Buying your first property or planning an investment in Australia can quickly become confusing when you face the question of Lenders Mortgage Insurance. Many believe this insurance protects their interests, but the reality is it’s a policy that solely benefits financial institutions, especially when your deposit is less than 20 percent of the property’s value. Understanding the difference between myth and fact about Lenders Mortgage Insurance helps you take control of costs and make smarter decisions before committing to a loan.

Table of Contents

- Definition And Myths Of Lenders Mortgage Insurance

- Types Of Lenders Mortgage Insurance In Australia

- When And How Lenders Mortgage Insurance Applies

- Financial Impacts And Obligations For Borrowers

- Risks, Legal Responsibilities, And Alternatives

Key Takeaways

| Point | Details |

|---|---|

| Lenders Mortgage Insurance Protects Lenders | LMI is a financial protection mechanism primarily for lenders, not borrowers, leaving borrowers exposed to debt responsibilities. |

| Costs and Responsibilities | Borrowers are liable for LMI premiums, which increase overall loan costs and do not provide personal financial protection. |

| Myths and Realities | Common misconceptions about LMI can lead to misunderstandings about borrower responsibilities and the insurance’s actual coverage. |

| Alternative Options Exist | Government-backed schemes and family guarantor loans offer viable alternatives to LMI, potentially reducing upfront costs for first home buyers. |

Definition and myths of lenders mortgage insurance

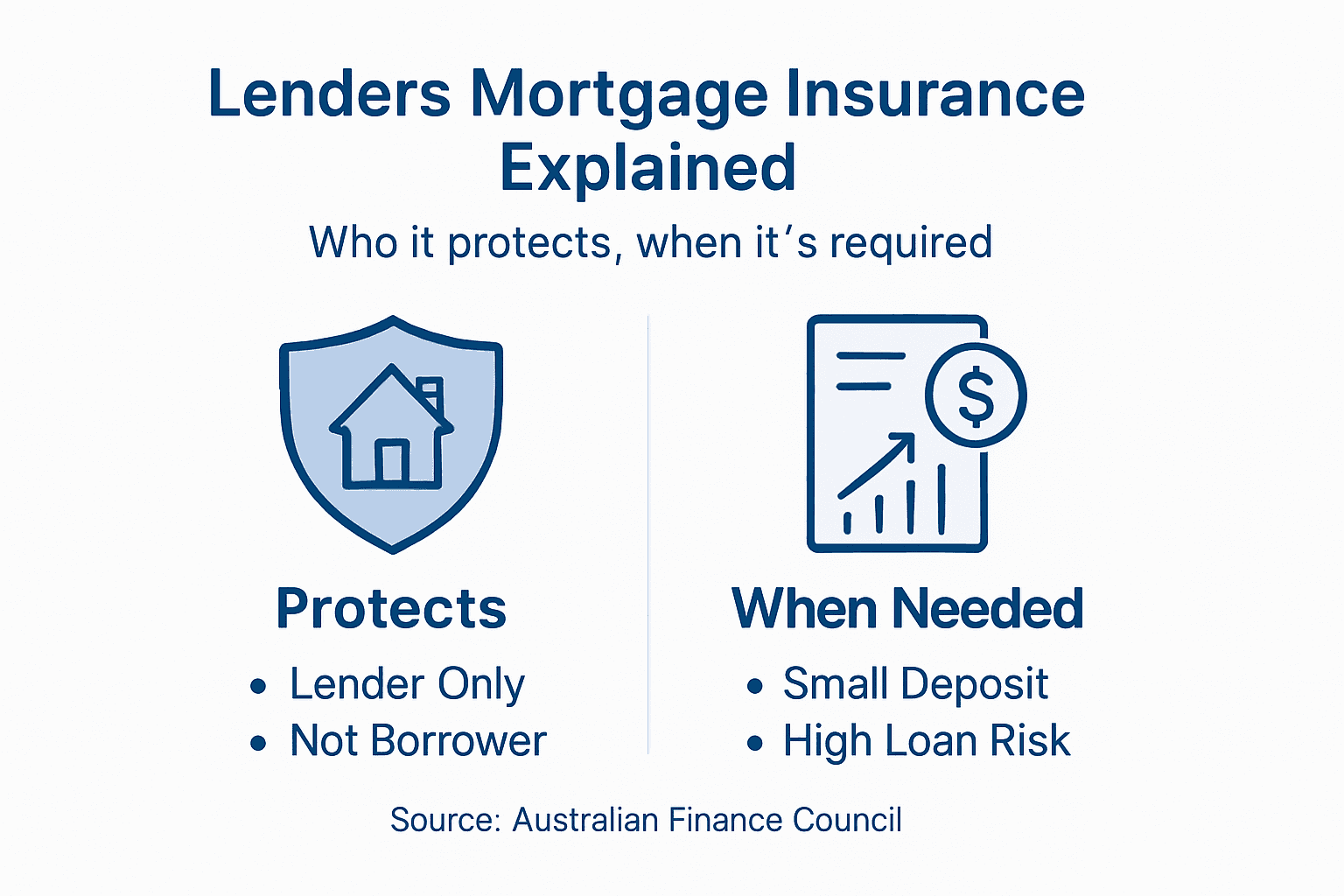

Lenders Mortgage Insurance (LMI) represents a complex financial protection mechanism that often confuses Australian property buyers. Detailed insurance guidelines reveal it’s a protection strategy exclusively designed for lenders, not borrowers.

At its core, LMI is a risk management tool enabling financial institutions to extend loans to borrowers with smaller deposits. When a borrower cannot provide a 20% deposit, lenders require this insurance to mitigate potential financial losses. Key characteristics include:

- Protects the lender, not the borrower

- Activated when borrowing more than 80% of property value

- Costs vary based on loan size and assessed risk

- Does not eliminate borrower liability for remaining debt

Common myths surrounding LMI can significantly impact a buyer’s understanding and financial strategy. Consumer protection principles highlight several misconceptions that borrowers must understand. Contrary to popular belief, LMI does not shield borrowers from debt responsibilities if a property sells for less than the outstanding mortgage.

Here’s how common LMI myths compare to the actual facts:

| Myth | Reality | Impact on Borrower |

|---|---|---|

| LMI protects the borrower | Only protects the lender | Borrower remains liable for debt |

| LMI removes all risk | Borrower still at risk of shortfall | Financial hardship not covered |

| LMI is optional with a small deposit | Required for deposits under 20% | Extra costs apply on small deposits |

The insurance premium is typically paid by the borrower but benefits the lender exclusively. This means that while you’re covering the cost, the protection is entirely directed towards the financial institution’s potential losses. Understanding these nuanced details helps buyers make more informed decisions about property acquisition and financial planning.

Pro tip: Always calculate the total cost of LMI and factor it into your property purchase budget to avoid unexpected financial strain.

Types of lenders mortgage insurance in Australia

Lenders Mortgage Insurance (LMI) in Australia encompasses multiple variations tailored to different property purchasing scenarios. Australian government deposit schemes offer unique alternatives that modify traditional LMI approaches, providing innovative solutions for borrowers.

The primary types of LMI in the Australian market include:

-

Owner-Occupied Property LMI

- Applies to homes where borrowers will live

- Typically lower risk profile

- Premiums based on loan-to-value ratio

-

Investment Property LMI

- Higher risk assessment

- More expensive premium structures

- Stricter qualifying criteria

-

Low Deposit LMI

- Designed for borrowers with less than 20% deposit

- Higher insurance costs reflecting increased lender risk

- Often includes additional assessment requirements

Government-Backed Alternatives represent an emerging category in mortgage protection. These schemes provide guarantees that effectively function like LMI but with different risk management approaches. They enable first home buyers to access property markets with reduced upfront insurance costs.

The complexity of LMI types reflects the nuanced risk management strategies employed by Australian financial institutions. Each variation addresses specific lending scenarios, considering factors like borrower profile, property type, and potential financial vulnerabilities.

Pro tip: Always compare multiple LMI providers and understand the specific terms of each insurance type before finalising your property purchase.

When and how lenders mortgage insurance applies

Lenders Mortgage Insurance (LMI) is triggered by specific borrowing conditions that increase potential financial risk for lending institutions. Detailed lending guidelines outline the precise circumstances where LMI becomes a mandatory requirement for property transactions.

The primary scenarios where LMI applies include:

-

Deposit Less Than 20%

- Automatic LMI requirement

- Increases lender’s risk exposure

- Premium calculated based on loan amount

-

High Loan-to-Value Ratio

- Triggered when borrowing exceeds 80% of property value

- Proportional risk assessment

- Additional financial protection for lenders

-

First Home Buyer Scenarios

- Often required with minimal deposit

- Higher scrutiny of borrower financial history

- Potential for government-backed alternatives

The application of LMI involves a comprehensive assessment process. Lenders evaluate multiple factors including borrower creditworthiness, employment stability, and overall financial profile. This meticulous approach ensures that the insurance mechanism provides appropriate protection while enabling broader access to property financing.

Understanding the nuanced application of LMI helps borrowers strategically plan their property acquisition. The insurance serves as a critical risk management tool, balancing the interests of both lenders and potential homeowners by facilitating loans that might otherwise be considered too risky.

Pro tip: Calculate your potential LMI costs early in your property purchasing journey to avoid unexpected financial surprises.

Financial impacts and obligations for borrowers

Lenders Mortgage Insurance brings significant financial implications that every borrower must carefully understand. Lending guidelines outline the complex financial obligations borrowers assume when LMI is involved.

The key financial impacts on borrowers include:

-

Premium Costs

- Added directly to loan amount

- Can range from thousands to tens of thousands

- Increases overall borrowing expenses

-

Ongoing Financial Responsibilities

- Full liability for entire mortgage debt

- Responsible for any shortfall after property sale

- No protection against financial hardship

-

Potential Long-Term Consequences

- Increased total loan amount

- Higher interest payments

- Extended loan repayment period

Borrowers must recognise that LMI does not provide personal protection. Despite paying the premium, individuals remain entirely responsible for mortgage repayments and potential financial shortfalls. The insurance solely protects the lending institution, transferring no direct benefit to the borrower beyond enabling loan approval with a smaller deposit.

Strategic financial planning becomes crucial when navigating LMI requirements. Borrowers should meticulously calculate total loan costs, including insurance premiums, and assess their long-term financial capacity to manage these additional expenses.

Pro tip: Request a detailed LMI cost breakdown before finalising your loan to understand the exact financial impact on your mortgage.

Risks, legal responsibilities, and alternatives

Lenders Mortgage Insurance involves complex legal and financial risks that borrowers must carefully navigate. Government support schemes offer alternative pathways for managing these potential challenges.

The primary risks and legal responsibilities include:

-

Personal Financial Liability

- Responsible for entire mortgage debt

- Potential legal action for loan shortfall

- No protection against financial hardship

-

Legal Debt Recovery Mechanisms

- Lenders can pursue full debt recovery

- Court-enforced repayment possibilities

- Credit rating implications for default

-

Long-Term Financial Consequences

- Potential asset seizure

- Extended legal obligations

- Negative impact on future borrowing capacity

Alternative strategies can help mitigate these risks. Government-backed schemes provide innovative solutions for first home buyers, offering guarantees that reduce or eliminate traditional Lenders Mortgage Insurance requirements. These alternatives create more accessible pathways to property ownership while minimising financial exposure.

Below is a summary of LMI alternatives and their key features:

| Alternative | Who it Helps | Main Advantage | Limitation |

|---|---|---|---|

| Government guarantee schemes | First home buyers | Entry with low deposit | Strict eligibility criteria |

| Family guarantor loans | Buyers with family support | Avoids LMI premium | Risks to guarantor’s property |

| Saving a larger deposit | Any buyer | No LMI needed | May delay property purchase |

Careful consideration of legal responsibilities and risk management strategies becomes crucial. Borrowers must thoroughly understand their obligations, potential liabilities, and available alternatives before committing to a mortgage with LMI requirements.

Pro tip: Consult a financial advisor to fully understand your legal obligations and explore alternative financing options before finalising your home loan.

Unlock Your Property Buying Power Despite Lenders Mortgage Insurance Challenges

Understanding how Lenders Mortgage Insurance protects lenders not borrowers can feel overwhelming when you have less than 20 percent deposit and face extra premiums on top of your loan. This article highlights the real financial impacts, legal responsibilities, and the myths surrounding LMI that may limit your property goals. If you want to maximise your buying power while managing these costs and risks confidently Elite Wealth Creators offers strategic solutions that go beyond traditional pathways.

With services like Instant Liquidity you can unlock up to $100,000 in cash from your existing investment properties giving you more flexibility to cover costs including LMI premiums. Our Homepay Advantage keeps your cash flow stable by deferring interest payments so you have control over your budget throughout your property purchase journey. This tailored approach combined with Precision Sourcing ensures you access off-market opportunities aligned with your long-term wealth strategy.

Don’t let Lenders Mortgage Insurance limit your path to financial freedom. Start now by exploring how to strengthen your property buying strategy at Elite Wealth Creators. Discover personalised advice and exclusive advantages designed to help you overcome LMI hurdles and build the future you deserve.

Frequently Asked Questions

What is Lenders Mortgage Insurance (LMI) and who does it protect?

Lenders Mortgage Insurance (LMI) is a risk management tool that protects lenders against potential financial losses when a borrower cannot provide a 20% deposit. It is important to note that LMI protects the lender, not the borrower.

When is Lenders Mortgage Insurance required during the home buying process?

LMI is typically required when a borrower has a deposit of less than 20% of the property’s value, which indicates a high loan-to-value ratio. It comes into effect to minimize the lender’s risk exposure.

What are the financial implications of paying for Lenders Mortgage Insurance?

Borrowers must pay the LMI premium, which can add significant costs to their overall loan amount. They will remain liable for the entire mortgage debt and any potential shortfalls if the property sells for less than the outstanding mortgage.

Are there any alternatives to Lenders Mortgage Insurance for homebuyers?

Yes, alternatives include government-backed schemes that offer guarantees to first home buyers, family guarantor loans, and saving for a larger deposit. These options can help mitigate the need for LMI while improving access to property ownership.

Recommended

- Pay Off Your Mortgage Faster | Elite Wealth Creators

- Mortgage Broker Role – Optimising Property Investment | Elite Wealth Creators

- NDIS Property Investment Guide | Elite Wealth Creators

- Home Loans & Equity for Investors | Elite Wealth

- Immobilienmakler Vorderer Odenwald | Haus verkaufen mit Lauria Immobilien

- Master the Solar Financing Process for Homeowners