TL;DR:

- Your credit score significantly impacts mortgage approval, rates, and borrowing costs in Australia.

- Improving your score by paying bills on time and reducing credit utilization can save you thousands.

- Maintaining a strong credit profile provides leverage for better loan terms and wealth-building opportunities.

Your credit score is one of the most powerful numbers in your financial life, yet most Australians give it little thought until they’re sitting across from a lender. A score that’s even 50 points below a key threshold can mean the difference between securing your dream home at a competitive rate and being turned away entirely. Worse, a lower score doesn’t just affect approval; it can quietly add tens of thousands of dollars to your total loan cost over time. This guide breaks down exactly how credit scores work in Australia, how lenders use them, and what you can do to put yourself in the strongest possible position before you apply.

Table of Contents

- Understanding credit scores in Australia

- How lenders use credit scores in mortgage decisions

- The impact of your credit score on mortgage rates and terms

- Common credit score pitfalls and how to avoid them

- How to improve your credit score before applying for a mortgage

- Our perspective: Why credit scores matter even more than you think

- Turn a better credit score into wealth-building property moves

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Scores drive mortgage offers | A good credit score means easier mortgage approval and better loan deals for Australian homebuyers. |

| Better scores, better rates | Raising your credit score can unlock lower interest rates and big savings over the life of your loan. |

| Avoid credit mistakes | Careful management and awareness of your credit profile prevent costly missteps when applying for a mortgage. |

| Act early for best results | Improving your score well before application gives you more loan options and better financial flexibility. |

Understanding credit scores in Australia

A credit score is a three-digit number that summarises your history of managing debt and financial obligations. In Australia, scores range from 0 to 1,200, with a higher number indicating a lower risk to lenders. Three main credit reporting agencies operate here: Equifax, Experian, and illion. Each uses its own scoring model, so your score may differ slightly depending on which agency a lender queries.

Your credit history, which feeds into that score, is built from several key data points:

- Repayment history: Whether you pay bills and loans on time

- Credit enquiries: Every time you apply for credit, a record is created

- Defaults and court judgements: Serious negative events that stay on your file for up to five years

- Credit accounts: The types, ages, and balances of your existing accounts

- Bankruptcy or insolvency: Recorded for up to five years after discharge

Lenders rely on these scores because they offer a fast, standardised way to assess risk. When you’re securing a home loan, a lender needs confidence that you’ll meet repayments over a 25 to 30-year term. Your score provides that initial signal. Research suggests a significant portion of Australians are unaware of how their credit behaviour shapes their borrowing options, which means many buyers walk into loan applications unprepared.

Key takeaway: Your credit score is not just a formality. It is a live financial report card that directly influences whether you get a loan and on what terms.

How lenders use credit scores in mortgage decisions

Now that you know what a credit score is, let’s see how banks and lenders use it to shape your borrowing options.

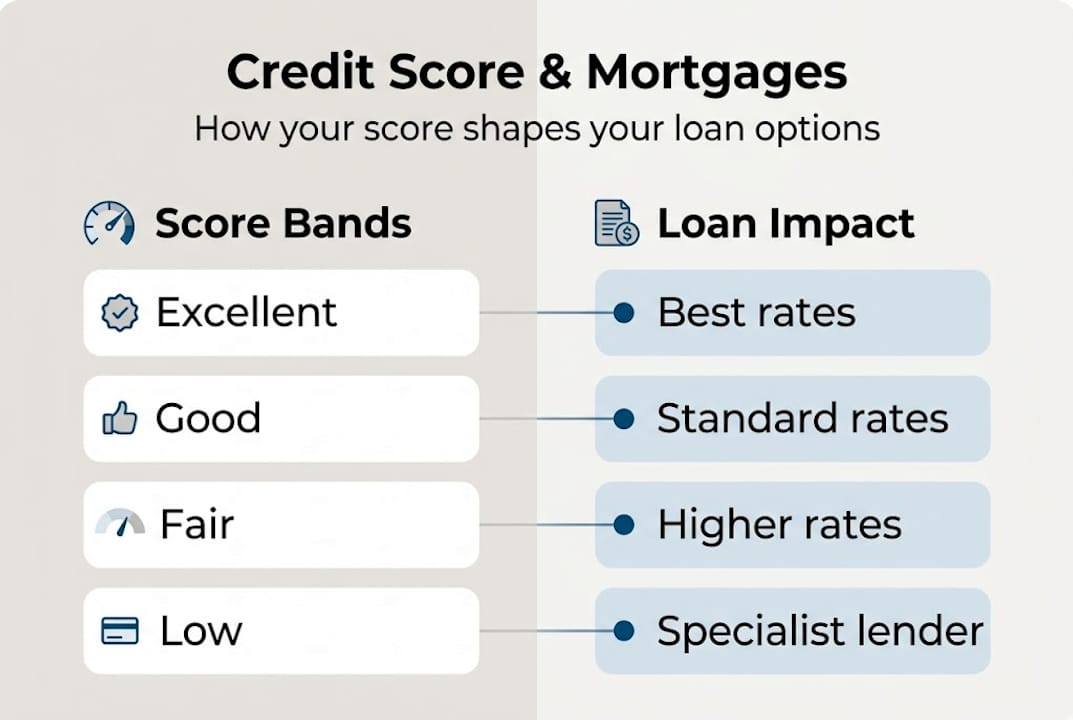

Lenders treat your credit score as a risk indicator. A high score signals responsible financial behaviour; a low score raises red flags about your ability to service a loan. Most lenders place applicants into lending tiers based on their score, and each tier comes with different products, rates, and conditions.

According to mortgage eligibility criteria, standard home loan products from major banks typically require a minimum score in the range of 620 to 700. Below that, you may still access finance, but through near-prime or specialist lenders at significantly higher rates.

| Credit band | Score range | Typical loan product | Rate premium |

|---|---|---|---|

| Excellent | 833 to 1,200 | Prime, best available rates | None |

| Very good | 726 to 832 | Prime, competitive rates | Minimal |

| Good | 622 to 725 | Standard products | Moderate |

| Fair | 510 to 621 | Near-prime products | Higher |

| Low | Below 510 | Specialist lenders only | Significant |

Beyond the score itself, lenders also weigh your income stability, deposit size, property type, and existing liabilities. Understanding credit score thresholds for home loans is important, but your score works alongside these other factors, not in isolation. A strong score with a small deposit may still face hurdles, while a moderate score paired with a 20% deposit can sometimes tip the balance in your favour.

Familiarise yourself with the mortgage approval steps early so you understand where your score fits within the broader assessment process.

The impact of your credit score on mortgage rates and terms

Beyond loan approval, your credit score also hits your back pocket by impacting the rate and terms you’re offered.

Even a 0.5% difference in your interest rate can translate into a substantial sum over the life of a loan. Consider a $600,000 mortgage over 30 years: at 6.0% interest, your total repayments are approximately $1.03 million. At 6.5%, that figure climbs to around $1.09 million. That’s roughly $60,000 extra, simply because your score placed you in a different lending tier. Credit score and loan rates data confirms this pattern across Australian lenders.

| Credit band | Indicative rate range | Estimated total cost ($600k, 30yr) |

|---|---|---|

| Excellent | 5.80% to 6.10% | $1.01M to $1.03M |

| Good | 6.20% to 6.60% | $1.05M to $1.09M |

| Fair | 6.80% to 7.50% | $1.12M to $1.22M |

| Low | 8.00%+ | $1.32M+ |

Your score also affects your required loan-to-value ratio (LVR). Borrowers with lower scores are often required to contribute a larger deposit, sometimes 20% or more, to offset the lender’s perceived risk. A strong score, by contrast, may allow you to borrow with a 10% deposit and avoid lenders mortgage insurance (LMI).

Pro Tip: Improving your score by even 50 points before applying could move you into a better lending tier. Start working on steps to prepare for a loan at least six months in advance, and the savings can be significant. If you already have a loan, a better score can also support refinancing strategies focused on paying off your mortgage faster.

Common credit score pitfalls and how to avoid them

To make sure your credit score helps, not hinders you, let’s look at the mistakes to avoid before your next property move.

Many Australians unknowingly damage their credit profiles through everyday habits. Understanding common credit score mistakes is the first step to protecting your borrowing power.

- Missing bill payments: Even a single missed payment can lower your score. Set up direct debits for utilities, phone plans, and credit cards.

- Making multiple credit applications: Each application creates an enquiry on your file. Several enquiries in a short period signal financial stress to lenders.

- High credit card utilisation: Using more than 30% of your available credit limit regularly can reduce your score, even if you pay the balance each month.

- Closing old credit accounts: Length of credit history matters. Closing an old card removes positive history from your file.

- Ignoring errors on your credit report: Incorrect defaults or outdated information can drag your score down unfairly. Check your report and dispute any inaccuracies.

- Co-signing loans carelessly: If the primary borrower defaults, it affects your score too.

Repairing credit damage takes time but is achievable. Pay down outstanding debt, correct any errors with the relevant reporting agency, and avoid new credit applications for at least three to six months before you plan to apply. Use the home loan checklist to track your preparation, and if you’re a first-time buyer, the checklist for first home buyers is a practical starting point.

Pro Tip: Check your credit report six months before applying for a mortgage. That gives you enough time to correct errors and address any issues before a lender sees your file.

How to improve your credit score before applying for a mortgage

Now that you know what drags your score down, here’s how to actively build it up for a stronger mortgage application.

Improving your score is not complicated, but it does require consistency. Effective strategies include the following practical steps:

- Pay every bill on time: This is the single most impactful habit you can build. Even small bills count.

- Reduce your credit card balances: Aim to keep utilisation below 30% of your total available limit across all cards.

- Correct errors on your credit file: Request a free copy of your report from Equifax, Experian, or illion and dispute anything inaccurate.

- Limit new credit applications: Each hard enquiry stays on your file for up to five years. Apply only when necessary.

- Keep older accounts open: A longer credit history works in your favour, so resist the urge to close accounts you no longer use regularly.

- Consolidate debt strategically: Reducing the number of active debts can simplify your profile and lower your overall utilisation.

Changes to your credit behaviour typically take one to three months to reflect in your score, though more significant improvements may take six months or longer. The payoff is real: a stronger score raises your borrowing power and opens access to better loan products. Explore the steps to boost borrowing power for a detailed action plan, and if you’re entering the market for the first time, our first home buyer guidance provides tailored support for your situation.

Our perspective: Why credit scores matter even more than you think

Most buyers treat a credit score as a simple pass or fail test. Either you qualify or you don’t. But that framing misses the real strategic opportunity.

Today’s lenders use sophisticated, tiered risk assessment models. A strong credit profile doesn’t just get you approved; it gives you leverage. Borrowers with excellent scores can negotiate offset accounts, interest-only periods for investment properties, and higher LVRs without LMI. These aren’t minor perks. They are the structural tools that allow investors to recycle capital, maintain cash flow, and scale a portfolio faster than someone locked into a standard principal-and-interest product.

We’ve seen clients use a deliberately managed credit profile as a vehicle for smart property investing, accessing deal structures that most buyers don’t even know exist. The buyers who treat credit management as an ongoing discipline, not a one-time fix before a loan application, are the ones who build lasting wealth. Your score is not just a gateway. It is an active part of your investment strategy.

Turn a better credit score into wealth-building property moves

Understanding your credit score is a strong foundation, but knowing how to act on that knowledge is where real outcomes are built. At Elite Wealth Creators, we work with homebuyers and investors to translate financial readiness into strategic property decisions. Whether you’re preparing for your first application or looking to invest smart for property wealth growth, our team provides the expert guidance to match your profile with the right opportunities. Explore our resources on unlocking financial freedom and take the next step with a team that understands what it takes to win in the Australian property market.

Frequently asked questions

What is the minimum credit score required for a mortgage in Australia?

Most banks prefer scores above 620 for prime products, but specialist lenders may accept lower scores in exchange for higher interest rates and stricter conditions.

How can I check my credit score for free in Australia?

You can access your free credit report through major Australian reporting agencies including Experian, illion, and Equifax, each of which is required by law to provide one free report per year.

Does applying for multiple home loans hurt my credit score?

Yes, multiple credit enquiries in a short period can reduce your score and signal financial instability to lenders, so it pays to research options before formally applying.

Can a strong credit score lower my mortgage repayments?

A higher score can qualify you for lower interest rates, which directly reduces both your monthly repayments and the total amount you pay over the life of the loan.

Recommended

- Step-by-Step Mortgage Approval: Boost Borrowing 30% in 2026 | Elite Wealth Creators

- Pay Off Your Mortgage Faster | Elite Wealth Creators

- Top Australian Mortgage Options in 2023 for Smart Borrowing | Elite Wealth Creators

- How to Secure a Home Loan for First-Time Buyers Easily | Elite Wealth Creators

- Credit Score for Apartment Rental: What You Need to Know – Luxury Apartments for Rent in Boca Raton | Premium Boca Raton Apartments | Aapartments Boca Raton