You've probably heard the 20% rule so many times it feels fixed. Save 20%, then buy. For a lot of Australians, that figure sits like a wall between them and their first or next property. The truth is more layered than that, and understanding why matters before you decide whether to keep saving or move now.

Where the 20% figure actually comes from

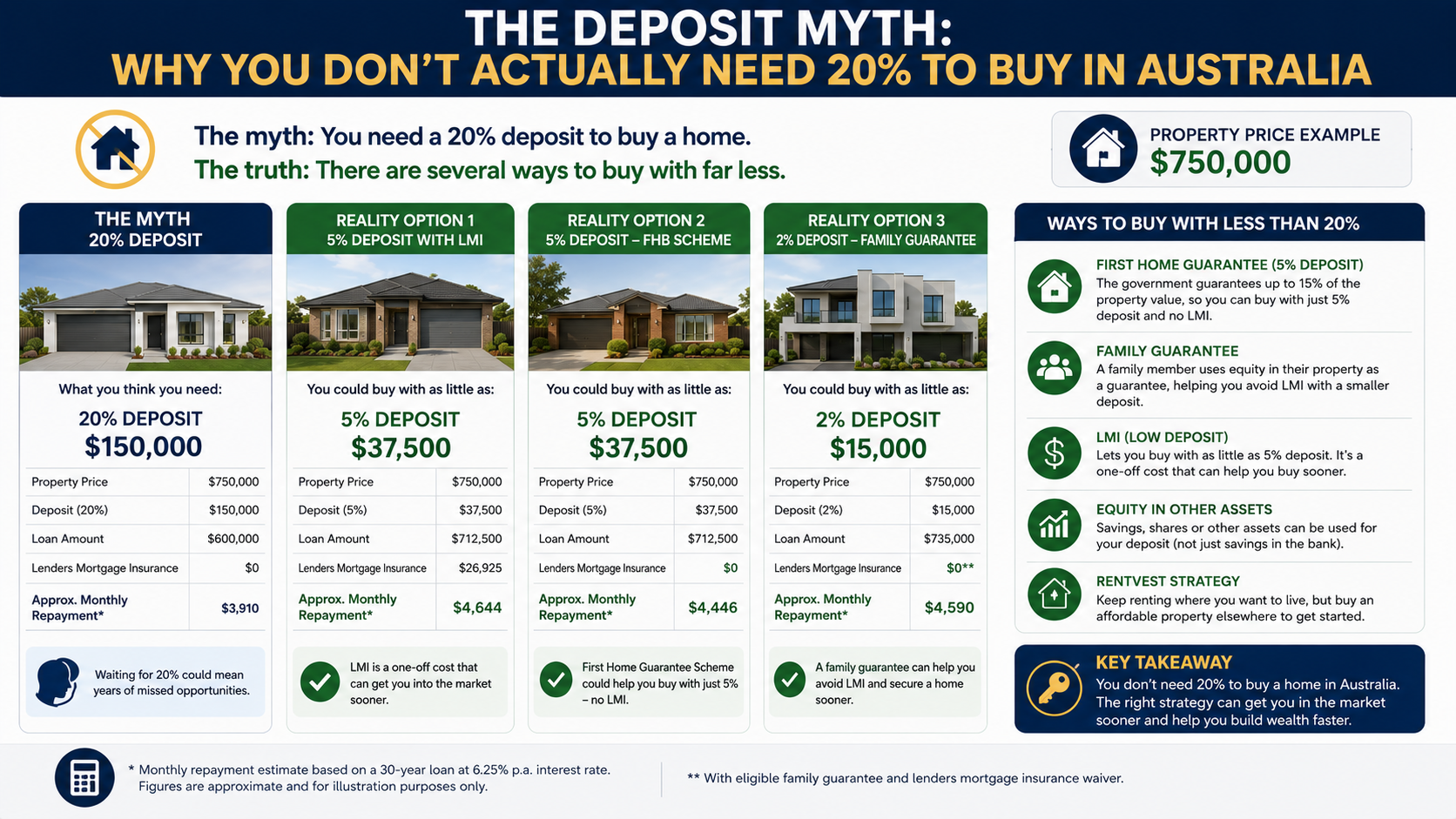

Lenders Mortgage Insurance (LMI) protects a credit provider if borrowers are unable to repay their loan. LMI is usually a one-off cost to a home loan borrower, payable when the amount borrowed exceeds 80% of the value of the property. LMI does not benefit the borrower, it only protects the lender.

So 20% isn't a minimum you must reach to borrow. It's the threshold where lenders stop charging you for their insurance. Despite the fact that LMI covers the lender, the cost is generally passed on to the borrower. LMI premiums can be paid upfront, or added to the loan.

Based on one analysis, LMI can cost around 1-5% of your home loan amount, depending on your LVR. On a $700,000 loan with a 10% deposit, that can translate to a significant upfront sum. The cost is real and worth weighing carefully, but it's a cost with a decision attached, not a hard barrier.

The paths below 20%

There are several legitimate ways to buy without a full 20% deposit. Each has its own trade-offs.

1. Pay LMI and proceed with a smaller deposit

It's still possible to buy an investment property in Australia with as little as a 10% or 5% deposit. However, this depends on the lender and your financial situation. If you go down this path, you'll likely need to pay LMI, but it can make it possible to get into the market sooner, even with a smaller deposit.

If you don't have a 20% deposit yet, some lenders may allow you to borrow more than 80% of the property value if you meet strict criteria, such as clean credit history, strong income, and stable employment. However, you may need to pay LMI if your loan-to-value ratio (LVR) is higher than 80%.

Whether paying LMI makes sense for you depends on how you weigh the upfront cost against the alternative of saving for longer. That's a conversation to have with a licensed broker who can model both scenarios against your actual numbers.

2. Use equity in an existing property

If you already own a property with usable equity, you can use that equity as the deposit on the new investment loan with no cash deposit at all. The usable equity formula is current property value x 80% minus your existing mortgage balance.

This is one of the more common paths for existing homeowners considering their first investment property. The cash deposit requirement disappears, though you are increasing the total debt secured against your assets.

3. Guarantor arrangements

A guarantor is usually a family member who uses the available equity in their home to secure your mortgage. If your deposit is less than 20% of the property, a guarantor could cover the shortfall, so that LMI isn't required. The guarantor takes on real risk here, so this arrangement deserves careful legal and financial consideration by everyone involved.

4. The First Home Guarantee (owner-occupiers only)

For eligible first home buyers, the federal government's First Home Guarantee changes the picture significantly. The First Home Guarantee is a federal government scheme administered by Housing Australia. It allows eligible first home buyers to purchase a home with as little as a 5% deposit, with the government guaranteeing the remaining 15% of the deposit. This means lenders treat the loan as if it has a 20% deposit, which eliminates the need for LMI. Importantly, the government guarantee is not a cash payment, you still borrow 95% of the property value.

From 1 October 2025, the changes to the scheme meant no income caps, no waitlists, and no LMI.

The scheme is for owner-occupiers, you must live in the property as your principal place of residence, move in within 6 months of settlement, and continue living there while the guarantee is active. Price caps apply and vary by state and region. Per Housing Australia, the deposit requirement for the First Home Guarantee is 5% of the property value.

Importantly, this scheme does not apply to investment purchases, it is for owner-occupied properties only.

The trade-offs to think through

Buying with less than 20% is not automatically the right or wrong move. A few things worth thinking through:

- LMI cost versus time: The longer you wait to save a full 20%, the more any property price movement affects your actual purchasing power. Neither outcome is guaranteed, this is a real uncertainty to sit with, not a reason to rush.

- Higher repayments: A larger loan means higher ongoing repayments. Bear in mind that having a higher LVR means you're borrowing more of your home's value, which might leave you vulnerable to rising interest rates.

- LMI on investment loans: LMI, if your deposit is under 20%, is sometimes tax-deductible for investment properties over five years, but confirm this with a tax adviser for your specific situation, as the ATO's treatment of borrowing costs can be nuanced.

- Lender appetite varies: Different lenders have different criteria. Some will stick strictly to a 20% deposit requirement. However, others may offer low-deposit loans to investors with strong finances or previous experience.

A worked example

Consider two buyers both targeting a $750,000 investment property.

Buyer A waits to reach a 20% deposit ($150,000 cash) and borrows $600,000 at an 80% LVR. No LMI applies. Stamp duty, legal fees, and holding costs sit on top of the $150,000.

Buyer B proceeds with a 10% deposit ($75,000 cash) and borrows $675,000 at a 90% LVR. A 10% deposit is achievable at most lenders with LMI applied, typically adding $6,000 to $15,000 in extra cost. Buyer B enters the market earlier, carries a higher loan balance, and pays more interest overall, but has deployed $75,000 less in upfront cash.

Neither path is objectively better. The right answer depends on serviceability, cash reserves, risk tolerance, and what the property is likely to cost by the time Buyer A has finished saving. An independent broker can model these scenarios with your actual income and borrowing capacity figures.

What to do next

If you're weighing up whether to move now or keep saving, three practical steps:

Get a broker assessment of your borrowing capacity. Understanding exactly what you can borrow at different deposit levels, and what LMI would cost in your case, takes the guesswork out of the decision. A licensed mortgage broker can compare lender policies and run the numbers. Book a free call with the EWC team to understand what your options look like with your current position.

Check if the First Home Guarantee applies to you. If this is your first home purchase (or you haven't owned property in the past 10 years) and you plan to live in it, the expanded scheme as of October 2025 may mean 5% is enough, with no LMI. Confirm eligibility with a participating lender via firsthomebuyers.gov.au.

Understand your full cost picture before comparing deposit sizes. Stamp duty, legal fees, inspections, and ongoing holding costs all sit outside the deposit figure. A clear upfront cost schedule, specific to the state and property type you're targeting, prevents surprises at settlement. See our services page for how EWC coordinates the property and finance side of a purchase, or visit /insights for more on structuring your first investment.

General information only, not personal financial advice. Speak with a licensed adviser before acting.