TL;DR:

- Refinancing can improve your financial position when the expected savings outweigh costs and you plan to stay long enough.

- Calculating your break-even point helps determine if refinancing aligns with your timeline and goals, avoiding unnecessary expenses.

Most Australian homeowners know refinancing can save money. Far fewer know exactly when it does, when it doesn’t, and what it actually costs to find out. This guide to mortgage refinancing cuts through the uncertainty with a clear, practical framework built for the Australian market. You’ll learn what refinancing a home loan really means, how to calculate whether it’s worth your time and money, and the exact steps to move from decision to settlement. No guesswork. No costly surprises halfway through the process.

Table of Contents

- Key takeaways

- Guide to mortgage refinancing: what it is and why it matters

- Is refinancing right for you?

- The mortgage refinance process, step by step

- Common pitfalls and mortgage refinancing tips

- My honest take on refinancing: what actually works

- How Elitewealthcreators can help you move with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Know your break-even point | Divide your closing costs by your monthly savings to find out how long before refinancing pays off. |

| Compare APR, not just rates | Two loans with the same interest rate can cost very different amounts once fees are included. |

| Time horizon matters | Refinancing rarely makes sense if you plan to sell or move within two to three years. |

| Rolling in fees costs more | Adding closing costs to your loan balance increases total interest paid and extends your break-even. |

| Shop at least three lenders | Multiple Loan Estimates give you negotiating power and a clearer picture of true market rates. |

Guide to mortgage refinancing: what it is and why it matters

Refinancing, or home loan refinancing as it’s commonly known in Australia, means replacing your existing mortgage with a new one. You go through a qualification process similar to your original loan, and you pay closing costs to complete the switch. The new loan pays out the old one, and you begin repaying under the new terms.

People refinance for several distinct reasons, and understanding yours shapes every decision that follows:

- Lower your interest rate. Securing a lower rate reduces your monthly repayment and the total interest paid over the life of the loan.

- Shorten your loan term. Moving from a 30-year to a 15-year loan costs more each month but saves significantly in total interest.

- Access equity via cash-out refinance. You borrow more than your remaining balance and receive the difference in cash, which can fund renovations, investments, or debt consolidation.

- Switch loan type. Some borrowers move from a variable rate to a fixed rate for payment certainty, or vice versa depending on rate forecasts.

- Consolidate debt. Rolling higher-interest debt into a lower-rate home loan can improve monthly cash flow, though it extends the repayment period.

The three main refinance structures you’ll encounter in Australia are rate-and-term, cash-out, and no-closing-cost refinancing. The no-closing-cost option sounds appealing but typically means either a higher interest rate or fees rolled into the loan balance. Neither is free. You pay either way. The question is when and how.

Closing costs are the biggest surprise for first-time refinancers. Expect to pay 2% to 6% of the new loan amount in fees, which translates to $6,000 to $18,000 on a $300,000 loan. Understanding this upfront changes how you evaluate whether any particular refinance offer is genuinely worthwhile.

Is refinancing right for you?

This is where most homeowners stall. The right answer isn’t about the rate alone. It comes down to your numbers, your timeline, and your financial goals.

Start by gathering your current loan information: remaining balance, interest rate, monthly repayment, and how many years remain. Then get a realistic estimate of your home’s current value to understand your equity position. Your credit score matters too, as a stronger score unlocks better rates.

Next, calculate your break-even point. The formula is straightforward:

- Get your closing cost estimate. Most lenders will provide a ballpark figure early in the conversation, typically 2% to 6% of the new loan amount.

- Calculate your monthly savings. Subtract the new projected repayment from your current repayment.

- Divide costs by monthly savings. The result is the number of months until refinancing pays for itself.

- Compare that to your time horizon. If you plan to stay in the property beyond that break-even point, refinancing likely makes financial sense.

| Scenario | Closing costs | Monthly savings | Break-even period |

|---|---|---|---|

| $400K loan, 0.75% rate drop | $10,000 | $200 | 50 months (4.2 years) |

| $400K loan, 1.5% rate drop | $10,000 | $400 | 25 months (2.1 years) |

| $600K loan, 0.5% rate drop | $15,000 | $200 | 75 months (6.3 years) |

The break-even point is the most honest measure of whether refinancing serves you. Many homeowners focus exclusively on the monthly saving and ignore how long it takes to recoup the entry cost.

Pro Tip: If you’re rolling closing costs into the new loan rather than paying upfront, your monthly savings figure drops and your break-even extends further. Model both scenarios before committing to either.

One rule of thumb worth knowing: the industry often treats a 1% rate reduction as the threshold where refinancing becomes clearly worthwhile. In practice, smaller drops can still make sense depending on your costs and how long you plan to stay. The maths tells you, not the rule of thumb.

Don’t overlook what happens to your total interest if you extend your loan term. Refinancing a 20-year remaining loan back to 30 years might lower your monthly payment while substantially increasing what you pay in total. That trade-off is sometimes the right one, but you need to make it deliberately.

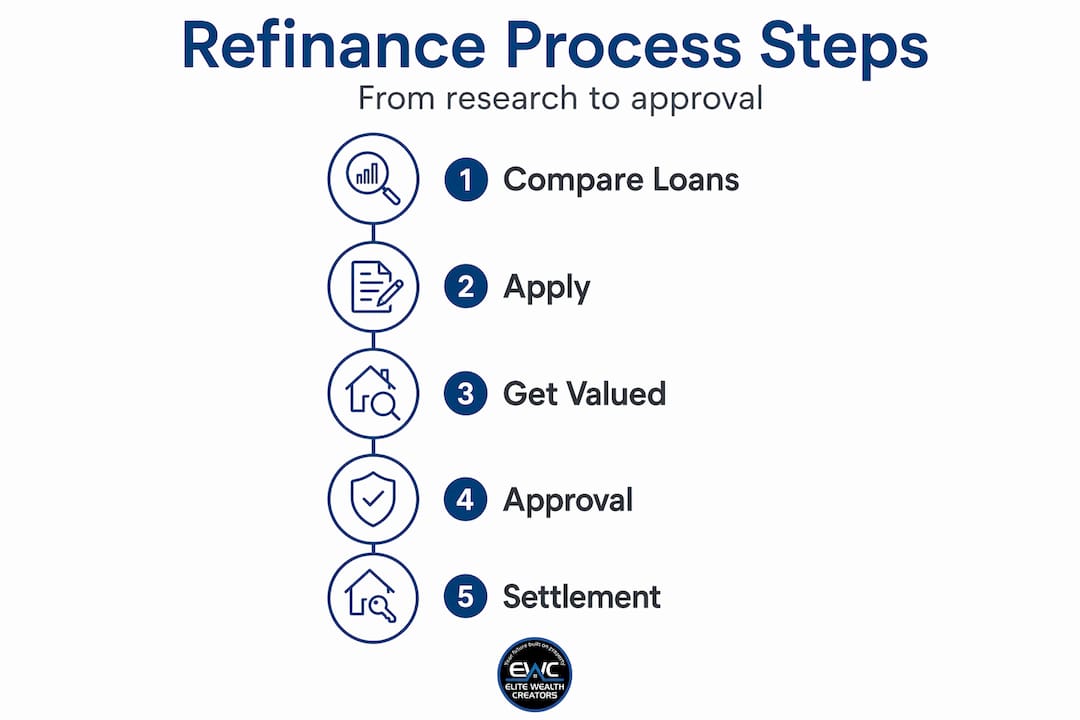

The mortgage refinance process, step by step

Knowing what to expect removes most of the anxiety from refinancing your home loan. Here’s how the process actually works:

- Set your goal. Before approaching any lender, decide what you’re trying to achieve. Lower repayments, shorter term, cash out, or rate certainty. Your goal determines which loan type suits you and how to evaluate offers.

- Check your credit and equity. Review your credit file for errors and understand your loan-to-value ratio. Most lenders want at least 20% equity for the best rates. Below that, you may face lenders mortgage insurance again.

- Gather your documents. You’ll need recent payslips, tax returns, bank statements, your current loan statement, and identification. Self-employed borrowers should prepare two years of tax returns and business financials.

- Shop at least three lenders. Contact banks, credit unions, and a mortgage broker. Each application will generate a Loan Estimate, which lenders must provide within three business days of your application.

- Compare Loan Estimates carefully. Don’t compare interest rates in isolation. Look at the APR, total closing costs, and the breakdown of fee sections. Sections A through C of a Loan Estimate cover origination charges and services, some of which are negotiable.

- Negotiate. Once you have multiple estimates, use them as leverage. A lender who wants your business will often match or beat a competitor’s fee structure.

- Lock your rate. Once you’ve chosen a lender, lock in your rate to protect against market movements during settlement.

- Prepare for the appraisal. Most refinances require a property valuation. Some streamlined programmes, such as government-backed options, may waive this requirement for eligible borrowers.

- Close and settle. Review all final documents carefully before signing. Confirm the figures match your Loan Estimate. After settlement, set up your new repayment schedule and cancel the old one.

| Step | What to focus on |

|---|---|

| Loan Estimate comparison | APR, total fees, and negotiable origination charges |

| Rate lock | Timing relative to settlement to avoid expiry |

| Appraisal | Comparable sales in your area that support your home’s value |

| Closing disclosure | Line-by-line match with original Loan Estimate |

Pro Tip: A mortgage broker can approach multiple lenders simultaneously, saving you time and often securing rates you wouldn’t find by approaching banks directly. Their fee is typically paid by the lender, not you.

Common pitfalls and mortgage refinancing tips

Even a well-structured refinance can work against you if you fall into predictable traps. Here’s what to watch for:

- Refinancing too soon. Many lenders impose a “seasoning period,” meaning you must hold a loan for a minimum period before refinancing. Check your current loan terms before assuming you can switch immediately.

- Chasing a teaser rate. Some lenders advertise very low introductory rates that revert to higher rates after one or two years. Always check the revert rate and the comparison rate, not just the headline figure.

- Ignoring total interest. A lower monthly repayment from an extended term can cost tens of thousands more in total interest. Run the full numbers, not just the monthly figure.

- Applying with multiple lenders carelessly. Each hard credit enquiry can slightly lower your credit score. Work with a broker or space out applications to minimise the impact.

- Accepting no-closing-cost at face value. As noted above, rolling fees into the loan increases your loan balance and the interest you pay over time. It’s a genuine trade-off, not a freebie.

Refinancing is not about getting the lowest rate on the market. It’s about improving your overall financial position in a way that aligns with your timeline and your goals. The two are very different things.

If you’re within two years of paying off your loan, refinancing rarely makes sense. The closing costs will likely exceed the interest savings you’d achieve in that remaining period. Likewise, if you’re planning to sell within 18 months, you probably won’t reach break-even before settlement.

Maintaining your credit score during the refinance process is straightforward: avoid opening new credit accounts, keep existing credit utilisation low, and don’t make large purchases on credit before settlement. Lenders will often run a final credit check just before closing.

My honest take on refinancing: what actually works

I’ve seen homeowners make the same mistake repeatedly. They call a lender, hear a rate that sounds good, and sign. No break-even calculation. No comparison of Loan Estimates. No clarity on whether staying in the property long enough to justify the cost.

In my experience, refinancing improves your financial position when you treat it as a strategic decision, not a reactive one. The borrowers I’ve seen benefit most are those who knew their break-even before they even contacted a lender. They walked into every conversation with a clear number in mind and the discipline to walk away if the offer didn’t meet it.

What surprises most people is how much variation exists between lenders on fees, not just rates. Two lenders might quote identical interest rates and differ by thousands in origination charges. That difference is often negotiable, but only if you’ve done the comparison work to know it exists.

My honest advice: don’t let the complexity of the process stop you from acting when the numbers are right. Get three Loan Estimates, run the break-even calculation, and be clear on how long you’re staying in the property. Those three steps cut through most of the confusion. Everything else is paperwork.

— Nick

How Elitewealthcreators can help you move with confidence

Refinancing is one decision in a larger wealth-building picture. At Elitewealthcreators, we work with Australian homeowners and investors to make sure each financial move, including refinancing, fits within a broader strategy that builds long-term value.

If you’re unsure whether refinancing is the right step right now, or you want to understand how your home equity could be working harder, our team can model the numbers with you and show you what’s actually possible. We take on a limited number of new clients each month because quality advice requires genuine attention. Spots are not unlimited.

Explore our property investment insights to see how refinancing fits within a growth-focused portfolio strategy, or visit our mortgage reduction resource to run your own break-even numbers and plan your next move. Ready to stop watching and start acting? We’re here.

FAQ

What does refinancing a home loan mean?

Refinancing replaces your current mortgage with a new loan, usually to secure a better rate, change the loan term, or access equity. You go through a similar qualification process to your original loan and pay closing costs to complete the switch.

How do I know if refinancing is worth it?

Calculate your break-even point by dividing your estimated closing costs by your projected monthly savings. If you plan to stay in the property beyond that period, refinancing is likely worthwhile financially.

How much do refinancing closing costs typically run?

Closing costs generally fall between 2% and 6% of the new loan amount. On a $400,000 loan, that’s $8,000 to $24,000, which is why calculating your break-even before committing is so important.

Does refinancing hurt my credit score?

Each lender application triggers a hard credit enquiry, which can slightly reduce your score. Working with a mortgage broker or consolidating applications within a short window minimises the impact on your credit profile.

When does refinancing not make financial sense?

Refinancing rarely makes sense if you’re close to paying off your loan, planning to sell within 18 months, or if the closing costs exceed the total interest savings you’d achieve within your planned ownership period.

Recommended

- Top Australian Mortgage Options in 2023 for Smart Borrowing | Elite Wealth Creators

- Why refinance your home: a guide for Australians 2026 | Elite Wealth Creators

- What is property refinancing: a smart guide for Australian homeowners 2026 | Elite Wealth Creators

- Smart Refinancing Tips to Build Wealth & Protect Your Home | Elite Wealth Creators