What makes one property investor consistently outperform another in the competitive Australian market often comes down to mastering the art of loan structuring. In a landscape where cash flow, borrowing capacity, and risk management directly shape your portfolio’s success, a carefully designed finance strategy is more than a necessity. This guide brings together expert-backed steps for assessing your position, selecting optimal loans, and structuring ownership to help you achieve the highest possible returns from every Australian property investment.

Table of Contents

Quick Summary

| Key Point | Explanation |

| 1. Assess financial position thoroughly | Understand your income, debts, savings, and credit to determine borrowing capacity for property investments. |

| 2. Select the right loan type | Choose a loan that aligns with your financial profile and investment strategy to maximise returns. |

| 3. Establish strong ownership structure | Implement legal frameworks that protect assets, optimise tax efficiency, and mitigate risks. |

| 4. Develop tax-efficient strategies | Plan repayments and ownership structures to minimise tax liabilities and enhance investment performance. |

| 5. Regularly evaluate loan performance | Continuously track loan metrics to identify improvements and optimise financial health of your investment. |

Step 1: Assess existing financial position and goals

Assessing your financial position forms the critical foundation for successful property loan structuring. This process involves taking a comprehensive snapshot of your current financial landscape to determine your investment readiness and potential borrowing capacity.

To systematically evaluate your financial situation, start by thoroughly reviewing your financial profile. This involves gathering and analysing key financial documents and metrics:

-

Income documentation: Collect payslips, tax returns, and bank statements

-

Existing debt obligations: List all current loans, credit card balances, and ongoing financial commitments

-

Savings and liquid assets: Calculate total savings, investment portfolios, and readily accessible funds

-

Credit score: Obtain a recent credit report to understand your borrowing potential

Your financial assessment is not just about numbers, but about understanding your capacity for strategic property investment.

Next, clearly define your investment goals by considering factors like desired annual return percentage, investment timeframe, and risk tolerance. Evaluate potential investment opportunities that align with your financial objectives, ensuring they match your current financial position.

Pro tip: Create a detailed spreadsheet tracking all financial inputs and potential investment scenarios to provide a clear, objective view of your investment landscape.

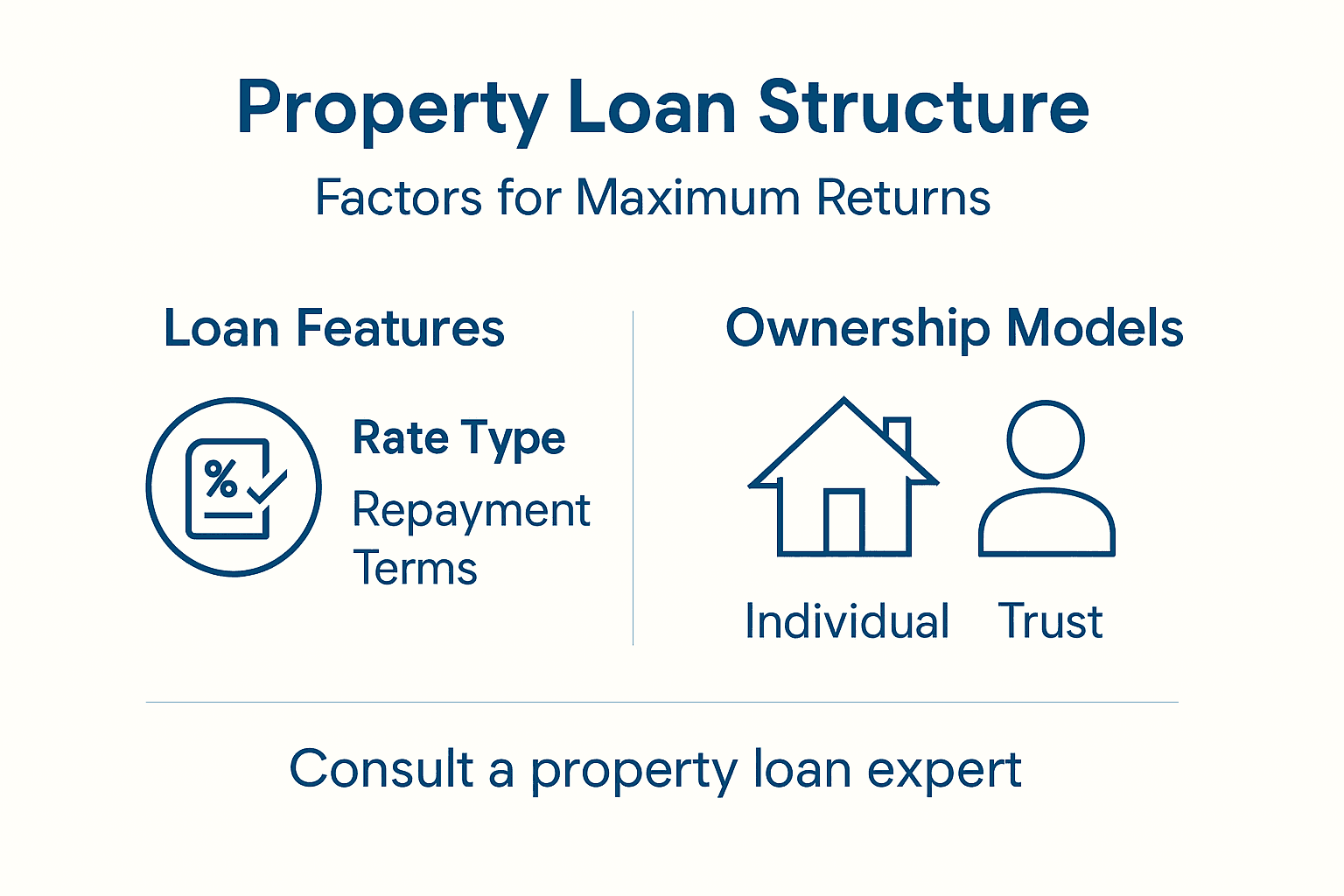

Step 2: Select optimal loan types and features

Selecting the right loan type and features is crucial for maximising your property investment returns. This step involves navigating the complex landscape of financing options to find the most strategic fit for your specific investment goals.

To begin, explore various investment property loan types that align with your investment strategy. Each loan type offers unique advantages depending on your financial profile and property objectives:

-

Conventional mortgages: Ideal for long-term residential investments

-

DSCR loans: Focused on property income rather than personal finances

-

Fix-and-flip loans: Perfect for short-term renovation projects

-

Portfolio loans: Flexible options for multiple property investments

-

Government-backed loans: Potentially lower interest rates and more flexible terms

Your loan selection can make or break your property investment success.

Carefully analyse loan features that impact investment returns by considering critical factors such as interest rates, loan terms, and repayment flexibility. Pay close attention to how each loan structure might affect your cash flow and overall investment strategy.

Pro tip: Compare at least three different loan options from multiple lenders to ensure you’re selecting the most competitive and strategically advantageous financing for your specific investment scenario.

Here is a quick comparison of common investment property loan types and their primary features:

| Loan Type | Typical Use Case | Key Financial Feature |

| Conventional Mortgage | Long-term rental property | Stable rates, full documentation |

| DSCR Loan | Income-focused investment | Based on property income flows |

| Fix-and-Flip Loan | Renovation and resale strategy | Short terms, fast funding |

| Portfolio Loan | Multiple property investments | Flexibility, asset-based lending |

| Government-Backed | First-time or low-deposit buyers | Lower rates, support programs |

Step 3: Structure ownership and security arrangements

Establishing robust ownership and security arrangements is critical for protecting your property investment and minimising financial risks. This step involves creating a strategic framework that safeguards your assets and provides clear legal protection for all parties involved.

Begin by understanding collateral security mechanisms that underpin property investment financing. Key considerations include:

-

First-ranking mortgages: Ensure priority claim on property assets

-

Legal ownership structures: Protect personal and investment assets

-

Security agreements: Clearly define lender and borrower rights

-

Risk mitigation strategies: Limit potential financial exposure

-

Comprehensive documentation: Maintain transparent legal records

Your ownership structure is the foundation of your investment’s legal and financial security.

Analyse security interests and legal frameworks that govern property-backed loans. Consider different ownership models such as individual ownership, trust structures, or corporate entities that provide optimal protection and tax efficiency for your specific investment strategy.

Pro tip: Consult a specialised property law professional to design a bespoke ownership arrangement that balances legal protection, tax effectiveness, and your unique investment objectives.

Below is a summary of ownership structure options and their strategic advantages for property investors:

| Ownership Model | Legal Protection Level | Potential Tax Efficiency |

| Individual Ownership | Limited asset protection | Simple, limited deductions |

| Trust Structure | Strong asset protection | Enhanced tax flexibility |

| Corporate Entity | Excellent liability shield | Company tax rates apply |

Step 4: Implement tax-efficient repayment strategies

Maximising your property investment returns requires strategic tax planning throughout your loan repayment journey. This step focuses on developing a sophisticated approach that minimises tax liabilities while optimising your overall investment performance.

Explore tax-efficient real estate investment strategies that can significantly impact your financial outcomes. Consider implementing key tax management techniques:

-

Depreciation claims: Leverage property depreciation for tax deductions

-

Ownership structure optimisation: Choose tax-efficient entity models

-

Qualified business income deductions: Maximise potential tax benefits

-

Strategic loan repayment planning: Align repayments with tax minimisation

-

Capital gains management: Implement strategies to reduce tax exposure

Tax efficiency isn’t about avoiding taxes, it’s about smart financial planning.

Carefully analyse your loan repayment schedule and investment structure to create a comprehensive tax strategy. This might involve selecting specific loan types, timing property improvements, or structuring your ownership to maximise potential tax advantages and preserve more of your investment returns.

Pro tip: Engage a specialised tax accountant with property investment expertise to develop a bespoke tax strategy that aligns precisely with your unique investment portfolio and financial objectives.

Step 5: Evaluate and refine loan performance regularly

Successful property investment requires continuous monitoring and strategic refinement of your loan performance. This step focuses on developing a proactive approach to tracking and improving your investment’s financial health.

Analyse loan performance metrics systematically to maintain investment effectiveness. Key performance indicators to track include:

-

Delinquency rate: Monitor missed or late payments

-

Default rate: Assess potential loan repayment risks

-

Recovery rate: Evaluate potential loan recovery strategies

-

Prepayment rate: Understand loan repayment patterns

-

Interest coverage ratio: Measure ability to meet loan obligations

Consistent evaluation is the key to transforming good investments into exceptional ones.

Benchmark your loan performance against industry standards to identify potential improvements. This involves comparing your loan metrics with market benchmarks, identifying performance gaps, and implementing targeted strategies to optimise your investment’s financial structure.

Pro tip: Create a quarterly review calendar and set up automated tracking tools to ensure consistent, objective assessment of your loan performance without manual intervention.

Unlock Your Property Investment Potential with Expert Loan Structuring

Struggling to navigate the complexities of property loan structuring for maximum returns is common. From selecting the right loan type to crafting tax-efficient repayment strategies and setting up secure ownership arrangements, each step demands precision and expertise. Key challenges such as understanding loan features, assessing your financial position, and regularly refining loan performance can overwhelm even seasoned investors.

At Elite Wealth Creators, we transform these challenges into clear, actionable strategies. With over 30 years in property and finance, we specialise in personalised solutions that align with your investment goals and financial profile. Our experts guide you through every detail—from structuring your loan to optimising ownership and implementing smart tax strategies for lasting wealth.

Take control of your property investment journey today. Visit Elite Wealth Creators to explore tailored strategies and start maximising your returns with confidence. Don’t wait—your next great investment step begins now.

Frequently Asked Questions

How can I assess my financial position before structuring property loans?

To assess your financial position, gather documents such as payslips, tax returns, and bank statements. Review your income, existing debts, savings, and credit score to understand your borrowing capacity clearly.

What are the different types of property loans I should consider for maximum returns?

Consider various loan types, such as conventional mortgages for long-term investments and DSCR loans that focus on property income. Evaluate the specific advantages of each type based on your financial goals and investment strategy.

How can I ensure my loan features are aligned with my investment objectives?

Carefully analyse loan features like interest rates, terms, and repayment flexibility to select a loan that complements your cash flow needs. Compare at least three options to find the most competitive terms that support your investment objectives.

What ownership structures should I consider when securing property loans?

Consider ownership structures such as individual ownership, trusts, or corporate entities, as each offers different levels of legal protection and tax efficiency. Consult a property law professional to identify the best structure that aligns with your investment strategy.

How can I implement tax-efficient repayment strategies for my property loans?

To implement tax-efficient strategies, explore depreciation claims and assess the most tax-efficient ownership structures for your loans. Work with a tax accountant to develop a repayment plan that aligns with your overall tax management strategy, which can help reduce your tax liabilities.

What key performance metrics should I track for my property loan’s success?

Track metrics like delinquency rates, default rates, and interest coverage ratios to gauge your loan performance. Establish a quarterly review process to identify trends and make necessary adjustments to enhance your investment’s financial health.