TL;DR:

- Property yield measures annual rental income as a percentage of a property’s value, but it is often misunderstood.

- While useful for initial comparisons, yield alone does not reflect profit, capital growth, or tax benefits essential for investment decisions.

Property yield is one of the most cited numbers in real estate, yet one of the most misunderstood. Ask ten investors what it means and you will likely get ten different answers. Many buyers fixate on yield as if it were a final verdict on whether a property is worth buying, when it is really just the starting point. Understanding what property yield is, how to calculate it correctly, and where it fits within a broader investment picture is the difference between confident, informed decisions and costly mistakes that compound over time.

Table of Contents

- Key takeaways

- What is property yield and why it matters

- How to calculate property yield

- The limits of yield as an investment metric

- Applying property yield to real investment decisions

- My take on property yield and investment decision-making

- How Elitewealthcreators helps you act on yield intelligence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Yield measures income potential | Property yield expresses annual rental income as a percentage of the property’s value or purchase price. |

| Gross yield is for shortlisting | Use gross yield to quickly compare properties or markets, not to make final investment decisions. |

| Net yield reveals true performance | Net yield accounts for expenses like management fees, insurance, and maintenance for a more accurate picture. |

| Yield is only part of the story | Capital growth, tax impacts, and financing costs are not captured by yield and must be assessed separately. |

| Vacancy buffers matter | Budget a vacancy allowance of 5 to 10% to avoid overestimating income and misreading your returns. |

What is property yield and why it matters

At its core, property yield is a percentage that tells you how much annual rental income a property generates relative to its value or purchase price. Think of it as a quick income efficiency score. If a property costs $500,000 and generates $25,000 in annual rent, the yield is 5%.

The property yield definition is straightforward, but its role in investment analysis is frequently misread. Yield is not profit. It does not tell you what you will walk away with after costs, tax, or loan repayments. What it does tell you is how much income the property produces as a proportion of its price, which is useful for comparing opportunities across different markets or property types.

Here is where many investors go wrong. They confuse yield with capital growth, or assume a high yield guarantees a strong investment. These are two completely separate forces. A property can deliver yield without growth and vice versa. The importance of property yield lies in what it measures precisely, not in what people assume it covers.

Understanding the real estate yield explained in its two core forms will sharpen how you assess any deal:

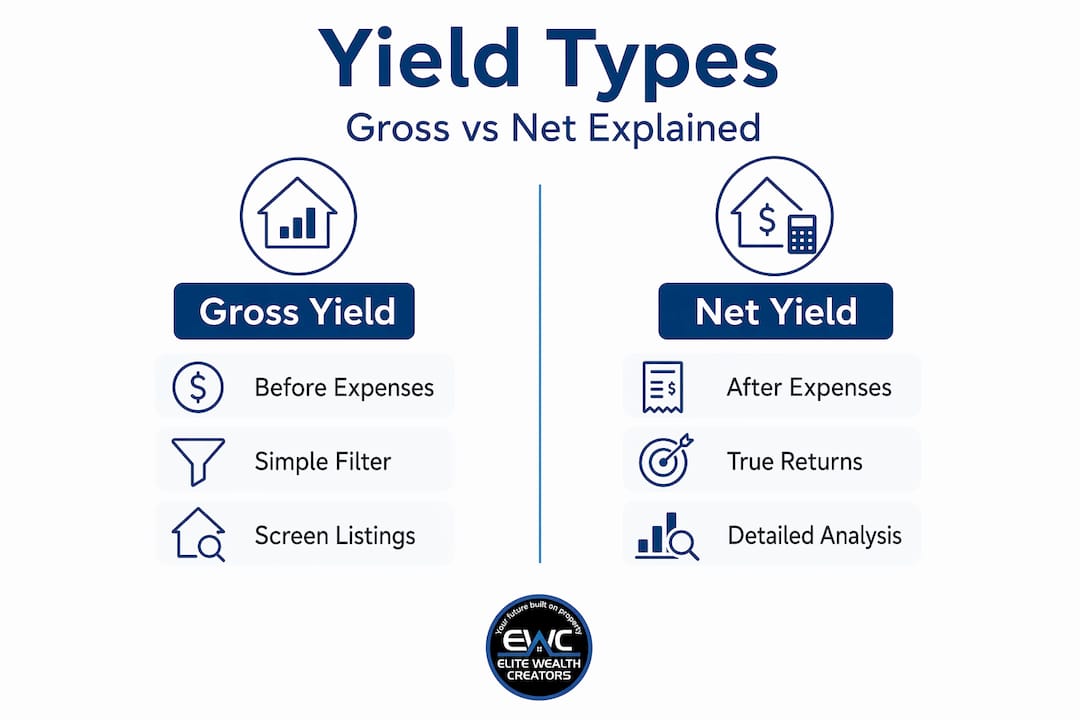

- Gross rental yield: The raw percentage of annual rent divided by the property’s purchase price or market value. Fast to calculate. Good for initial comparisons.

- Net rental yield: A more precise figure that subtracts ongoing landlord expenses from rental income before calculating the percentage. This is what you should be drilling into for any serious purchase.

- Capital growth: The increase in the property’s market value over time. Completely separate from yield. High yield suburbs do not always produce strong capital growth.

- Cash flow: What actually lands in your account after expenses and loan repayments. Yield informs this, but does not equal it.

- Vacancy impact: An often overlooked variable. Even a 2% vacancy rate can meaningfully drag your real yield below what the numbers suggest on paper.

The importance of property yield is real, but only when you understand exactly what it is measuring and what it is not.

How to calculate property yield

Knowing the property yield formula for each type of yield puts you in control of your own analysis. Do not outsource this thinking. Run the numbers yourself every time.

Gross yield

This is the starting point for any property yield analysis. The formula is simple:

(Annual Rental Income ÷ Property Value) × 100 = Gross Rental Yield %

If a property is valued at $600,000 and rents for $550 per week, the annual rental income is $28,600. Divide by $600,000, multiply by 100, and you get a gross yield of 4.77%. Use this to quickly screen properties. Nothing more.

Net yield

Net yield is where the real story begins. It accounts for the actual costs of holding and managing the property:

((Annual Rental Income − Annual Expenses) ÷ Property Value) × 100 = Net Rental Yield %

Typical expenses included in this calculation are:

- Property management fees (usually 7 to 10% of rent collected)

- Council rates and water charges

- Landlord insurance premiums

- Routine maintenance and repairs

- Accountancy and administrative costs

- Strata or body corporate fees if applicable

Using the same $600,000 property, assume annual expenses of $8,000. Net rental income becomes $20,600. Divide by $600,000 and multiply by 100 to get a net yield of 3.43%. That is a meaningful drop from the gross figure, and it paints a far more honest picture of what the property actually earns. Gross yield typically exceeds net yield by 2 to 3 percentage points once all costs are factored in.

Cash-on-cash return

Once financing enters the picture, you need a different metric. Cash-on-cash return is an investor-level calculation that accounts for how the property is funded:

Annual Pre-Tax Cash Flow ÷ Total Cash Invested × 100 = Cash-on-Cash Return %

Two investors buying the same property with different loan structures will arrive at completely different cash-on-cash returns. This is the metric that tells you how hard your actual dollars are working, not the property’s dollars.

Pro Tip: Always calculate net yield and cash-on-cash return before committing to any purchase. Gross yield gets you in the door, but these two numbers tell you whether the deal is genuinely worth walking through.

| Metric | What it measures | Includes financing? | Best used for |

|---|---|---|---|

| Gross rental yield | Raw income vs purchase price | No | Quick property screening |

| Net rental yield | Income after expenses vs value | No | Realistic income comparison |

| Cash-on-cash return | Cash flow vs cash invested | Yes | Evaluating financed deals |

Do not forget vacancy. Budget a 5 to 10% vacancy allowance when modelling any property’s income. Even a single month of vacancy per year reduces your effective yield and can tilt a borderline deal into negative territory.

The limits of yield as an investment metric

Property yield analysis is a powerful lens, but it is not a complete one. Treating it as the final word on a property’s merit is one of the most common and costly mistakes investors make.

Yield is a property-level income snapshot. It does not capture capital growth, tax benefits like depreciation deductions, or the impact of your loan structure. A property yielding 7% that never appreciates in value may deliver less total wealth over ten years than a 4% yield property in a suburb growing 8% per annum. Context is everything.

Here is what experienced investors weigh alongside yield:

- Market context: A gross yield above 6% is broadly considered strong in many Australian residential markets, but this benchmark shifts significantly by location, property type, and economic conditions. Regional properties often show higher yields than inner-city apartments, yet carry very different risk profiles.

- Liquidity risk: High-yield properties in thin markets can be difficult to sell quickly. If the tenant leaves and demand is soft, you may face both vacancy costs and a property that sits unsold longer than expected.

- Maintenance exposure: Older properties or those in lower socioeconomic areas sometimes produce attractive yields on paper. But elevated maintenance costs and higher tenant turnover can erode net yield faster than the gross figure suggests.

- Leverage impact: When your cap rate exceeds your cost of debt, leverage amplifies your returns. When debt costs more than the property earns, leverage destroys them. This dynamic is not visible in the yield number alone.

“Most investors wrongly use gross yield as a final metric. Experienced investors rely on net yield and cash-on-cash return to factor in costs and financing.” — How to calculate rental yield

Understanding what affects property yield also means recognising that comparable properties in the same street can produce dramatically different returns depending on renovation quality, lease terms, management quality, and the specific ownership structure in place. These variables live beneath the headline yield figure.

Explore types of property investments to understand how yield outcomes differ across residential, commercial, and SMSF-held assets. The variables that shape yield are not uniform across property types, and treating them as if they are will skew your analysis from the start.

Applying property yield to real investment decisions

Understanding property yield is worth nothing unless it changes how you act. Here is how to move from theory to decisive, grounded decisions.

Start with gross yield to filter quickly. There is no point spending hours on due diligence for a property that fails even the basic income screen. Set a minimum gross yield threshold for your target market and use it to cut your shortlist fast.

Once you have shortlisted candidates, drill into net yield. This is where you request rental appraisals, confirm actual council rates, get strata levy figures, and factor in realistic management costs. Use the net rental yield formula with real numbers, not estimates. Pair this with a rental income deductions review to understand what tax offsets apply to your expenses, as these directly influence your after-tax cash flow position.

Then model your cash-on-cash return. Factor in your actual loan structure early, not as an afterthought. Two properties with identical net yields can produce radically different investor-level returns depending on borrowing strategy. The investors who get this right are rarely the ones who know the most. They are the ones who act on clear numbers rather than waiting for perfect certainty.

Common pitfalls to avoid:

- Ignoring vacancy: Do not model 100% occupancy. Build in a 5 to 10% vacancy buffer in every calculation.

- Using asking rent, not market rent: Vendor-provided rent figures can be optimistic. Get an independent rental appraisal from a local property manager.

- Forgetting capital expenditure: Roofs, hot water systems, and appliances all have finite lifespans. Budget for these or your net yield will be far lower than you calculated.

- Skipping the financing conversation: Know your borrowing costs before you fall in love with a yield figure. The property yield formula tells you nothing about your loan repayments.

Pro Tip: Ask your property manager for a twelve-month rental ledger on any property you are seriously considering. It confirms the actual rent received, not the advertised amount, and reveals any payment gaps or vacancy periods the vendor may not volunteer.

My take on property yield and investment decision-making

I have worked with hundreds of investors across the Australian market, and the pattern I keep seeing is this: people become so focused on finding the “right” yield number that they stop moving altogether. They watch good properties sell while still debating whether 5.2% is better than 4.8%.

Gross yield is a screening tool. Nothing more. I use it to eliminate properties that clearly do not meet my income criteria, then I set it aside. The real analysis begins with net yield and cash-on-cash return, and even those numbers are inputs into a bigger picture that includes market trajectory, debt serviceability, and personal wealth goals.

The uncomfortable truth is that experienced investors rely on net yield and financing metrics, not gross yield headlines. I have seen investors chase 8% gross yields in regional markets, only to realise that management costs, vacancy, and capital stagnation made the actual return far weaker than a 4.5% yield property in a growing corridor.

Yield matters. But it is a starting point, not a destination. The investors I see build genuine wealth are the ones who understand the numbers clearly enough to act decisively, rather than waiting for a yield figure that feels perfect.

— Nick

How Elitewealthcreators helps you act on yield intelligence

Understanding property yield is one thing. Knowing which properties in the Australian market actually deliver on their yield promise is another challenge entirely. That is where Elitewealthcreators provides the edge that most buyers and investors simply do not have access to on their own.

Through property investing expertise, Elitewealthcreators goes beyond surface-level yield figures to model net returns, assess financing structures, and match each client to opportunities that align with their specific wealth goals. Whether you are building your first investment portfolio, optimising for cash flow, or structuring assets within an SMSF, the team delivers analysis that cuts through the noise.

SMSF trustees can also access dedicated SMSF property investment guidance to avoid compliance pitfalls while maximising allowable returns within the fund’s structure.

New client spots are limited each month. Not for exclusivity, but because genuine strategy takes time and attention. If you are ready to stop watching others build wealth and start acting on real numbers, now is the time to connect.

FAQ

What is the property yield definition in simple terms?

Property yield is the annual rental income of a property expressed as a percentage of its value or purchase price. It measures how much income a property generates relative to its cost.

What is the difference between gross and net property yield?

Gross yield is calculated before deducting any expenses. Net yield subtracts costs such as management fees, insurance, maintenance, and rates, giving a more accurate view of actual income performance.

How do I calculate property yield using the formula?

Divide the annual rental income by the property value, then multiply by 100. For net yield, subtract annual expenses from rental income first before dividing by the property value.

What is considered a good property yield in Australia?

A gross rental yield above 6% is broadly regarded as strong in many Australian residential markets, though this varies significantly by location, property type, and current market conditions.

Why is yield alone not enough to assess an investment property?

Yield only captures income relative to property value. It does not account for capital growth, tax impacts, vacancy rates, or the effect of your loan structure on actual investor returns.