The problem most investors underestimate

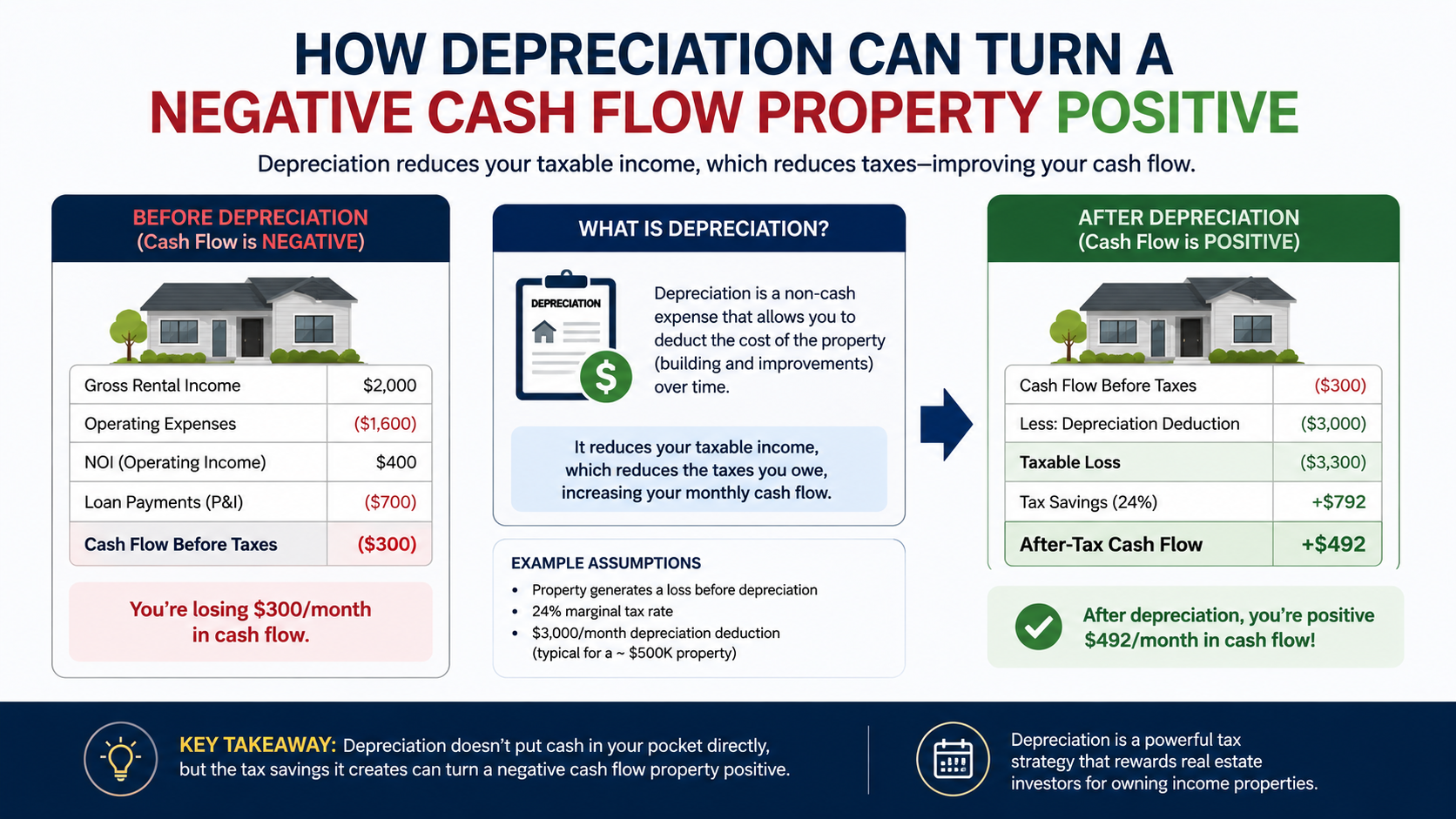

You run the numbers on an investment property. Rent comes in, but mortgage repayments, rates, insurance, and property management fees go out. The property is cash-flow negative by, say, $400 a month. That gap has to come from somewhere, and for a lot of buyers it is the reason they walk away.

What those numbers often leave out is depreciation: a deduction you claim at tax time without spending an extra dollar. When depreciation is added to the picture, the after-tax weekly cost of holding a property can shift substantially, sometimes enough to tip a negative position into a positive one.

How depreciation works under Australian tax law

The ATO allows investment property owners to claim the decline in value of a property as a tax deduction. It lets you claim the decline in value of the building structure and its fixtures and fittings as a tax deduction, even though you have not spent any money in that financial year.

There are two separate systems, each governed by the Income Tax Assessment Act 1997 (ato.gov.au):

Division 43 (capital works): This covers the building structure itself, including brickwork, concrete, roofing, windows, walls, and fixed built-in items, and is claimed at a flat rate of 2.5% per year over 40 years for buildings constructed after 15 September 1987.

Division 40 (plant and equipment): This covers removable or mechanical assets within the property, including air conditioning units, hot water systems, carpets, blinds, ovens, and dishwashers, which depreciate at individual asset rates set by the ATO based on each item's effective life. Effective lives are published in ATO Tax Ruling TR 2024/3.

There is an important rule affecting established properties. From 1 July 2017, the government restricted Division 40 deductions for second-hand plant and equipment items in residential properties. If you purchase a residential property with existing fixtures and fittings, you cannot claim Division 40 deductions for those items; you can only claim Division 40 for new items you purchase and install yourself. Division 43 building allowance deductions are not affected by this change. For new properties, both Division 40 and Division 43 are available in full.

A note on quantity surveyors: For investment property claims, the ATO requires a depreciation schedule prepared by a qualified quantity surveyor for capital works (Division 43) claims. The cost of the report is tax-deductible.

The trade-offs to weigh

Depreciation is genuinely useful, but it is not a free lunch. A few things to understand before relying on it:

Depreciation reduces your CGT cost base. Every dollar of Division 43 you claim reduces your CGT cost base, which increases your capital gain when you eventually sell. The same applies to Division 40 claims. Speak with a registered tax agent about how this affects your long-term position.

New versus established properties. New properties generally contain higher depreciation deductions than established ones. This is because new properties are not affected by the 2017 legislation changes and their owners are eligible to claim plant and equipment assets. Construction costs generally increase over time, making capital works deductions on new buildings higher.

Older properties are not automatically excluded. Even if your property is older, you can still claim capital works deductions if it was built after 16 September 1987. Never assume your property is too old to qualify.

Tax benefit depends on your marginal rate. For the 2025-26 financial year, resident income tax rates progress from 0% for income up to $18,200, then 16%, 30%, 37%, and a top rate of 45% for income over $190,001 (per the ATO, ato.gov.au), plus the standard 2% Medicare levy. The higher your marginal rate, the more each dollar of depreciation saves you in tax.

The tax benefit comes at year-end, unless you vary. PAYG employees can apply to the ATO for a withholding variation. This allows property investors to adjust the amount of tax withheld from their salary by their employer, taking into account the expected tax deductions from their investment property. Instead of receiving a lump sum tax refund at year-end, investors can access the benefits of their deductions throughout the year via increased take-home pay. Discuss this with a registered tax agent, as accuracy is important.

A worked example

The numbers below are illustrative only. They are not a projection or a guarantee of any outcome. All figures are in today's dollars.

Assume a brand-new apartment purchased for $650,000, with a land-to-building split where the building component is $420,000. The investor earns a salary that puts them on a 37% marginal tax rate (plus 2% Medicare levy, so 39% combined).

Annual cashflow before tax:

- Rental income: $28,600

- Mortgage interest, rates, insurance, management: -$36,400

- Pre-tax shortfall: -$7,800

Depreciation deductions (Year 1, illustrative):

- Division 43: $420,000 x 2.5% = $10,500

- Division 40 (sample items, diminishing value): $4,200

- Total depreciation: $14,700

Combined property loss for tax purposes:

- Cash expenses exceed income by $7,800, plus $14,700 depreciation = $22,500 total loss

Tax saving (at 39% combined rate): $22,500 x 39% = $8,775

After-tax position:

- Cash shortfall: -$7,800

- Tax saving: +$8,775

- After-tax surplus: approximately +$975 per year

The property moves from cash-flow negative to marginally positive on an after-tax basis, in Year 1 alone. Depreciation is a non-cash deduction, meaning you do not spend anything in the year you claim it, but it reduces your taxable income all the same. For a typical new apartment, depreciation can add $8,000 to $15,000 in deductions per year on top of cash expenses.

These figures are examples to illustrate the mechanics. Actual outcomes depend on the specific property, your rental income, your interest rate, your marginal tax rate, and the ATO-compliant depreciation schedule prepared by a qualified quantity surveyor. Run your own numbers with a tax agent and a quantity surveyor before drawing any conclusions.

What to do next

If you are weighing up an investment property purchase and want to understand how depreciation affects the real cost of holding it, three concrete steps apply:

Get a quantity surveyor estimate before you commit. Many quantity surveyors will provide a depreciation estimate for free or low cost before you finalise a purchase. The fee for a quantity surveyor report typically runs $500 to $800 for a standard residential property, and the fee itself is tax-deductible in the year you pay it. Factor this into your due diligence.

Discuss a PAYG withholding variation with a registered tax agent. If you are a PAYG employee, the ATO allows you to apply for a PAYG withholding variation (form NAT 2036) if you expect your allowable deductions to significantly reduce your taxable income. Once approved, your employer withholds less tax each fortnight, effectively giving you the benefit of your deductions throughout the year rather than waiting for a lump sum refund.

Talk to us about the property itself. The depreciation benefit is only part of the picture. Rental income, vacancy risk, property quality, and independent rental appraisals all matter too. Book a call with the Elite Wealth Creators team to understand what is available in the market and how the full cashflow picture stacks up, or explore our services.

General information only, not personal financial advice. Speak with a licensed adviser before acting.