TL;DR:

- Australian property cycles involve rising, slowing, correction, and recovery phases influenced by local factors.

- Main cycle drivers include population growth, interest rates, supply constraints, government incentives, and economic resilience.

- Successful investors focus on fundamentals and local data, not fixed cycle predictions like the 18-year myth.

The Australian property market attracts no shortage of bold predictions. Headlines warn of imminent crashes or declare endless booms, yet most of these forecasts are built on shaky foundations. The so-called 18-year property cycle is a prime example — widely cited, rarely scrutinised, and largely dismissed by serious analysts. What actually drives Australian property values is a set of interconnected forces that repeat in broad patterns but never identically. This article breaks down those patterns, exposes the myths that mislead investors, and gives you practical tools to read market conditions with greater clarity and confidence.

Table of Contents

- What is the property cycle?

- Key drivers of the property cycle in Australia

- Common myths and reality checks about property cycles

- How to practically use the property cycle for investing

- A fresh perspective on property cycles: What most guides miss

- Where to get expert help with your property journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Property cycles vary | Each market and property type moves through cycles at different times and speeds. |

| Focus on fundamentals | Population, interest rates, and supply impact property prices more than cycle myths. |

| Debunk cycle myths | No single ‘18-year rule’—successful investors use evidence and local insight. |

| Apply cycle knowledge wisely | Align your property investing with actual indicators rather than chasing media headlines. |

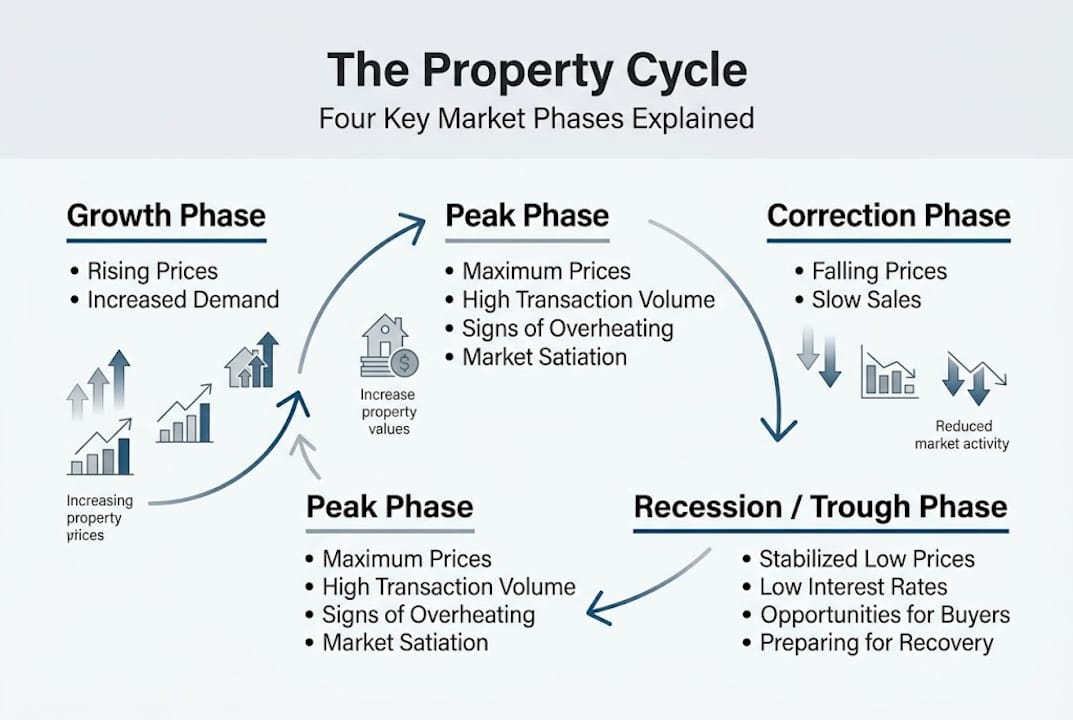

What is the property cycle?

The property cycle is the recurring sequence of market phases that property values tend to move through over time. It is not a rigid calendar or a guaranteed timetable. Think of it as a roadmap that shows the general direction of travel, even when individual roads differ.

According to the Reserve Bank of Australia, property cycles shape market movement through four broad phases: growth, slowdown, correction, and recovery. Each phase has distinct characteristics that affect buyer behaviour, rental demand, and asset values.

The four classic stages:

| Stage | Key characteristics | Typical investor sentiment |

|---|---|---|

| Boom (growth) | Rising prices, high demand, low stock | Optimistic, sometimes over-confident |

| Slowdown | Price growth eases, days on market increase | Cautious, waiting for signals |

| Correction (slump) | Values fall, listings rise, buyers retreat | Fearful, bargain hunters emerge |

| Recovery | Demand returns, prices stabilise and lift | Selective, strategic buying resumes |

One critical point: these stages do not roll out uniformly across the country. A suburb in Brisbane may be in full recovery while inner Melbourne sits in a slowdown. Understanding the cycle at a local level, not just a national headline level, is where real insight begins.

- Booms are fuelled by strong demand meeting limited supply

- Slowdowns often follow interest rate rises or reduced lending appetite

- Corrections present genuine buying opportunities for prepared investors

- Recovery signals are often visible before the broader media reports them

Before you make any asset acquisition decision, build your understanding of property buying essentials relevant to your specific market and budget.

Pro Tip: Do not wait for the media to confirm you are in a recovery phase. By the time the headlines agree, the best entry points are usually gone.

Key drivers of the property cycle in Australia

Knowing the stages is only part of the picture. What actually pushes a market from one stage to the next? In Australia, a specific set of forces consistently drives these transitions, and understanding them gives you a meaningful edge.

The Reserve Bank of Australia identifies population growth, interest rates, and government incentives as the primary forces shaping property demand and investor behaviour across the Australian market.

The five main drivers of the Australian property cycle:

- Population growth. Australia’s consistent net migration and natural population increase create sustained housing demand. More people need more homes, and when supply cannot keep pace, values rise.

- Interest rates and lending conditions. The RBA cash rate directly affects mortgage repayments and borrowing capacity. Rate cuts typically stimulate demand; rate rises cool it. Lending standards set by banks amplify or dampen this effect.

- Supply constraints. Land availability, planning restrictions, and construction timelines limit how quickly new housing can enter the market. This inelastic supply means demand spikes translate quickly into price movement.

- Government incentives. Policies like negative gearing and the capital gains tax discount actively shape investor behaviour. Changes to these settings can shift demand patterns significantly and quickly.

- Economic resilience. Australia has avoided a technical recession for an unusually long period. This resilience supports household incomes, employment, and ultimately, the capacity to service mortgage debt.

How key drivers compare in their market impact:

| Driver | Speed of impact | Duration of effect |

|---|---|---|

| Interest rate changes | Fast (months) | Medium term |

| Population growth | Slow (years) | Long term |

| Government incentives | Medium | Variable |

| Supply pipeline | Slow | Long term |

For a deeper look at why these conditions make Australian property attractive, explore real estate growth benefits and consider how property finance strategies can position you to act when the cycle turns in your favour. If you are assessing your entry timing, reviewing buying property tips for current market conditions is a smart starting point.

Statistic to note: Australia’s population is projected to grow substantially over the next two decades, placing ongoing pressure on housing supply in major cities and regional centres alike.

Common myths and reality checks about property cycles

Few topics in property generate more confusion than the concept of a predictable, repeating crash cycle. The most persistent is the idea that property markets follow an 18-year rhythm, guaranteeing a major correction at a fixed point. This narrative is compelling and memorable, but it does not hold up under scrutiny.

As analysts have pointed out, the 18-year cycle is a myth; Australian property cycles are fragmented and asynchronous across cities and property types. A unit market in Perth and a house market in Sydney are not following the same script.

“The belief that all Australian property moves in lockstep leads investors to make decisions based on national headlines rather than the local fundamentals that actually drive their suburb or asset class.”

What the myths get wrong:

- A single national cycle does not exist. Each city, and often each suburb, operates on its own timeline.

- Crash predictions based on historical cycles ignore structural differences in today’s market, including stronger equity buffers and lower forced-selling conditions.

- Media amplification of cycle narratives can trigger emotional selling at exactly the wrong time.

- Rising interest rates do not automatically cause property crashes, particularly when unemployment remains low and household equity is strong.

What to actually watch instead:

- Mortgage arrears rates. Rising arrears can signal early stress in the market.

- Housing supply pipelines. Fewer approvals today mean tighter supply in 12 to 24 months.

- Equity buffers. High equity across the market reduces forced selling risk.

- Local vacancy rates. Tight rental markets often precede price growth in that area.

Staying across 2026 property trends gives you a clearer view of which indicators are moving right now, and understanding what drives long-term property investment success will help you separate signal from noise.

Pro Tip: When you hear a confident prediction about the next property crash, ask what specific local data supports it. Vague cycle theories without local evidence are rarely actionable.

How to practically use the property cycle for investing

Understanding the cycle is one thing. Using it to make better decisions is another. The goal is not to time the market perfectly; that is almost impossible. The goal is to avoid the costly mistakes that come from emotional buying and selling driven by headlines rather than fundamentals.

A practical step-by-step approach for buyers and investors:

- Identify the local phase. Research your target suburb or city. Is stock rising or falling? Are days on market increasing? Are auction clearance rates moving up or down? These are leading indicators of which stage you are in.

- Assess your financial position. Determine your borrowing capacity, deposit size, and cash flow requirements before the market dictates urgency to you.

- Research supply pipelines. Check approved development applications and new housing starts in your target area. Low supply forecasts support future price growth.

- Review economic fundamentals. Local employment levels, infrastructure investment, and population trends tell you more about sustainable demand than any cycle theory.

- Plan your hold strategy. Property rewards patience. Entering during a slowdown or early recovery and holding through the next boom is a proven approach.

Before committing to a purchase, assess these factors:

- Current rental yield and vacancy rate in the target area

- Comparable sales trends over the past 6 and 12 months

- Planned infrastructure projects that could increase liveability and demand

- Your cash flow resilience if interest rates rise further

- Exit strategy, whether that is sale, subdivision, or long-term hold

For buyers ready to move forward, reviewing the steps to property ownership will ground your approach, and the property buying guide 2026 offers a clear framework for navigating current conditions.

Pro Tip: Conduct your research at the suburb level, not the national level. Markets are local, and so are the best opportunities.

A fresh perspective on property cycles: What most guides miss

Most articles on property cycles present a tidy four-stage model and leave you to figure out the rest. That oversimplification is where many investors go wrong. The honest reality is that cycles do not repeat; they rhyme. The broad patterns are familiar, but the timing, depth, and geographic spread shift with every iteration.

What actually separates successful investors from reactive ones is not better cycle prediction. It is resilience planning. They build portfolios that can withstand a correction without forced selling, hold equity buffers that provide options, and maintain cash flow discipline regardless of which stage the market is in.

As the evidence shows, cycles are not destiny; the investors who succeed focus on fundamentals, adaptability, and local knowledge rather than chasing a predictable national rhythm.

At Elite Wealth Creators, we see this play out regularly. Clients who stay anchored to sound fundamentals, sound cash flow modelling, and local data consistently outperform those chasing the next predicted boom. Tracking investment trends for 2026 is useful context, but it is the decisions you make in your specific market that define your outcome.

Where to get expert help with your property journey

Understanding the property cycle is a significant advantage, but translating that knowledge into well-timed, well-structured decisions requires more than theory. At Elite Wealth Creators, we work with aspiring investors and first-home buyers to cut through the noise and build strategies grounded in real market data and your personal financial position. Whether you need clarity on where the market sits right now or want a tailored blueprint for your next acquisition, our team is ready to guide you. Explore our property investing insights or take the first step toward unlocking financial freedom with expert support behind you.

Frequently asked questions

What are the main stages of the property cycle?

The four main stages are boom, slowdown, correction or slump, and recovery, though these can overlap or vary significantly depending on the location and property type.

Why don’t all Australian cities follow the same property cycle?

Each city’s cycle responds to its own economic conditions, population trends, and supply dynamics, meaning cycles are asynchronous by city and property type rather than moving in national lockstep.

Is it possible to predict the next boom or downturn?

Exact predictions are not reliable, but focusing on fundamentals rather than myth-based cycles gives you a far stronger basis for making informed entry and exit decisions.

What should I watch for to avoid buying at the wrong time?

Monitor interest rates and supply pipelines alongside local vacancy rates and comparable sales data, rather than relying on simplified national cycle predictions.

Recommended

- Why property research is crucial for smarter investing | Elite Wealth Creators

- Why Property Delivers 7-8% Growth as Long-Term Investment | Elite Wealth Creators

- Maximise Equity with Real Estate | Elite Wealth Creators

- Top real estate investing strategies for higher returns | Elite Wealth Creators

- Yigal Realty