TL;DR:

- Off-the-plan buying involves purchasing property before construction is finished, relying on plans and specifications.

- Benefits include stamp duty concessions, capital growth potential, depreciation advantages, and flexibility in finishes.

- Key risks are construction delays, valuation shortfalls, and developer insolvency, requiring thorough research and legal protections.

Purchasing a property you’ve never walked through might sound counterintuitive, yet thousands of Australians do exactly this every year through off-the-plan buying. This approach, where you commit to a purchase before a single brick is laid, has grown steadily across capital cities and regional growth corridors alike. Whether you’re a first-time buyer trying to enter the market or an investor building a high-yield portfolio, understanding this method of asset acquisition could meaningfully shape your financial future. This guide walks you through exactly what off-the-plan buying means, where the opportunities lie, and how to protect yourself at every stage.

Table of Contents

- What is off the plan buying?

- Benefits of off-the-plan buying for buyers and investors

- Risks and protections: What every buyer should know

- Essential steps for safe off-the-plan buying

- Why due diligence trumps hype: Our take on off-the-plan success

- Take the next step: Access smart property investing tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Off-the-plan meaning | Buying off the plan means purchasing a property before it’s built, using plans and developer information. |

| Key benefits | You can secure lower stamp duty, allow more time to save, and potentially benefit from capital gains during construction. |

| Main risks | Delays, valuation changes, and developer insolvency are real risks but legal protections exist. |

| Due diligence | Independent advice and thorough contract review dramatically reduce off-the-plan risks. |

What is off the plan buying?

Off-the-plan buying means committing to purchase a property before construction is complete or a legal title has been created. Instead of inspecting a finished home, you rely on architectural plans, developer specifications, and rendered images to make your decision. The property exists on paper and in promise, not yet in concrete and glass.

This approach is most common with apartments in high-rise developments, townhouses in master-planned estates, and land packages in new residential corridors. Developers favour this model because pre-sales allow them to secure financing from lenders before construction begins. Buyers gain access to properties at today’s prices, even though settlement won’t happen for 12 to 36 months.

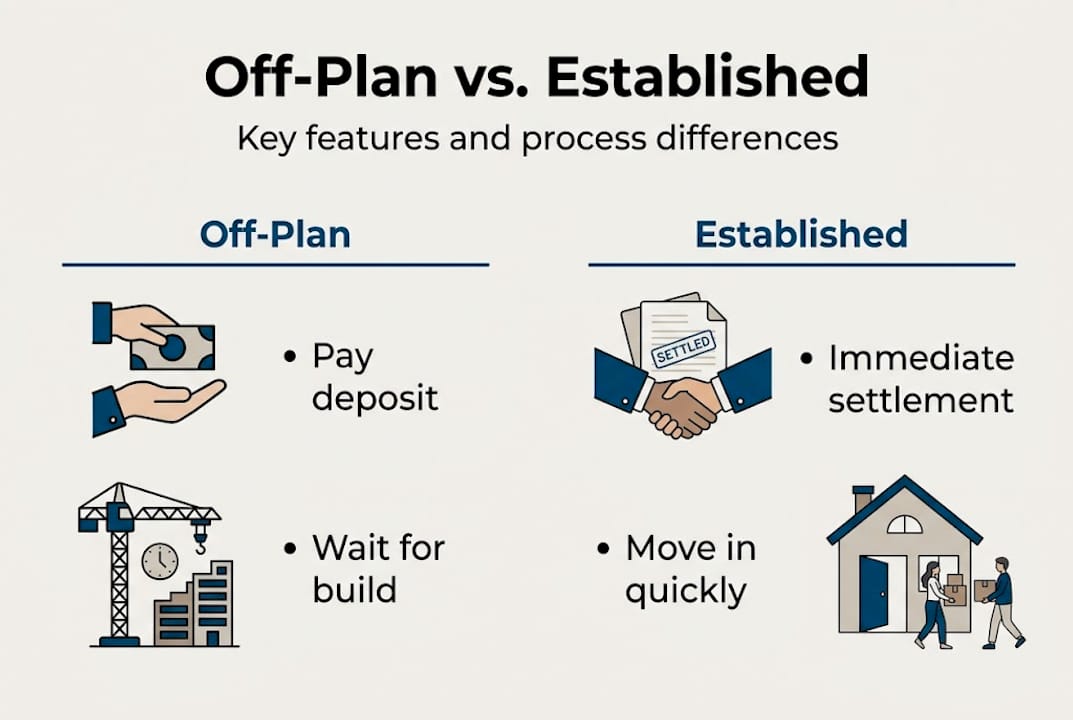

For context, here’s how off-the-plan buying typically compares to buying an established property:

| Feature | Off the plan | Established property |

|---|---|---|

| Purchase price locked | Yes, at signing | Yes, at signing |

| Property inspectable | No (plans only) | Yes |

| Settlement timeline | 12 to 36+ months | 30 to 90 days |

| Stamp duty concessions | Often available | Limited |

| Depreciation benefits | High (new assets) | Lower (older assets) |

| Customisation options | Sometimes | Rarely |

The legal and purchase process follows a clear sequence. You sign a contract of sale and pay a deposit, typically 10% of the purchase price, which is held in a trust account rather than handed to the developer. This is an important protection. The developer cannot access those funds until settlement occurs at construction completion.

Here’s a simplified overview of what the process looks like in practice:

- Research stage: You identify a development, review floor plans, and assess the location and developer track record.

- Contract review: A solicitor or conveyancer reviews the off-the-plan contract, which can be far more complex than a standard property contract.

- Deposit payment: Your deposit is lodged into a statutory trust account, protected until settlement.

- Construction period: You monitor progress and prepare your finances for final settlement.

- Settlement: The title is created, the balance of the purchase price is paid, and ownership transfers to you.

Understanding this sequence thoroughly is essential before you sign anything. Our step-by-step off-plan buying resource goes deeper on each stage. You should also review our property buying essentials guide if you’re approaching the market for the first time.

The popularity of off-the-plan buying among investors stems from its unique financial structure. You secure an asset with a relatively small upfront commitment, giving you time to organise finance while the property potentially grows in value during construction.

Benefits of off-the-plan buying for buyers and investors

Now that you’ve grasped what off-the-plan buying is, it’s worth examining why it consistently attracts both owner-occupiers and investors across Australia. The financial advantages are real, measurable, and in some cases, significant enough to reshape your wealth-building strategy.

1. Stamp duty concessions

Stamp duty is one of the largest upfront costs in any property purchase. Off-the-plan buyers in several states benefit from concessions that established property buyers simply cannot access. In Victoria, New South Wales, and South Australia, stamp duty on off-the-plan purchases is often calculated on the land value only, or on the contract price minus the construction component. The result? Savings of $20,000 to $40,000 on a $750,000 property are entirely realistic. For a first-home buyer, that sum can mean the difference between entering the market and waiting another two years.

2. Time to save your deposit

Because settlement occurs months or years after you sign the contract, you effectively have extra time to build your savings. Your 10% deposit is locked in at today’s price, but your remaining funds can continue growing in a high-interest savings account. This is particularly useful for buyers who are close to their goal but not quite there when a promising development launches.

3. Capital growth during the build

If the property market rises between the date you sign and the date you settle, you capture that growth. You’ve locked in the purchase price, so a property valued at $750,000 today that settles at $830,000 in two years means you’ve gained $80,000 in equity before you even receive the keys. This isn’t guaranteed, and markets can move in either direction, but it has historically been a compelling argument in high-demand urban corridors.

4. Depreciation benefits for investors

New properties attract substantially higher depreciation deductions than older ones. Investors purchasing off the plan can claim depreciation of $10,000 to $18,000 in the first year alone, depending on the property’s fixtures, fittings, and structural components. Over a five to ten-year holding period, these deductions can materially reduce your taxable income and improve net cash flow.

Pro Tip: Commission a quantity surveyor to prepare a depreciation schedule before your first tax return. This document captures every claimable asset, from carpet to air conditioning systems, and ensures you don’t leave legitimate deductions on the table.

5. Flexibility and customisation

Some developers allow buyers to select finishes, colour schemes, and layout options within a certain timeframe. This means you can influence the final product to suit your lifestyle or maximise rental appeal. Established properties rarely offer this flexibility without expensive renovations.

A well-chosen off-the-plan property, aligned with a sound property investment strategy, can serve as a reliable long-term wealth vehicle. For broader context on building your portfolio, our Australian property investment guide covers the fundamentals in detail.

Risks and protections: What every buyer should know

While the advantages are strong, buyers often overlook the risks and contract nuances in their excitement. Knowledge here is not optional. It’s the foundation of a sound decision.

Construction delays

This is the most commonly experienced risk. Builds run late for many reasons, including material shortages, labour disputes, council approvals, and weather. The impact on buyers can be severe. Consider cases where buyers have found themselves effectively homeless, having sold their existing home in anticipation of a settlement date that was then pushed back by 12 months or more. If you’re planning your living arrangements around a settlement date, always build in a significant contingency buffer.

Valuation shortfalls at settlement

Your bank will conduct a fresh valuation of the property at the time of settlement, not at the time you signed the contract. If the market has softened or the development has an oversupply problem, the bank may value the property below your contract price. This creates a shortfall you must cover from your own funds. For example, if you contracted to buy at $750,000 but the bank values it at $710,000, you need an additional $40,000 in cash at settlement. This is not a hypothetical scenario. It catches many buyers off guard.

Developer insolvency

Construction companies represent 26% of all Australian business insolvencies in 2024 to 2025, making this a very real concern. If your developer collapses mid-build, you could face a prolonged legal process to recover your deposit or find yourself in a partially completed development with uncertain ownership prospects.

“Your deposit is only as safe as the trust account it’s held in. Verify that your contract explicitly states the deposit is held in a statutory trust, not a general account, before you sign.”

Fortunately, protections exist. Here’s what Australian law currently provides:

- Trust account protection: Deposits must be held in trust until settlement, meaning the developer cannot access your funds during construction.

- QLD Land Sales Act safeguards: Queensland law mandates that settlement must occur within 18 months, or the buyer has the right to terminate and reclaim their deposit.

- 2023 sunset clause reforms: Recent legislative changes restrict developers from using sunset clauses to terminate contracts for their own benefit without the buyer’s consent or a court order.

Pro Tip: Always request a copy of the project’s development approval and finance confirmation before committing. A development without secured construction finance is a red flag worth taking seriously.

For a thorough walkthrough of how to navigate the buying process safely, our property buying guide is an excellent starting point.

Essential steps for safe off-the-plan buying

Armed with the risks and protections, the next step is turning theory into action. Here is a practical checklist to guide your approach.

1. Research the developer thoroughly

Before anything else, investigate who you’re buying from. How many projects have they completed? Do they have a history of delivering on time and on spec? Check publicly available records, speak to buyers in their previous developments, and search for any legal proceedings or complaints filed against the company. Given that rising construction insolvencies reached 2,832 in the most recent financial year, vetting your developer is not a formality. It’s a critical filter.

2. Engage a specialist solicitor before signing

An off-the-plan contract is not a standard property contract. It contains sunset clauses, sunset dates, sunset rights, substitution clauses, and variation provisions that can each carry significant consequences. Engage a solicitor who specialises specifically in off-the-plan purchases, not just a general conveyancer. The cost of expert legal review is a fraction of the cost of a contract dispute.

3. Review the contract for these key terms

- Sunset clause dates and who holds termination rights

- Permitted variations to the finished product

- Progress payment schedule and deposit bond options

- Defect liability periods and rectification obligations

- Body corporate levy estimates

4. Understand your finance position at settlement

Get a pre-approval from your lender that specifically acknowledges the off-the-plan timeline. Ask your mortgage broker what happens if valuations come in below the contract price. Stress-test your position against a 5% to 10% valuation shortfall and ensure you have access to additional funds if needed.

5. Consider a deposit bond instead of cash

Rather than tying up a large cash deposit for two or more years, a deposit bond acts as a guarantee to the developer while your cash continues working elsewhere. Not all developers accept them, but it’s worth asking.

Pro Tip: Ask the developer directly for the names and contact details of buyers in their most recently completed project, then call those buyers and ask candid questions about the experience.

6. Get independent financial advice

An accountant or financial adviser can model the investment returns, depreciation schedule, and tax implications specific to your situation. What works brilliantly for a high-income earner may not suit a buyer on a moderate salary.

For those looking to build a property portfolio through this approach, understanding the buy-to-let process in an Australian context will sharpen your strategy considerably.

Why due diligence trumps hype: Our take on off-the-plan success

Having worked across hundreds of off-the-plan transactions, we’ve noticed a consistent pattern. The buyers who achieve the best outcomes are rarely the fastest movers. They’re the most thorough ones.

The biggest mistake we see is emotional decision-making driven by glossy brochures, limited-time offers, and fear of missing out. Developers are skilled at creating urgency. A “last remaining” two-bedroom apartment often isn’t. The pressure to act quickly is a sales technique, not a market reality.

Independent legal and financial advice pays for itself every single time, even when friends, colleagues, or developers insist the process is straightforward. Off-the-plan contracts are not straightforward. They are designed to favour the developer, and a specialist adviser is the counterbalance you need.

What we’ve seen work consistently is buyers who spend more time reading than celebrating. They study the developer’s track record, understand every clause in the contract, and enter settlement with a financial buffer already in place. They access our detailed off-plan guide before signing, not after.

The buyers who struggle are those who treated the glossy display suite as sufficient due diligence. Patience, scrutiny, and sound advice are the real competitive advantages in this space.

Take the next step: Access smart property investing tools

Off-the-plan buying, when approached strategically, is a genuinely powerful vehicle for building long-term wealth. The stamp duty savings, depreciation benefits, and capital growth potential are real advantages available to buyers who do their homework. At Elite Wealth Creators, we support buyers and investors with precision sourcing, expert guidance on ownership structures, and tools that keep your cash flow working efficiently throughout the process. Explore our property investing insights to see how we approach portfolio building differently. If you’re considering using your superannuation fund, our guide to SMSF property advantages outlines what’s possible. Book a consultation and let’s build a strategy tailored specifically to your goals.

Frequently asked questions

What does buying off the plan mean in Australia?

Buying off the plan in Australia means purchasing a property before construction is complete, using only the architectural plans, legal contract, and developer specifications as your reference. The title to the property does not yet exist at the time of purchase.

What are the main risks of off-the-plan buying?

The primary risks include construction delays and insolvencies, valuation shortfalls at settlement where the bank values the property below the contract price, and quality variations between what was promised in the plans and what is ultimately delivered.

Can first-home buyers get stamp duty discounts with off-the-plan purchases?

Yes, many Australian states offer stamp duty concessions for off-the-plan buyers, with savings between $20,000 and $40,000 on a $750,000 property being realistic in states such as Victoria, New South Wales, and South Australia.

What protections do buyers have if the developer fails or the build is delayed?

Buyer deposits must be held in statutory trust until settlement, and legal frameworks such as the Queensland Land Sales Act provide mandatory completion timeframes and restrict developers from misusing sunset clauses to exit contracts for their own financial benefit.

Recommended

- How to Buy Off-Plan Property in Australia in 2023 | Elite Wealth Creators

- Step by step property buying guide for Australian first-timers 2026 | Elite Wealth Creators

- Step by step land purchase guide for Australian buyers 2026 | Elite Wealth Creators

- Property buying essentials for first-timers in Australia | Elite Wealth Creators