TL;DR:

- Many trustees mistakenly believe SMSFs can borrow freely for any purpose, but borrowing is heavily restricted and mainly limited to short-term needs or asset acquisition through LRBAs. Understanding these rules and ensuring compliance, especially with related party loans, is essential to avoid severe penalties, disqualification, and loss of tax concessions. Proper planning, expert advice, and adherence to legal framework enable trustees to confidently leverage borrowing opportunities for long-term wealth growth within their SMSFs.

If you believe your self-managed super fund can borrow freely for any investment purpose, you are not alone. Many trustees hold exactly that misconception, and it costs them dearly, whether through missed property opportunities or an unexpected ATO audit. Understanding what is SMSF borrowing rules means looking beyond the surface and grasping a tightly regulated framework that governs every borrowing decision your fund makes. With LRBA assets reaching $75 billion by 2025, the stakes for getting this right have never been higher.

Table of Contents

- Key takeaways

- What is SMSF borrowing rules: the legal framework

- How Limited Recourse Borrowing Arrangements actually work

- Compliance pitfalls and the real cost of getting it wrong

- Related party loans and ATO safe harbour rules

- Putting SMSF borrowing rules into your investment strategy

- My honest take on SMSF borrowing paralysis

- How Elitewealthcreators helps you act with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Borrowing is heavily restricted | SMSFs can only borrow under specific, legislated circumstances, not for general investment needs. |

| LRBAs are the primary vehicle | Limited Recourse Borrowing Arrangements are the only legal pathway for borrowing to acquire investment assets. |

| Related party loans carry serious risk | Loans from related parties must meet strict ATO safe harbour terms or face a 45% penalty tax. |

| Compliance breaches are costly | Penalties include fines up to $19,800 per trustee, disqualification, and fund tax concession loss. |

| Professional advice is non-negotiable | Every borrowing decision should be backed by specialist SMSF advice and documented thoroughly. |

What is SMSF borrowing rules: the legal framework

Most trustees are surprised to discover just how narrow the legal permission to borrow actually is. Australian superannuation law prohibits SMSFs from borrowing money in almost all circumstances. The exceptions are deliberate, limited, and strictly enforced.

Your fund can borrow under three specific conditions, each with tight time and value limits:

- Paying member benefits: Borrowing for up to 90 days to cover a benefit payment to a member when the fund lacks liquidity

- Covering surcharge liabilities: Borrowing for up to 90 days to meet a surcharge liability

- Settling security transactions: Borrowing for up to 7 days when a security trade has already been placed and the fund needs to settle

Critically, each of these short-term borrowings is capped at 10% of total fund assets. If your SMSF holds $600,000 in assets, your maximum short-term borrowing exposure is $60,000 across all permitted purposes combined.

The fourth and most commonly used exception is the Limited Recourse Borrowing Arrangement, which applies specifically to asset acquisition. This is the mechanism most SMSF trustees encounter when exploring property investment. Understanding LRBAs is the cornerstone of any SMSF borrowing strategy.

One more point that catches trustees off guard: borrowed funds cannot be used for operating expenses, management fees, insurance premiums, or member benefits outside the short-term exception. If your fund borrows through an LRBA, every dollar must be directed toward the acquisition of the intended asset. Nothing else.

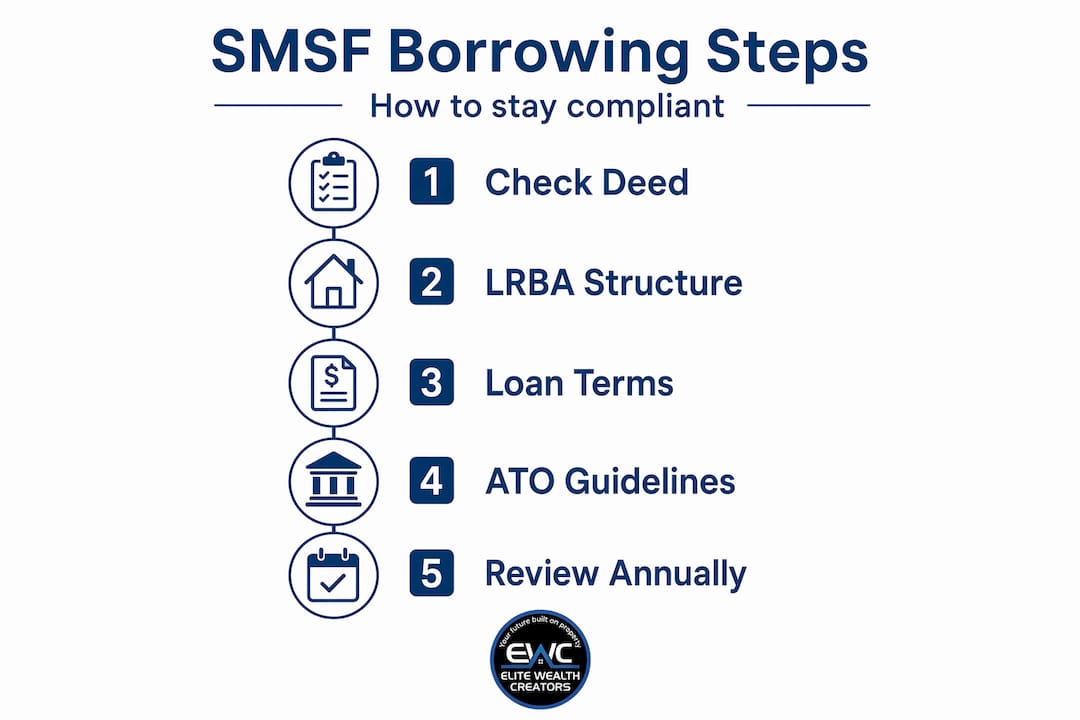

Pro Tip: Review your SMSF trust deed before any borrowing conversation begins. If it does not explicitly permit borrowing under an LRBA, the arrangement is non-compliant from day one regardless of how well-structured the loan itself is.

How Limited Recourse Borrowing Arrangements actually work

An LRBA is the only legal way for your SMSF to borrow money for the purpose of acquiring an asset. The structure protects your fund members by limiting what the lender can claim if the loan defaults. The lender’s recourse is confined strictly to the asset being purchased, meaning your other fund assets remain protected.

Here is how the process works in practice:

- The holding trust is established. A separate bare trust is set up, and the asset is held by a custodian trustee within that trust. Your SMSF does not legally own the asset during the loan period.

- The SMSF makes loan repayments. Your fund services the debt using its own cash flows, typically rental income from the property or contributions from members.

- The asset transfers to the SMSF upon full repayment. Once the loan is fully paid, the legal title moves from the holding trust into your SMSF.

- Lender recourse stays limited. If the fund defaults, the lender can only recover the specific asset held in the bare trust. Your remaining fund assets are untouched.

The asset acquired under an LRBA must be a single acquirable asset or a collection of identical assets. You cannot use one LRBA to purchase two separate residential properties. Each acquisition requires its own separate structure and loan.

There are also strict limits on what you can do with the asset while the loan is outstanding. You can repair and maintain the property, but you cannot improve it in a way that changes its fundamental character. Renovations that upgrade a property beyond its original condition, or development activities, are prohibited during the borrowing period.

SMSF loans do not permit redraw facilities or offset accounts. If you make extra repayments, those funds are locked in. All expenses related to the asset, such as rates, maintenance, and insurance, must also be paid from your SMSF’s own accounts to preserve the required separation of funds.

Pro Tip: When sourcing a lender for an SMSF loan, compare interest rates carefully. Rates for SMSF loans tend to sit higher than standard residential loans, so modelling the cash flow impact on your fund before committing is essential for sound investment planning. You can review SMSF property lending options to understand what lenders currently look for.

Compliance pitfalls and the real cost of getting it wrong

The compliance minefield around SMSF borrowing is real. The ATO does not apply a light touch when it finds breaches, and the consequences can unwind years of carefully built wealth.

The most serious prohibition you need to understand is the absolute ban on lending fund money to members or their relatives. This includes providing any form of financial assistance. Breach this rule and you face penalties of approximately $19,800 per trustee, plus the risk of trustee disqualification. That penalty applies to each individual trustee, so in a fund with four trustees, a single breach could cost nearly $80,000 in fines before any tax consequences are calculated.

Beyond lending prohibitions, the following compliance traps claim the most trustees:

- Non-arm’s length income (NALI): If a related party lends to your SMSF on terms more favourable than a commercial lender would offer, the entire income from that asset can be taxed at a punitive 45% penalty tax rate. This wipes out the tax advantages that made the SMSF structure attractive in the first place.

- Breaching the sole purpose test: Every investment and borrowing arrangement your SMSF enters must exist solely to provide retirement benefits. If a borrowed asset provides a present-day benefit to a member or their associate, such as living in the property or using it for a business, the fund risks disqualification and severe tax penalties.

- Non-compliant loan structures: A non-compliant LRBA can trigger a cascade of consequences including loss of all tax concessions, forced asset forfeiture, trustee disqualification, and an expensive loan unwind process.

“The compliance minefield is real. Don’t navigate it alone.” Understanding each rule before you sign anything is not overcaution. It is the difference between building wealth and destroying it.

Related party loans and ATO safe harbour rules

Borrowing from a related party is legally permitted within an SMSF, but it requires meticulous structuring. A related party includes fund members, their relatives, and entities they control.

The ATO publishes safe harbour guidelines that define the minimum acceptable terms for related party LRBA loans. Meeting these guidelines protects you from the NALI risk described above. Here is how a compliant related party loan compares to a non-compliant one:

| Feature | ATO safe harbour compliant | Non-compliant arrangement |

|---|---|---|

| Interest rate | Matches ATO benchmark rate (published annually) | Below market rate, informal, or nil |

| Loan term | Maximum 15 years (real property), 7 years (other assets) | Open-ended or unspecified |

| Security | Registered mortgage over the asset | No formal security in place |

| Loan agreement | Formal written document executed at establishment | Verbal or email-based agreement |

| Repayments | Regular, documented repayments made on time | Inconsistent or deferred without reason |

Written, formal loan agreements are legally required for any related party LRBA. The ATO has made clear that conduct-based or implied arrangements do not satisfy compliance requirements, even if the economic terms appear reasonable.

One critical requirement that many trustees underestimate: you need genuine evidence of a third-party loan offer to demonstrate that your related party terms are truly arm’s length. Quotes from commercial lenders, even if you choose not to use them, provide the paper trail the ATO expects to see. Informal comparisons or verbal representations will not hold up under scrutiny.

Refinancing an existing LRBA is permitted, but only under strict conditions. The refinance must relate to the same asset, cannot access additional equity, and cannot alter the fundamental loan purpose. You cannot redraw against an LRBA to fund another investment or pay expenses.

Pro Tip: Set calendar reminders to review your related party loan terms against the ATO benchmark rate each financial year. The benchmark rate is updated annually, and missing a rate adjustment can push your arrangement outside safe harbour without you realising it.

Putting SMSF borrowing rules into your investment strategy

Understanding the rules is only half the work. Translating them into a practical investment plan is where trustees either gain ground or lose time.

Before your fund borrows a single dollar, work through the following checklist:

- Review your trust deed. Confirm it explicitly permits borrowing and the type of asset you intend to acquire. An outdated or generic deed will need amending before you proceed.

- Update your investment strategy. Your fund’s documented investment strategy must reflect the borrowing arrangement, the asset class, and how it serves the retirement benefit objective required by the sole purpose test.

- Model your cash flow. Confirm the fund holds enough liquidity to meet loan repayments, ongoing expenses, and member obligations without relying on further borrowing.

- Assess lender options. SMSF loan eligibility requirements vary by lender. Some require minimum fund balances, specific property types, or independent valuations. Checking your SMSF borrowing capacity early saves time and prevents wasted legal costs on a structure that cannot proceed.

- Engage specialist advice. An SMSF auditor, a specialist SMSF solicitor, and a financial adviser experienced in SMSF property investment rules should all review the arrangement before execution.

The most common application of SMSF borrowing in Australia remains direct property investment, particularly residential and commercial real estate purchased for rental income. When structured correctly, the combination of concessional tax rates on rental income inside the fund and potential capital gains tax discounts at retirement makes SMSF property investment one of the more compelling long-term wealth strategies available.

My honest take on SMSF borrowing paralysis

I have worked with dozens of SMSF trustees who understood borrowing was possible, gathered extensive information, and then did nothing. Not because the rules were too complex to follow. Because they were afraid that one wrong move would trigger an ATO audit and unravel everything they had built.

That fear is understandable. The SMSF borrowing guidelines are detailed, the penalties are genuine, and the consequences of a non-compliant loan are severe. But the cost of hesitation is just as real. Every year a trustee delays a compliant property acquisition inside their SMSF is a year of compounding rental income and capital growth that never enters the fund.

What I have seen work consistently is not fearlessness. It is preparation. Trustees who act decisively do so because they have the right structures confirmed, the right advisers aligned, and a documented plan that passes the sole purpose test before a single dollar moves.

The compliance minefield exists. But it is navigable. The mistake is not attempting to borrow. The mistake is attempting it without genuine expert support.

— Nick

How Elitewealthcreators helps you act with confidence

At Elitewealthcreators, we work with SMSF trustees who are ready to stop watching property opportunities pass by and start building real, compounding wealth inside their fund. Our team understands both the SMSF borrowing strategies that deliver results and the compliance requirements that protect your fund’s tax status and your future.

We assess your fund’s borrowing power, align acquisitions to your investment strategy, and connect you with the property sourcing and lending specialists your SMSF needs. Whether you are exploring your first LRBA or refining an existing portfolio, we offer access to expert SMSF property investment guidance that goes well beyond generic advice.

We limit new client onboarding monthly, not for exclusivity, but to protect the quality of every engagement. Spots are almost gone. If you are ready to act with clarity and confidence, start building your SMSF strategy with us today.

FAQ

Can an SMSF borrow money for any purpose?

No. SMSFs can only borrow under very specific short-term conditions or via an LRBA for asset acquisition. Borrowing for operating costs or general investment is prohibited.

What is an LRBA and why does it matter?

An LRBA is the only legal structure that allows an SMSF to borrow money to purchase an investment asset. The lender’s recourse is limited to the specific asset held in a separate bare trust, protecting the rest of your fund.

What happens if my SMSF breaches borrowing rules?

Consequences include loss of tax concessions, trustee disqualification, substantial fines, and a potentially costly loan unwind process. The ATO takes non-compliance seriously and the penalties are applied per trustee.

Can I borrow from a family member through my SMSF?

Yes, but the loan must meet ATO safe harbour guidelines including a formal written agreement, the correct benchmark interest rate, and registered security. Non-compliant related party loans attract a 45% NALI penalty tax on the fund’s income from that asset.

Do SMSF loans allow redraw or offset accounts?

No. SMSF loans under an LRBA do not permit redraw facilities or offset accounts. Extra repayments cannot be reclaimed, and all fund expenses must be paid separately from the SMSF’s own accounts.