrowing 30% in 2026 | Elite Wealth Creators